Vishnu Chemicals: 2X+ top-line in last 2 yrs, similar pace expected for FY24

Capacity expansion to drive growth supported by improving EBITDA and higher free cash flow generation, all available at reasonable valuations

1. Largest manufacturer of Chromium & Barium compounds in India

Vishnu Chemicals Limited (vishnuchemicals.com) is in the business of manufacturing, marketing and export of chromium chemicals, Barium compounds and other specialty chemicals worldwide. The barium compounds are produced under its subsidiary Vishnu Barium Private Limited.

Vishnu Chemicals Limited caters to various export markets in Europe, Asia, Africa, North America, South America etc. Consolidated, domestic and export business are roughly 50:50

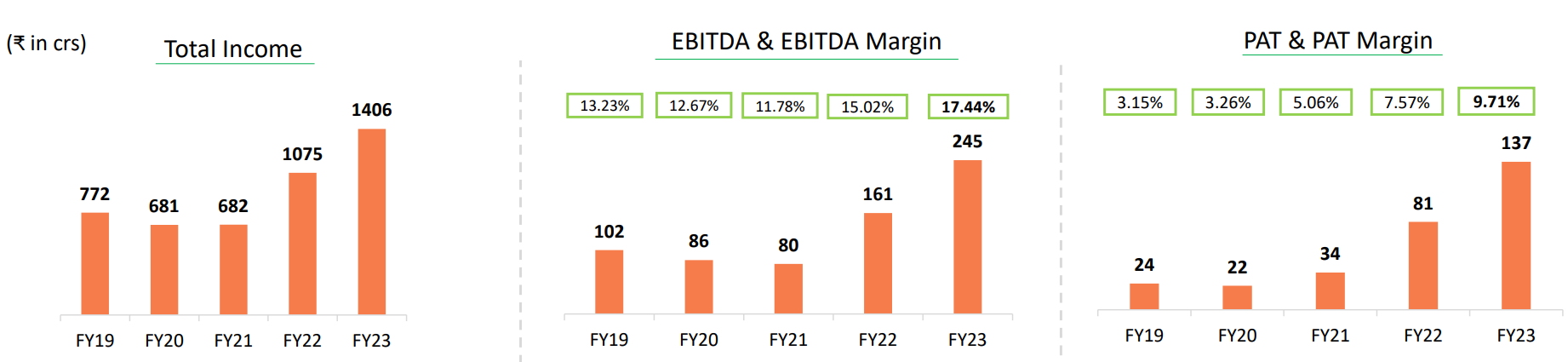

2. Vishnu has delivered growth since FY21

CAGR between FY21 to FY23

Revenue: 44%

EBITDA: 75%

PAT: 101%

3. Growth with disciplined capital utilization

Solid return ratios from FY21

4. Growth getting converted to EPS

EPS delivering CAGR of 54% between FY19 to FY23

5. Growth to continue in FY24

i. Capacity addition: Creating head room for growth

Chromium: -Average operating levels ~80% between FY19FY23.. In FY23, a debottlenecking exercise resulted in capacity expansion by 10,000 TPA. The full benefits of the expanded capacity are expected in FY24.

Barium: Average capacity utilisation since FY20 is ~75%. Brownfield expansion to introduce a new speciality chemical to aid Barium portfolio diversification. To be commissioned by H1FY24.

ii. Volume growth to be driven by barium

Mostly the volume growth will be coming through barium chemistry, that is how we are seeing that

iii. Growth “at similar levels“, last 2 years top-line grew 44%

We would not be able to give a guidance at this juncture, but our endeavor will be to a grow at a similar levels of what we have seen over the last two years and now that this new product addition in barium is happening so we are very confident that the growth trajectory will continue.

iv. 18% EBITDA target for FY24 vs 17.4% in FY23

Yes, we are expecting a margin improvement in chrome as well as barium. Barium in lieu of a backward integration what we have done. Our raw material cost will further improve that can be a leverage for us to gain more market share globally as well as achieve desired EBITDA margin.

I think our objective is to target at 18% EBITDA

6. Free cash generation from FY24

Capex cycle is getting over as capacities come online H1-24

Nearly about 10 Crores is pending as a capex which has to be spent during this financial year.

Free cash flow = Cash Flow from Operations + Capex

FY23 Capex = 137-20 =117

Rs 117 cr of capex reducing to Rs 10 cr has the potential to generate about Rs 100 cr of additional free cash

7. EPS CAGR of 54% for FY19-23 at a PE of 15

Valuations at a 15 PE attractive considering past EPS CAGR of 54% and the intent to “grow at a similar levels of what we have seen over the last two years“

7. So Wait and Watch

If I hold the stock then one must

Wait and watch for quarterly results to see if the management is delivering on its intent to “grow at a similar levels of what we have seen over the last two years“

Watch out for management commentary on pricing in Q1-24 as it can impact the growth story

In barium, yes, China is an important player. I mean we are not witnessing a lot of price pressure at the moment and also, we are not seeing any volume decrease

In the standalone business the chromium chemicals China is not a competitor for us or not an immediate player because whatever chemical is produced in China are sold in China, so we are competing with US, Turkey, and South Africa who are our main players.

Management commentary as of May-23

8. Or join the ride

If I am looking to enter the stock then

Valuations are reasonable. PE of 15 for growth cycle running since FY21

Management intent to deliver on the bottom-line with 18% EBITDA target

Potential of incremental free cash flow of Rs 100 cr on a market cap of about Rs 2,720 cr implies a potential of incremental free cash flow yield of 4.4% (100/2720) which will the valuations cheaper than the 15 PE today

Pricing in the overall chemicals industry is under pressure. Management in May-23 was confident on pricing for both chromium and barium. If I want to be doubly sure, I may wait for the Q1-24 results before making an entry.

Don’t like what you get every morning?

Let us know at hi@moneymuscle.in

Will send you better stuff.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades