Vilas Transcore FY25 Results: PAT Up 48%, Targets ₹ 1,000 Cr Revenue by FY27

Guides 60%+ revenue CAGR by FY27, led by capacity, improving product mix, exports, margin expansion, and potential valuation re-rating from current premium levels.

1. Transformer Lamination, Toroidal Cores, and CRGO Slitted Coils.

vilastranscore.com | NSE - SME: VILAS

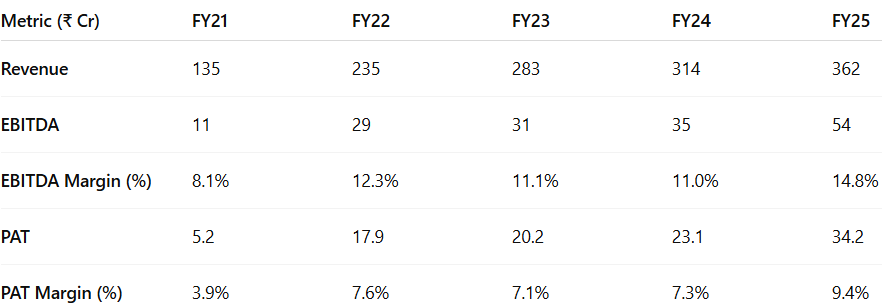

2. FY21-25: PAT CAGR 60% & Revenue CAGR 28%

2.1 Business Evolution: FY21–FY25

Capacity: From 12,000 MTPA (fully utilized) to 36,000 MTPA commissioned in FY25

Product Mix: Moved beyond CRGO laminations to radiators & nanocrystalline cores

Market Reach: Domestic-focused to early-stage exports (Gulf, EU, Canada)

Customer Base: From core OEMs (Voltamp, Electrotherm) to wider infra & energy segments

Capital Structure: Net-debt free, IPO-funded expansion in FY24–25

Execution: Cost control, product diversification, and operating leverage visible

FY26 Ready: Infrastructure in place to scale to ₹ 1,000 Cr revenue

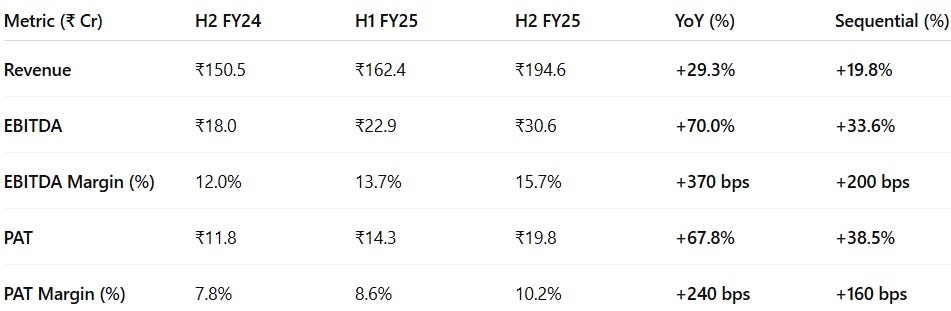

3. H2-25: PAT up 68% & Revenue up 29% YoY

PAT up 39% & Revenue up 20% sequentially

Sequential acceleration across all key metrics signals strong operating leverage.

YoY margin expansion driven by improved cost management, CRGO availability, and improved realization.

H2 FY25 marks highest-ever EBITDA & PAT, supporting a robust FY26 growth outlook.

4. FY-25: PAT up 48% & Revenue up 15%

Strong top-line growth: driven by full utilization and higher volume.

Operating leverage: better scale, stable CRGO prices, and improved mix.

Robust profitability: disciplined cost control and lower finance cost (company remains net-debt free).

Margins at peak levels: Highest EBITDA and PAT margins in company history, laying foundation for FY26 ramp-up.

5. Business Metrics: Strengthening Return Profile

Margin expansion & capital efficiency amid capacity constraints

FY22–FY23 Peak Efficiency: Return ratios surged post-COVID as full capacity utilization, strong transformer sector demand, and pricing discipline led to high asset productivity and strong operating leverage.

FY24–25 Investment Phase: Returns have normalized due to IPO-led equity infusion and partial deployment of new capacity (only 50% utilized in FY25). Despite this, return ratios remain resilient, supported by improving margins and a net debt-free balance sheet.

Outlook: ROCE is expected to rebound once the new 36,000 MTPA capacity is fully utilized by FY27, with incremental contribution from high-margin products like nanocrystalline cores and radiators.

6. Outlook: 60%+ Growth in FY26 with 200 bps Margin Expansion

Driven by new capacity, product ramp-up, and demand tailwinds

6.1 FY25 Expectations vs Performance — Vilas Transcore Ltd

✅ Hits in FY25

Robust Revenue Execution: Revenue grew 15% YoY despite capacity constraints, with full utilization (12,069 MT) of legacy plant and no contribution yet from the new facility.

Margin Expansion: EBITDA margin improved by 380 bps to 14.8%, driven by stable CRGO prices, disciplined pricing, and improved product mix.

Strong Balance Sheet: Net debt-free status maintained, with ₹112 Cr cash on books and healthy ROE (16.4%) despite IPO-led equity base expansion.

New Capacity Commissioned: 36,000 MTPA facility (24k lamination + 7.2k radiator + nano cores) entered trial stage in March 2025; commercial production begins Q1 FY26.

Product Diversification: Radiators and nanocrystalline cores lined up to scale in FY26 — both offering significantly higher margins (20–25%).

Customer Base Expansion: Added new marquee clients across transformer and renewable segments; export base widened to Gulf, Europe, and Canada.

❌ Misses in FY25

Capacity Ramp Delay: Commercial operations for new plant delayed from Jan to July due to floods and statutory approvals, capping topline potential.

Working Capital Build-Up: Inventory and receivables rose ahead of capacity scale-up; short-term borrowings increased temporarily to manage CRGO stocking.

Return Ratio Dip: ROCE dropped to 17.7% from 22.0% YoY due to equity base expansion and underutilized new assets.

Export Contribution Still Modest: Exports remained at ~3–4% of revenue; FY26 to see higher traction once new product lines stabilize.

6.2 Outlook for FY26 and Beyond

Aggressive scale-up backed by strong demand visibility and capacity headroom

FY26–FY27: Transformational Growth Phase

And looking to the present market situation and market demand, we don't see big challenge here. I said next year, we will achieve a INR600 crores of turnover. And financial for year '27, INR1,000 crores.

FY26 Guidance: Management reiterated confidence in achieving ₹600 Cr revenue (~66% YoY growth) driven by:

Ramp-up of the new 36,000 MTPA capacity (CRGO laminations + radiators + nanocrystalline cores)

Full utilization of the legacy 12,000 MTPA capacity

Margin expansion through high-value product mix

FY27 Ambition Raised:

Management has now publicly guided for ₹1,000 Cr turnover in FY27 — a 66.7% YoY jump over FY26, indicating:Strong demand visibility across transformer and renewables sectors

High confidence in operational readiness and supply chain execution

Gradual ramp-up in exports and radiator/nano core contributions

Profitability Levers Intact

EBITDA Margin: Expected to stay in the 16.5–17% range as higher-margin products scale

PAT Margin: Management expects 11–12% range, aided by operating leverage and limited capex post-FY26

ROCE: Forecast to rebound to 20%+ as the asset base sweats over FY26–27

Structural Growth Beyond FY27

Targeting leadership in the transformer ancillary ecosystem, offering CRGO, wound cores, radiators, nano/amorphous cores

Export revenue to rise from current ~3% to 15–20% of revenue by FY28

With full capacity likely utilized by FY28, company may explore brownfield expansion or backward integration

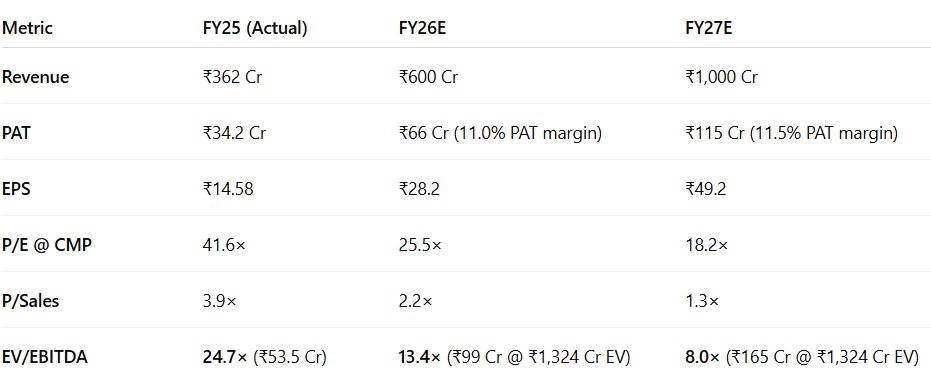

7. Valuation Analysis — Vilas Transcore Ltd

7.1 Valuation Snapshot

Assumptions:

EBITDA Margin: 16.5% (steady across FY26–27, based on margin guidance)

PAT Margin: FY26: 11.0% & FY27: 11.5% (modest expansion from product mix and scale)

Valuations move from expensive (FY25) ➝ fair (FY26) ➝ undervalued (FY27).

Earnings, not re-rating, will drive returns going forward.

Execution of ₹1,000 Cr/₹115 Cr PAT guidance in FY27 justifies further upside.

If management meets its ₹1,000 Cr revenue and ₹115 Cr PAT target in FY27, current valuations may understate the true potential.

7.2 What’s in the Price?

The current valuation (~42× P/E TTM, ~25× forward P/E) reflects high investor confidence in FY26–27 execution.

PAT CAGR of ~48% over FY25–27 and 20%+ ROCE by FY27 are priced in.

Forward EV/EBITDA of 13.4× (FY26) and 8.0× (FY27) implies a valuation premium to transformer ancillary peers.

Implied in valuation:

Execution of ₹600 Cr in FY26 and ₹1,000 Cr in FY27

Ramp-up of radiator + nanocrystalline products

Margins stabilizing at 16.5–17% with high product mix contribution

Working capital normalization by FY27

Full execution is priced in. Any slip in margin, mix, or volume may trigger a de-rating.

7.3 What’s Not in the Price?

Upside triggers remain underappreciated:

Exports: FY27 guidance doesn’t bake in full potential of exports (~15–20% revenue potential by FY28+)

Premium Product Upside: Faster-than-expected scale-up of radiators/nano cores could boost margins above 17%

Amorphous/Nano Core Visibility: New client wins or import substitution could expand addressable market

Brownfield Expansion Optionality: No expansion priced in beyond 36,000 MTPA; possible capacity trigger post-FY27

Valuation Re-Rating: Could move to 28–30× P/E or sub-8× EV/EBITDA if ROCE sustains >24% by FY27

7.4 Risks and What to Monitor

Execution delays or external shocks could derail valuation confidence.

Volume Growth: Deliver > 27k tons sales in FY26

Product Mix: >30% revenue from radiators + nano cores by FY27

UPT/Ramp-Up: 2+ new radiator clients or nano tech wins by FY27

Cost Discipline: Maintain 20%+ PAT CAGR through FY27

CRGO Price Volatility: Spot price spikes could compress margin

Working Capital: Inventory/receivable absorption by FY26

Regulatory Risk: Any changes to transformer input import norms

Vilas offers limited room for execution error — but also strong asymmetric upside if exports, premium products, and volume ramp materialize faster than modeled.

8. Implications for Investors

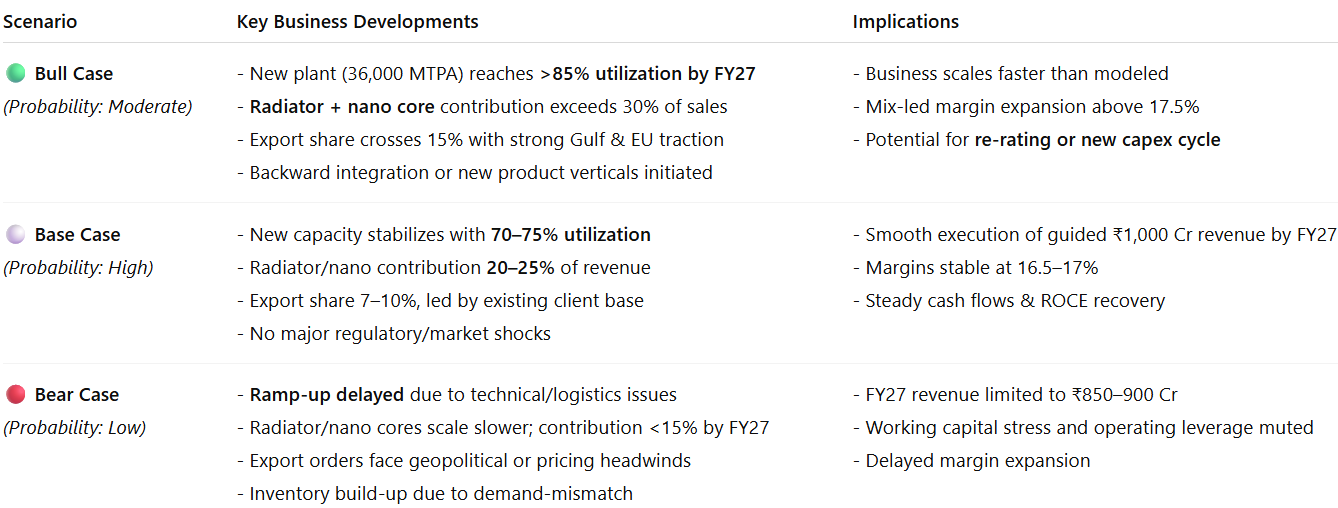

8.1 Bull, Base & Bear Scenarios — Vilas Transcore Ltd

Base Case assumes steady execution of the guided plan — high confidence.

Bull Case unlocks optionality in exports, premium mix, and faster ramp-up.

Bear Case driven by operational delays or external shocks, not structural weakness.

8.2 Is There Any Margin of Safety?

✅ Where There Is Margin of Safety

Business Quality & Model

Long customer relationships with transformer OEMs & utilities

Product mix shift (radiators, nano) adds margin levers

Proven cost control: FY25 EBITDA margin already 14.8%

Capital Structure

Net cash positive: ₹100+ Cr surplus in FY25

IPO-funded expansion; no dilution or leverage risk ahead

Capex behind, asset sweating begins FY26 onward

Execution Levers Not Yet Priced In

Radiator/nano core contribution still minimal in FY25

Faster-than-modeled scale-up could take FY27 revenue to ₹1,100+ Cr

Export ramp and margin kicker (20–25% from radiators) still optionality

Valuation vs Future Earnings

FY27 EPS of ₹49.2 → at CMP, P/E ~18× = 2.5+ years of earnings locked in

EV/EBITDA drops to 8.0× by FY27 — <12× sweet spot for high-quality industrials

❌ Where There Isn’t Much Margin of Safety

Valuation Is Full

Current P/E of 41.6× (TTM) and ~25× forward reflects high expectations

Execution priced in; little room for error or delay

EV/EBITDA of 13.4× (FY26E) implies mid-cycle valuation for a business still scaling

Execution & Market Risks

Radiator mix may ramp slower than expected

Export volumes or CRGO pricing may impact FY26 cash flows

Working capital absorption risk remains (inventory + receivables ↑)

FY25–26 valuation leaves little room for disappointment, but also rewards any upside surprise in margins, exports, or faster ramp.

If Vilas delivers ₹1,000 Cr / ₹115 Cr PAT in FY27, current prices imply limited downside and optional upside — provided execution holds.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

Hi thank you for the write up! Just wanted to check on where has the management guided for 11-12% PAT margin?

Thank you!!