Zaggle Prepaid Ocean Services: PAT up 62% & Revenue up 37% in 9M-24 at a PE of 129

Conservative guidance of 40-50% revenue growth with adjusted EBITDA margin of 11-13% in FY24 & FY25. PAT growth for ZAGGLE to be higher than revenue growth on account of falling ESOP & interest cost

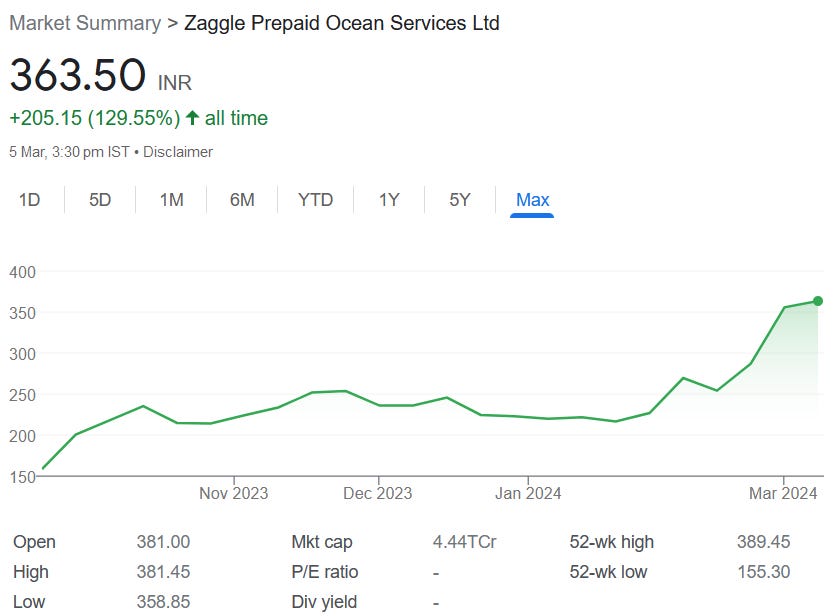

1. # 1 Issuer of Prepaid cards in India

zaggle.in | NSE: ZAGGLE

diversified offering of fintech products and services, having one of the largest number of issued prepaid cards in India in partnership with certain of our banking partners (which constituted approximately 16.0% of India’s total prepaid transaction volume, as of March 31, 2023), a diversified portfolio of SaaS, including tax and payroll software, and a wide touchpoint reach (Source: Frost & Sullivan Report). We are a leading player in spend management, with more than 50 million prepaid cards issued in partnership with banking partners and more than 2.27 million users served, as of March 31, 2023.

2. FY20-23: PAT CAGR of 9%, Cash PAT CAGR of 43% & Revenue CAGR of 52%

Weak FY23: PAT down 45%,Cash PAT down 1% & Revenue up 49%

Gross margin contraction from 81% in FY21 to 42% in FY23

ESOP cost impact on PAT margin in FY23

3. H1-24: PAT down 31%, Cash PAT up 69% & Revenue up 38%

4. Strong Q3-24: PAT up 920% & Revenue up 35% YoY

PAT up 101% & Revenue up 8% QoQ

5. Strong 9M-24: PAT up 62% & Revenue up 37% YoY

Strong margin improvement

6. Strong outlook: Revenue growth of 40-50%

i. FY24 & FY25: Revenue growth of 40-50%

So guidance wise yes on the growth we are in the range of 40% to 50%

ii. FY24 & FY25: Improvement in margins

Adjusted EBITDA margin in 11-13% range compared to 11.3% in FY23

In terms of adjusted EBITDA our guidance is 11% to 13% and we will fall in that region.

7. PAT growth of 62% & Revenue growth of 37% in 9M-24 at a PE of 129

8. So Wait and Watch

If I hold the stock then one may continue holding on to ZAGGLE

Based on 9M-24 performance, ZAGGLE looks on track to deliver the strongest PAT in FY24, touching peak PAT delivered in FY22

For FY24, ZAGGLE is on track to deliver as per the guidance of 40-50% revenue growth and 11-13% adjusted EBITDA margin.

Reduced interest costs to drive PAT growth in FY25

Following the recent IPO, the company has successfully repaid INR470 million in borrowings, which is expected to result in reduced finance costs starting from H2. In the future, we will realize significant interest cost savings, resulting in a meaningful shift towards the profitability.

ESOP costs have been a drag on the bottom-line and are expected to reduce going forward which will drive PAT growth in FY25 and FY26

FY '24, it is going to be roughly about INR19 crores and the going forward, which is '25 and '26, it will be minuscule about INR4 crores or so is, what is our guidance

Have headroom for growth for next 3-4 years without needing money.

So, sir, we have raised about INR490 crores from the IPO and it is sufficient for our next three years to four years of growth. It would -- if unless and until we go ahead and do an inorganic acquisition, where we might require some external funding. We do not see any signs of needing money in the next two to three to maybe let's say three to four years.

Q4-24 is expected to be strong

ZAGGLE management is confident of growth

I think we do not see any specific head winds for our business. We see more and more confidence growing with corporate customers and banks to work with us as a profitable listed entity.

9. Join the ride

If I am looking to enter ZAGGLE then

ZAGGLE has delivered PAT growth of 62% and revenue growth of 37% in 9M-24 at a PE of 129 which makes the valuations quite rich over the short term.

With an outlook for 40-50% top-line growth top-line growth and higher bottom-line growth on account of falling ESOP costs & interest costs a PE of 129 can be sustained over the longer term given that ZAGGLE management claims that the growth estimates are conservative

At a 100+ PE, the margin of safety is quite low to sustain even a single weak quarter.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer