Utssav CZ Gold FY26 Results: Profit Up 136%, Strong FY27 Guidance

Utssav Gold guides for 60% revenue growth in FY26 with stable margins after delivering a strong results in FY26. Available at attractive FY27 forward valuations

1. Designs & Manufactures Gold Jewellery

utssavjewels.com | NSE - SME: UTSSAV

Utssav was established in 2007 and manufactures/designs/wholesales gold and diamond jewellery. Its core is 18K, 20K and 22K CZ / rose gold jewellery, but it has now diversified into plain casting jewellery, natural diamond jewellery and lab-grown diamond jewellery. The model is 100% B2B, supplying retailers across India and now trying to scale exports.

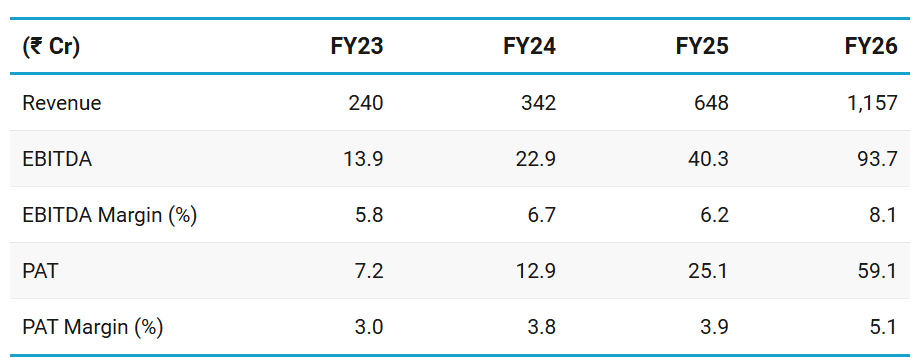

2. FY23–26: PAT CAGR of 102% & Revenue CAGR of 69%

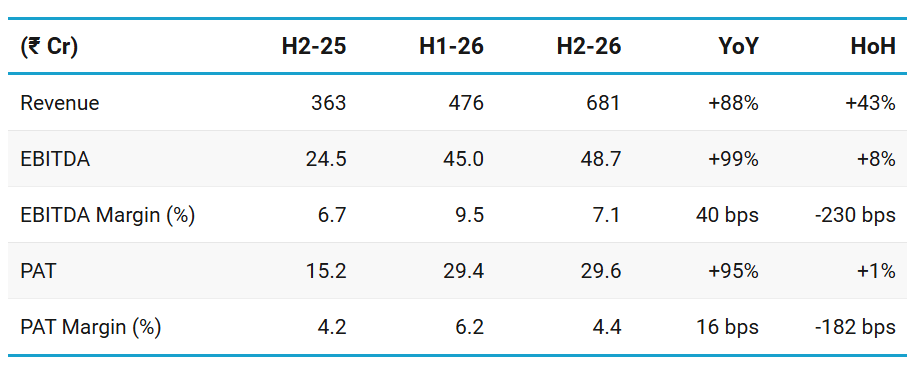

3. H2-26: PAT up 95% & Revenue up 88% YoY

PAT up 1% & Revenue up 43% HoH

H2 FY26 margins softened because the product mix moved toward lower-margin / higher-gold-value categories, especially plain gold and 22K jewellery.

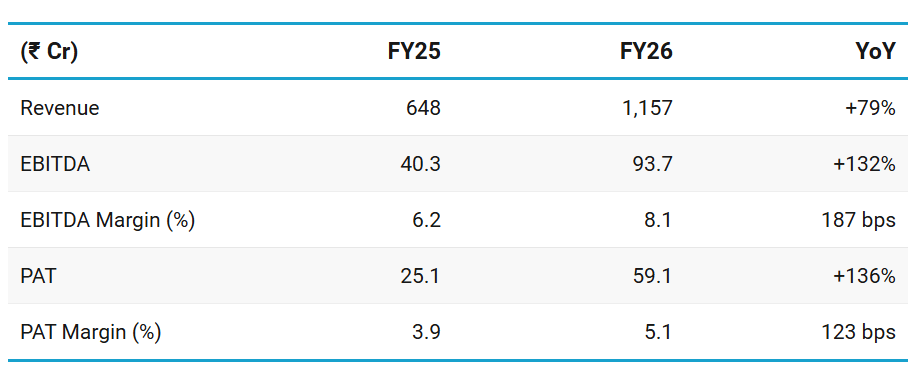

4. FY26: PAT up 136% & Revenue up 79% YoY

Quality of performance is mixed because operating cash flow remained negative despite strong profits.

So the FY26 story is: — Great growth. Better margins. Weak cash conversion. Rising working capital.

Strong operating growth, helped by festive/wedding demand, repeat business, deeper market penetration and new client additions

112 new clients in FY26, while continuing to expand across India and abroad.

Product mix shifted sharply toward 22K jewellery — 22K jewellery became the largest category, rising from 36.6% of revenue in FY25 to 59.5% in FY26.

Inventory and receivables rose sharply. That is why profits did not convert into operating cash.

Growth is being funded through working capital and debt, not internal cash generation yet.

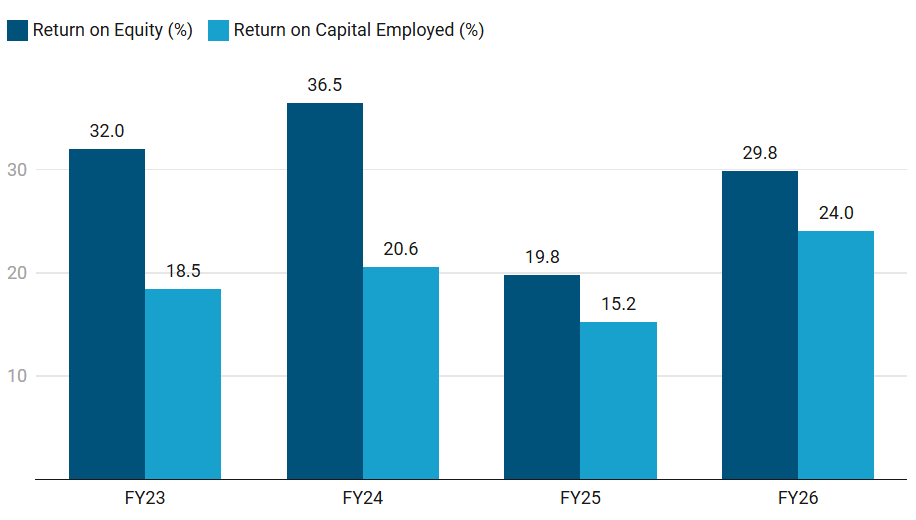

5. Business metrics: Strong & Improving Return Ratios

Utssav is generating strong accounting returns, but operating cash flow was negative in FY26.

Can Utssav keep ROE/ROCE high while funding growth without debt and working capital running ahead of profits

For FY27, watch whether ROCE stays above 20–25% after more borrowing and inventory build.

That will confirm if Utssav is compounding capital or only scaling revenue.

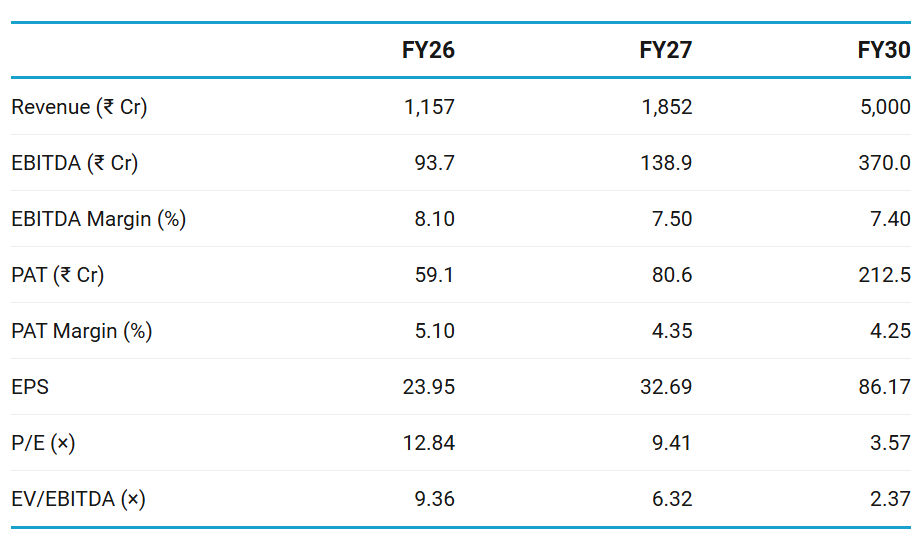

6. Outlook: FY27 Growth of 60%; ₹5K Cr by FY30

6.1 Guidance

FY27

We are looking out for growth around 60% from last year.

Around 30% to 40%, I'm looking for a volume growth this year. And around 60% as business growth.

4% to 4.5% PAT margin and EBITDA around 7% to 8%

Maintaining previous guidance

FY 2030, we look around INR4,000 to INR5,000 crores

With same margins. Or maybe a better margin if, because we recently started Real Diamonds. As their sales will increase and percentage starts growing in our company, so margins might improve

Annual capacity: Approximately around 6 to 7 tons.

FY27 growth guidance

60% revenue growth in FY27

Volume growth of 35–40% — remaining growth dependent on gold price movement and value mix.

Margin guidance

EBITDA margin of 7–8% and PAT margin of 4–4.5%.

Guiding for a lower normalized margin due to the addition of plain gold jewellery, which is lower-margin than some other categories.

Capacity expansion

Capacity ~2,500 kg, with utilization around 65%, rising up to 90% in season, and expected FY27 utilization of 70–75%.

Acquiring more space/buildings and eventually moving capacity toward 6–7 tonnes per year.

~₹50 Cr capex / additional funds for the year, to be funded through bank borrowing, not equity — debt/equity should remain below 1x.

Diamond jewellery opportunity

Diamond jewellery is currently small, about 2% of revenue

To reach more than ₹200 Cr annual sales in the next two years.

It broadens the product mix, but management also said blended margins will still likely remain around 7–8% EBITDA and 4%+ PAT

Export / UAE subsidiary

Exports are currently tiny — very bullish on the UAE subsidiary.

Once the UAE subsidiary starts, export sales could jump to 10–20% immediately.

Looking at GCC, Singapore, Malaysia and Australia through distributor partnerships and exhibitions.

Key upside lever — but it is still unproven.

FY26 exports were only ₹9.47 Cr

Long-term FY30 target

Maintained its earlier target of ₹4,000–5,000 Cr business by FY30 — very aggressive growth from FY26 revenue of about ₹1,155 Cr.

6.2 FY26 Performance vs FY26 Guidance

We are confident of closing the year in the range of INR1,100 crores to INR1,200 crores

9% to 10% should be EBITDA sustainable.

Strong P&L delivery. Weak Cash-flow delivery

Revenue: As per guidance

EBITDA Margin: Lower than the 9-10% guidance range given in H1-26

PAT Margin: Stronger than 4.5–5% range given in H1-26

Cash flow: Weak — Negative operating cash-flow despite solid growth

7. Valuation Analysis — Utssav CZ Gold

7.1 Valuation Snapshot

Current Market Price= ₹307.50; Market Cap = ₹742.55 Cr

Attractively priced on a FY26 basis

Opportunity to re-rate to ~15-20× P/E based on FY27 EPS

Cheaper than Sky Gold on FY26 valuations

Utssav is much smaller than Sky Gold

Longer-term story of FY30 if delivered — opportunity for significant upside ~5×

Utssav CZ Gold Jewels appears undervalued on FY26 metrics — with re-rating potential as it delivers on FY27 guidance

7.2 Opportunity at Current Valuation

Attractive Valuations: At FY26 P/E of ~13×, EV/EBIDTA of ~10× the valuations don’t seem to be discounting FY26 performance. Potential for re-rating of multiples based on FY26 execution

Utssav is much smaller not as established than Sky Gold — reason for significant discount compared to Sky Gold

Forward Valuations are not demanding: With a At FY27 P/E of ~9×, EV/EBIDTA of ~6× there is a strong margin of safety in the stock even if guidance is not fully met

Large Headroom for Growth:

Transition toward organized jewellery retail is a structural tailwind

New Capacity coming in to support near-term growth

Vision of ₹4,000-5,000 Cr revenue by FY30 provides a longer term story in Utssav

Global Optionality:

Expanding exports to UAE etc will improve margins

7.3 Risk at Current Valuation

Lowered Guidance: Guidance of 60-70% growth for FY27 in H1 FY26 earnings call reduced to 60% for FY27 during H2 FY25 earnings call

Typical risks with any small-cap with limited track-record of management as public company persist

Quality of Earnings — Negative cash flow as typically seen in a high growth company

Risk is profits do not convert to cash

Previous Coverage of Utssav CZ Gold Jewels Ltd

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer