Yes Bank Q4 FY26 Results: Valuation Analysis Re-Rating?

Yes Bank delivers record FY26 profit, 1% ROA milestone, and strong asset quality. But does it justify a P/B re-rating? Full valuation analysis with scenarios.

yes.bank.in | NSE: YESBANK

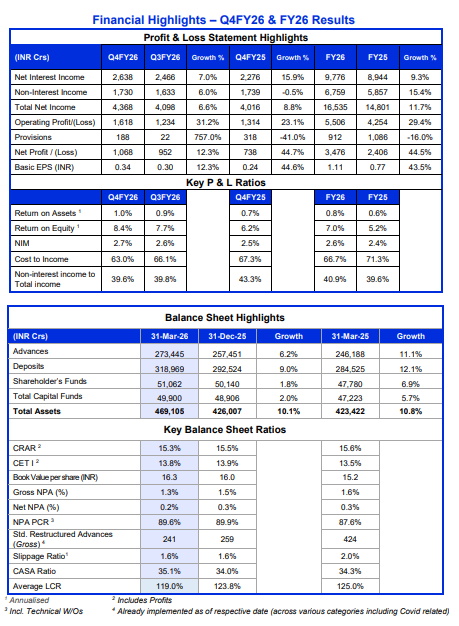

1. FY26 Performance Snapshot (What Changed)

The latest Q4 and FY26 results confirm what the market was waiting for:

The balance sheet is repaired

Asset quality is no longer a risk

Profitability is improving

But the real question for investors is not about the past.

Does Yes Bank now deserve a higher valuation multiple?

2. Current Valuation (Where the Market Stands)

P/B =1.25x

Market Cap =₹63,377.2 Cr | Current market price = ₹20.41

Book Value=₹16.3

P/E= 18.2x

For banks, P/B matters more than P/E. Banks are valued on how efficiently they use capital (RoE), not just earnings.

3. The Valuation Thesis

Management execution → RoA → RoE → P/B → Stock Price

Where Yes Bank Stands Today

Current RoA~0.8%

RoE~7%

P/B~1.24x

What Market Needs to See

RoA≥ 1% sustained

RoE≥ 12–15%

Result ==> P/B rerating

4. Management Guidance → Valuation Impact

Growth Strategy

Loan growth: 13–15%

Supports earnings growth

Retail + SME focus

Improves margins

Controlled corporate exposure

Reduces risk

CASA & Liability Strategy

CASA~30% ==> Improve to 35–40%

CASA ↑ → Cost ↓ → NIM ↑ → RoA ↑ → P/B ↑

NIM Expansion Strategy

RIDF/PSL reduction ==> Improves yield

Priority Sector Lending (PSL) means banks are required to lend a fixed portion of their loans to specific sectors that are important for economic development.

If a bank fails to meet PSL targets, it must deposit money into RIDF (Rural Infrastructure Development Fund).

RIDF/PSL are low-yield regulatory investments that drag returns. Reducing them directly improves profitability.

Deposit mix improvement ==> Expands margins

Target NIM3.25–3.50%

Asset Quality & Credit Cost

GNPA: Stable at low levels

Credit cost: Controlled

Legacy stress: Largely behind

This ensures RoA improvement is sustainable

5. Valuation Scenarios

Scenario Analysis

Bear

RoA <0.8%

RoE<10%

P/B 1.0–1.2x

Base

RoA =0.8–1.0%

RoE = 10–12%

P/B = 1.3–1.6x

Bull

RoA = 1.1–1.3%

RoE = 13–15%

P/B 1.8–2.2x

Stock is fairly valued today

Upside depends entirely on RoA expansion

6. Why the Market Is Still Not Fully Convinced

Despite strong results, valuation remains moderate.

Key Concerns

CASA still below top-tier banks

NIM expansion is guided, not proven

ROE still sub-10% (FY26 average)

Market view → “Turnaround is real, but premium profitability is not yet proven.”

7. The 3 Triggers for Re-Rating

Sustained RoA Above 1%

Not just one quarter — consistency matters

NIM Expansion Toward 3.5%

Driven by better liability mix

CASA Improvement

Structural cost advantage

If these happen → valuation rerates

8. Final Verdict: Is Yes Bank Ready for Re-Rating?

Short Answer

Yes—but only if the bank sustains RoA above 1% and improves ROE into double digits.

Investment View

Not a deep value play

Not yet a premium bank

A transition story with rerating potential

Bottom Line

Yes Bank is no longer broken. But it is not yet proven.

If RoA sustains above 1% → stock rerates

If RoA falls back → valuation stays capped

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer