WPIL Ltd: Order book 2.6X FY23 revenues, to be executed in 3 years

Good revenue visibility, strong YoY performance, solid cash generation, available at attractive valuations

Company Overview

WPIL Limited is a multinational pumps and systems company, with diversified operations covering the entire gamut of the pumping industry.

The Project division provides end to end solution from Survey, Hydraulic studies, System design, Intake structures, Treatment plants, Storage reservoirs, Pumping stations, Pipelines and House connections.

WPIL expanded operations globally through various inorganic acquisitions in Italy, France, Switzerland, South Africa, Australia and Thailand. WPIL has 12 global manufacturing locations covering the entire process of pump manufacture from casting, fabrication, machining, assembly and testing

Share Details

BOM: 505872 (wpil.co.in)

Quality: Returns on capital employed in cash

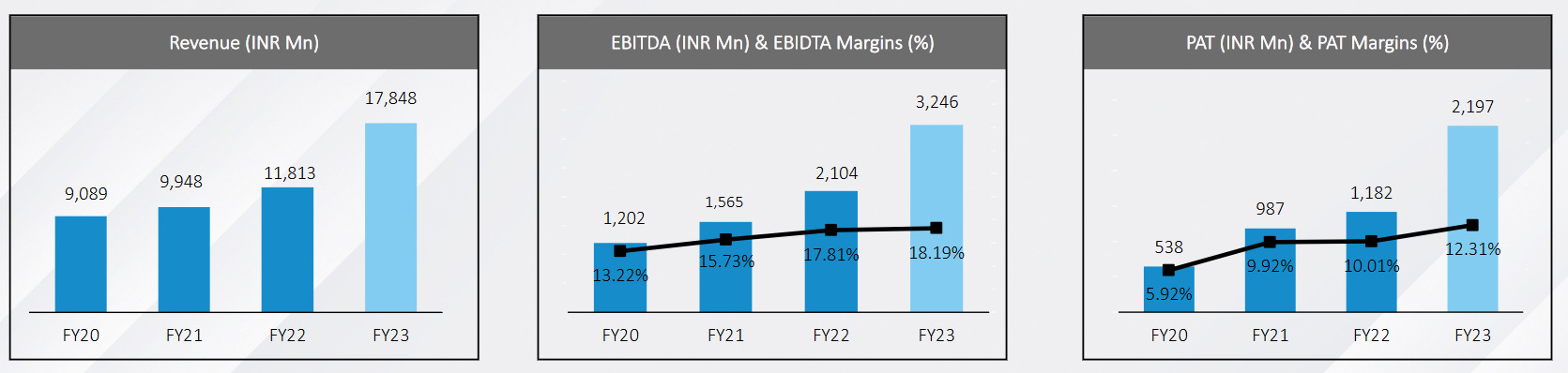

The return ratios are not as good as FY19 but still they are improving sequentially since FY20. Cash conversion has always been solid and is a strength of WPIL.

Growth

The growth performance of WPIL since FY19 is quite poor. The interest in WPIL is on account of the turnaround between FY20 and FY23. While growth performance has been poor, WPIL stands out in its ability to generate free cash flow.

Growth Momentum

The top-line growth momentum is extremely strong and this momentum continues into Q1-24. While YoY growth for Q1-24 PAT is good one needs to keep a watch on the bottom-line growth in FY24.

Outlook

Strong revenue visibility

Consolidated order book Rs 4,616 cr.

Order book size, 2.6X times of FY23 revenue

To be executed within three years.

India order book of Rs 3,955 cr, the remaining Rs 661 cr is for the international business

International order book at 0.8X of FY23 international revenue.

India business: It has got INR 3,600 of projects (there is a INR 600 crore O&M in that) and about INR 350 crores of product.

No revenue guidance

We are very strong. We are very confident of good opportunities for growth going forward, but no guidance, we don't want to make forward looking statements.

EBITDA outlook for a 15-20% range

We want to focus on EBITDA margins between 15% and 20%. So when we get to 15%, we start focusing on the margins. But when we get to 20%, we are looking at revenue growth.

Inorganic growth opportunities to utilize cash

We are exploring opportunities.

So What????

If I currently hold the stock, I may continue holding it based on my past returns, expectations for future returns, and the availability of alternative stock ideas. WPIL has a strong order book in place and keep watching the efficient execution of the order book.

If I don't currently own the stock, I may want to enter it at the current level.

Order book 2.6X of FY23 revenues

Tailwinds in India because of governmental spending

The order book is completely divided between Jal Jeevan, AMRUT and irrigation. So I think Jal Jeevan would be more than 50% presently because it is the major initiative in the water section by the government. Second, in the execution of INR 800 crores last year, again Jal Jeevan would be close to 50%-55%.

Outlook for the future is very strong and management is quite confident sustaining top-line and margin growth on the back of good revenue visibility

WPIL is trading at PE of 17. The valuations are attractive given the outlook for WPIL.

WPIL generated Rs 148 cr of free cash flow on a market cap of about Rs 3,250 cr. This implies that WPIL is trading at a free cash flow yield of 4.6% which also make its valuations quite attractive.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades