Vilas Transcore H1 FY26 Results: PAT Up 74%, On-track FY27 Guidance

Guides 66%+ revenue CAGR by FY27, led by capacity growth and widening product mix. Trading at attractive valuations with opportunity of re-rating of multiples.

1. Transformer Lamination, Toroidal Cores, and CRGO Slitted Coils.

vilastranscore.com | NSE - SME: VILAS

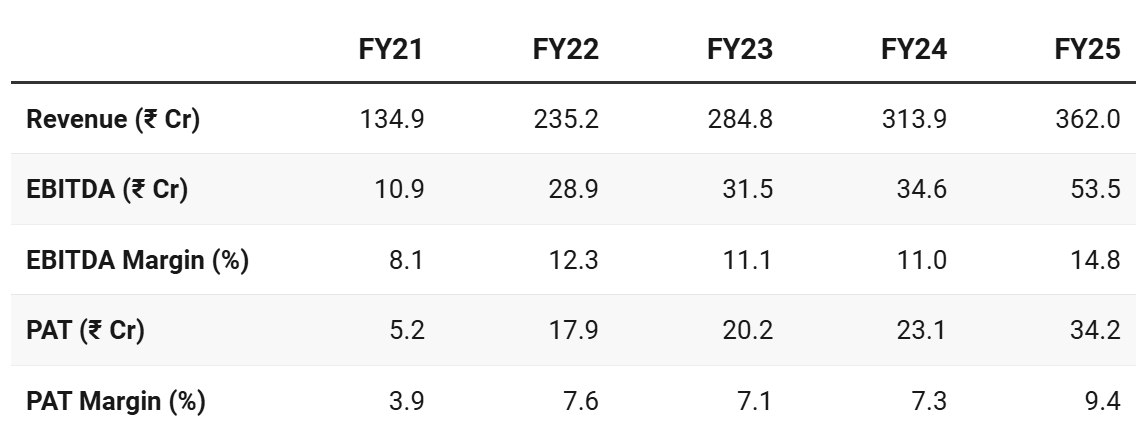

2. FY21-25: PAT CAGR 60% & Revenue CAGR 28%

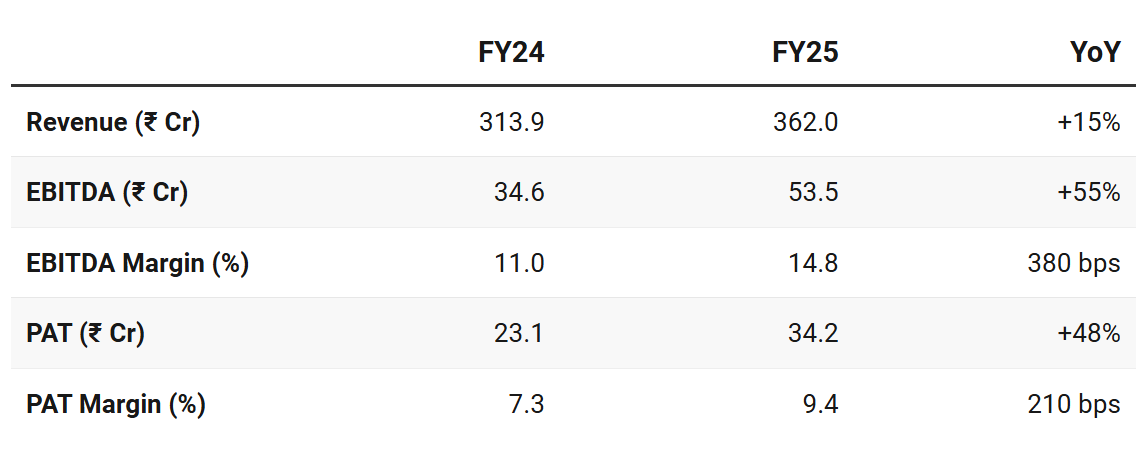

3. FY-25: PAT up 48% & Revenue up 15%

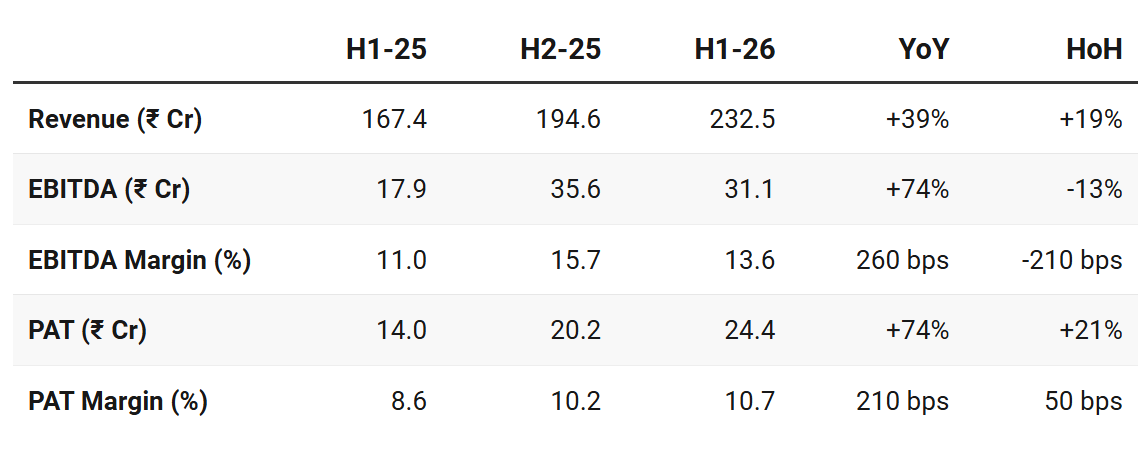

4. H1-26: PAT up 74% & Revenue up 39% YoY

PAT up 21% & Revenue up 19% sequentially

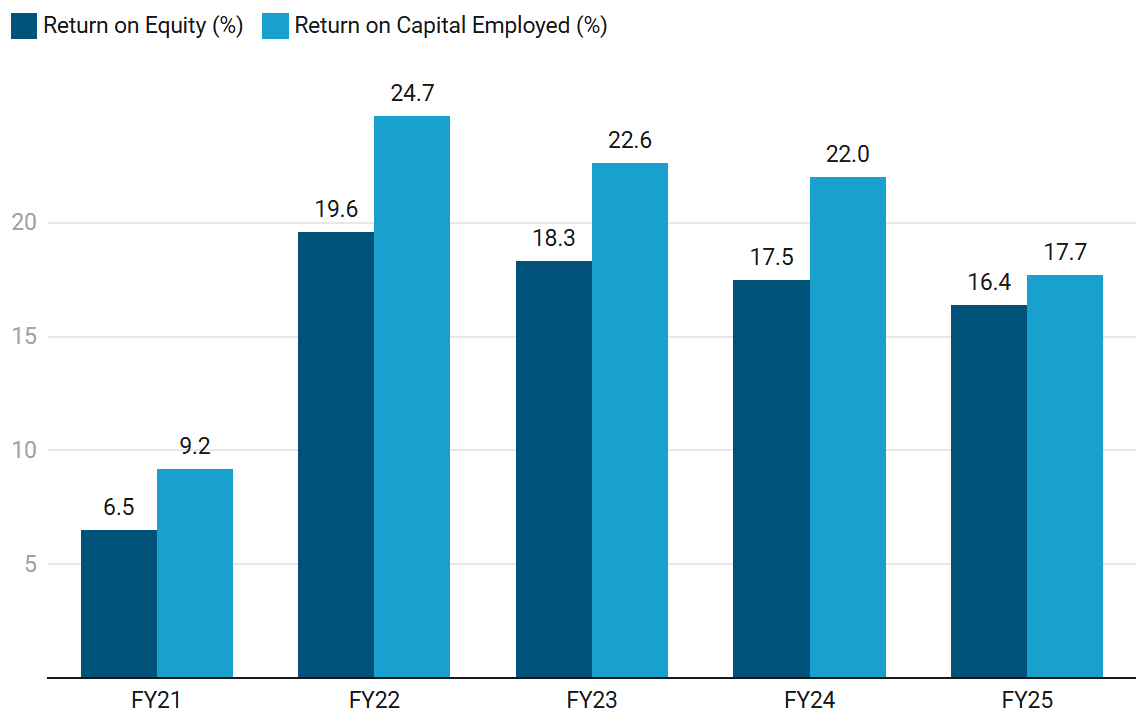

5. Business Metrics: Strengthening Return Profile

Margin expansion & capital efficiency amid capacity constraints

Outlook: ROCE is expected to rebound once the new 36,000 MTPA capacity is fully utilized by FY27, with incremental contribution from high-margin products like nanocrystalline cores and radiators.

6. Outlook: 35-40% Growth in FY26

Driven by new capacity, product ramp-up, and demand tailwinds

6.1 Management Guidance

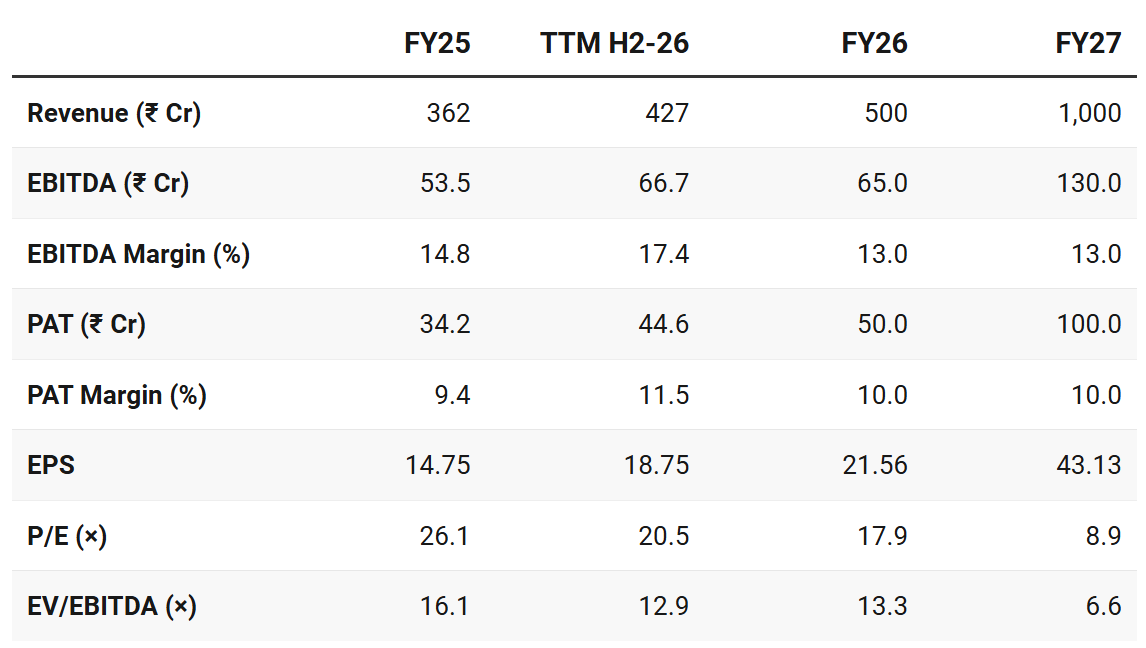

Vilas Transcore is guiding for a revenue CAGR of 66% for FY25-27 and as revenue scales from ₹362 Cr in FY25 to ₹1,000 Cr in FY27

The company is targeting volume growth of 45-50% in FY26E, though revenue growth will lag at 35-40% due to a 20-30% decline in CRGO prices. The company has set an ambitious revenue target of INR 10bn in FY27E, anticipating that a recovery in CRGO prices will provide a significant tailwind.

Demand from transformer manufacturers remains strong, supported by the continued expansion of power transmission and distribution networks across the country.

Government's focus on renewable energy integration, grid modernization, and the replacement of aging transformer plates is further driving production growth.

Sector is also benefiting from the steady rollout of large solar and wind projects

This growth is translating into consistent order inflows from utilities and EPC players, who are ramping up procurement for upcoming transmission and corridors, green energy projects, and substation upgrades.

With rising industrial power consumption, ongoing rural electrification, and strong investment from both public and private sectors, CRGO demand is expected to remain firm over the medium to long term.

7. Valuation Analysis — Vilas Transcore Ltd

7.1 Valuation Snapshot

Current Market Price: ₹385.05; Market Cap: ₹942.60 Cr

At single digit multiple for P/E and EV/EBITDA for FY27 — the forward valuations are quite attractive

Provide opportunities for re-rating of multiples from a FY27 perspective.

7.2 Opportunity at Current Valuation

FY27 valuations are not demanding

Provide strong opportunity for re-rating based on FY27 expectations

At single digit multiples for FY27 there is a strong margin of safety embedded in the valuations — useful in the current environment of weakness

Strong Demand Visibility (Industry Tailwind)

Transformer industry demand remains structurally strong driven by:

Grid expansion, renewable energy (solar + wind)

Replacement of aging infrastructure

India demand strong; global demand even tighter (multi-year order books)

Management clearly highlighted:

No slowdown in transformer demand

Possible future shortage of transformers again

Demand risk is low → execution becomes the key variable

Company is transitioning from single-product (CRGO) → multi-product transformer ecosystem

New segments:

Radiators

Revenue starts Dec-26 onwards — Strong demand + limited organized supply

Nanocrystalline cores

High-margin niche product — Gradual ramp-up

Copper conductors (CTC/PICC)

Capex: ₹25–30 Cr for Revenue potential: ₹150–200 Cr — Commercialization in FY27

7.3 Risk at Current Valuation

Margin Normalization Risk (Most Important)

Margins due to: CRGO shortage and supply disruptions

If supply normalizes Margins can compress

Execution Risk in Capacity Ramp-up

FY27 growth dependent on capacity expansion

Slower ramp-up, operational inefficiencies and delayed utilization could impact ₹1,000 Cr revenue target for FY27

CRGO Price Volatility

Raw material is imported — price volatile

Impacts: Working capital + Margins (if pass-through lags)

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer