UGRO Capital Q4 FY25 Results: AUM up 31%, Disciplined FY26 Outlook, Deep Value Opportunity

Targets secured-led AUM growth, improved productivity, and calibrated credit costs in FY26. Valuations remain low, but disciplined execution strengthens the re-rating case.

Table of Content

Financial Performance Snapshot

Management Commentary & Outlook

Valuation Deep Dive

Implications for Investors: What to Watch

1. UGRO Capital Financial Performance: FY25 Results & Q4 Highlights

UGRO Capital ended FY25 with record-breaking growth in disbursements and assets under management (AUM), underscoring its execution strength in the competitive MSME lending space. The NBFC’s digital-first, co-lending-driven model helped expand reach, while maintaining asset quality across key segments.

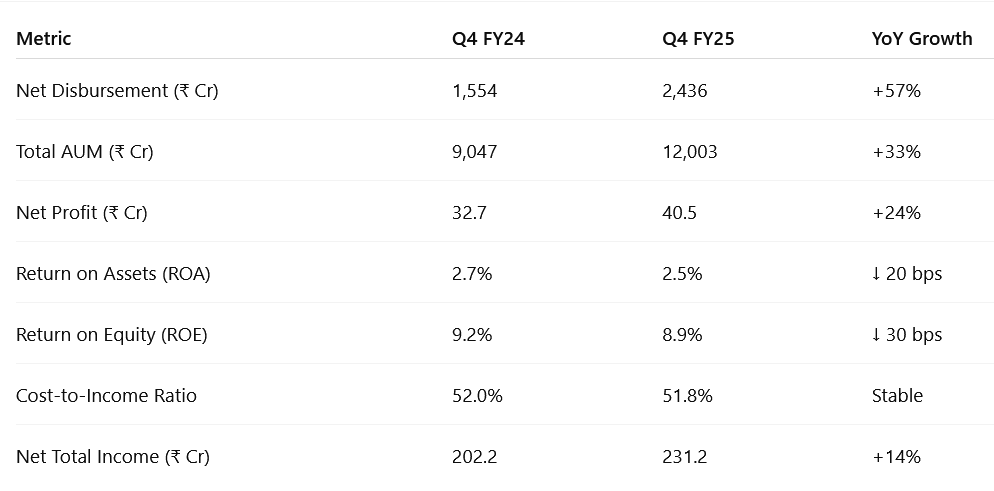

1.1 Q4 FY25 Performance Snapshot: UGRO Capital Earnings & Growth Momentum

UGRO Capital closed Q4 FY25 with record quarterly disbursements and healthy asset quality, reinforcing its execution capability across MSME-focused lending segments. The company’s multi-channel strategy and digital underwriting tools continue to power growth despite macro headwinds.

Key performance drivers:

Emerging Market disbursements rose to ₹669 crore (vs ₹203 crore YoY), now forming 27% of Q4 disbursements — a sign of deepening rural MSME outreach.

Embedded Finance (MSL platform) contributed ₹638 crore in Q4 disbursals and reached ₹743 crore in AUM.

Borrowing cost remained stable at ~10.6% despite higher leverage and expansion.

UGRO Capital’s Q4 FY25 results show strong momentum heading into FY26, supported by tech-enabled credit processes and rising penetration in high-yield lending segments.

1.2 FY25 Performance Summary: UGRO Capital Earnings & Growth Drivers

Despite a marginal dip in profitability ratios due to branch expansion and credit provisioning, UGRO Capital demonstrated strong operating leverage. The company also retained a high off-book AUM mix (42%) — showcasing its capital-light co-lending model as a key competitive advantage.

1.3 Lending Segment Analysis: What Drove UGRO Capital’s Growth

UGRO Capital’s FY25 lending book shows clear signs of diversification and yield optimization:

What stood out in FY25:

High-yield products (embedded finance, EM LAP) contributed to top-line growth.

Strategic pullback in unsecured business loans helped manage portfolio risk.

Low GNPA across most categories confirms strong credit underwriting via UGRO’s Gro Score AI system.

2. UGRO Capital Management Commentary & Strategic Outlook

UGRO Capital enters FY26 with a calibrated approach to growth, emphasizing quality over quantity, profitability over pure AUM scale, and deeper execution across existing business lines. The strategy varies across lending verticals but maintains a consistent focus on risk-adjusted returns, operating leverage, and disciplined expansion.

2.1 FY26 Guidance & Execution Themes by Lending Channel

UGRO has not issued consolidated revenue or PAT guidance, but its lending channel-level plans offer clear forward-looking direction.

Emerging Market: Secured Loans

FY25 Disbursement: ₹669 Cr | Branches: 212

FY26 Strategy: Significant increase in disbursement expected as branch count expands to 400.

Credit Outlook: GNPA to rise from 2.6% to 3.7–4%; credit cost to increase by 30–50 bps due to portfolio aging.

Yield: May improve by 30–40 bps with optimized loan mix.

Prime Intermediated: Secured Business Loans

FY25 Disbursement: ₹299 Cr | Productivity: ₹1.10 Cr/FOS

FY26 Strategy: Planned increase of 15–20% in both disbursement and productivity.

Credit Outlook: GNPA expected to stabilize at 0.8–1%; pricing pressure anticipated due to competitive intensity.

Prime Intermediated: Business Loans (Unsecured)

FY25 Disbursement: ₹285 Cr

FY26 Strategy: Planned 25–30% reduction to rebalance the portfolio in favor of secured products.

Credit Outlook: GNPA to remain elevated at 4%; credit cost expected to rise by 20–25 bps as the book runs down.

Ecosystem Channel & Green Asset Finance

FY25 Disbursement: ₹287 Cr

FY26 Strategy: Disbursement and productivity to increase by 15–20%.

Credit Outlook: GNPA to reduce to 1.0–1.1%; credit cost may rise 10–15 bps with portfolio vintage impact.

Direct & Digital Alliances

Alliances Disbursement: ₹308 Cr | Partners: 64

FY26 Strategy: Maintain steady scale and unit economics. All key metrics expected to continue at current levels.

Embedded Finance

FY25 Disbursement: ₹638 Cr | Yield: 26% | GNPA: 0.2%

FY26 Strategy: No change in operating model; however, GNPA expected to rise to 2.7–3% as book matures.

2.2 FY26 Strategic Priorities

Scale Emerging Market Lending Through Branch Expansion

UGRO plans to increase its Emerging Market branch count from 212 to 400 in FY26.

This is expected to drive a significant increase in disbursement volumes, particularly in secured LAP and MSME products.

These branches serve as the backbone of UGRO’s retail-led expansion, with a consistent monthly productivity of ₹1.1 Cr per branch.

Largest contributor to AUM growth; critical for balancing secured exposure against riskier unsecured books.

Improve Productivity Across Sales Channels

In the Prime Secured and Ecosystem channels, disbursement productivity per FOS (Feet-on-Street) is expected to rise by 15–20%.

UGRO has not added new product lines, choosing instead to focus on operational efficiency from existing capacity.

Ecosystem disbursements (₹287 Cr in Q4FY25) and Green Asset Finance will be driven by improved FOS efficiency, not headcount growth.

Margin uplift through operating leverage; higher RoA without additional opex.

Moderate High-Risk Lending in Unsecured Segments

UGRO is reducing disbursement in unsecured business loans by 25–30%.

The GNPA in this book stood at 4% in FY25, and credit cost was 1.9%.

This is an intentional move to improve the risk-adjusted return profile of the overall portfolio.

Strengthens balance sheet; lowers provisioning drag; reallocates capital to secured and embedded models.

Deepen Co-Lending and Embedded Finance Model

UGRO's co-lending book forms ~42% of total AUM and will be maintained at this level.

Embedded Finance, with 26% yield and ₹638 Cr disbursement in Q4FY25, will continue at scale but with caution as GNPA is projected to rise from 0.2% to 2.7–3%.

Focus remains on expanding high-margin, short-tenor loans while managing portfolio seasoning impact.

Key ROE driver; high-yield channels balanced with proactive credit cost management.

No New Products: Prioritize Execution Excellence

Management has explicitly stated that no new products will be launched in FY26.

The objective is to consolidate gains from existing verticals, ensure credit quality stability, and maximize productivity per channel.

Reduced execution complexity; enhances focus on profitability and credit discipline.

Strategic Theme: Shift From “Grow Fast” to “Grow Smart”

UGRO Capital’s FY26 plan reflects a tactical pivot:

From volume-first to margin-first growth.

From expansion to consolidation.

From new product launches to deepening distribution of tested verticals.

2.3 Management Commentary Summary

The management emphasized a “calibrated growth strategy”—intentionally slowing growth in high-risk, high-yield segments like unsecured business loans, while doubling down on secured MSME lending through expanded branch footprint and ecosystem-led channels.

Their approach reflects a transition from the “build and expand” phase of FY24–25 to a “consolidate and optimize” phase in FY26, ensuring that growth is sustainable, diversified, and profitable.

3. UGRO Capital’s Valuation Deep Dive

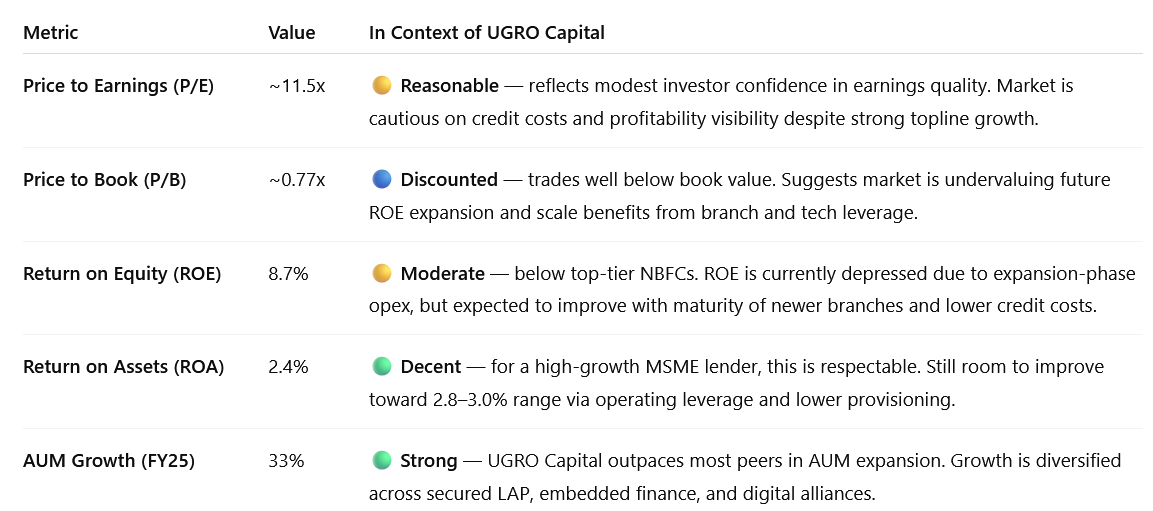

3.1 UGRO Capital’s Key Multiples in FY25 Context

UGRO Capital trades at a deep value relative to peers, with both P/E and P/B ratios leaving room for re-rating. The business is still transitioning from high investment mode to profitability expansion. As returns scale and credit performance stabilizes, valuation multiples could expand significantly, especially given the consistent 30%+ AUM growth.

3.2 Peer Comparison: UGRO Capital vs Other High-Growth NBFCs

When benchmarked against other high-growth NBFCs in India, UGRO Capital stands out for its differentiated strategy—but still remains underappreciated by the market. While peers like MAS Financial, Aavas Financiers, and Bajaj Finance trade at premium valuations, UGRO’s pricing reflects a gap between execution and perception.

Business Model Positioning

Unlike traditional NBFCs focused on single-product lending (e.g., Aavas in housing, MAS in small enterprise finance), UGRO Capital operates a multi-engine model—offering secured business loans, LAP, machinery finance, and embedded MSME credit through digital alliances. This diversified strategy spreads risk, but also requires time to prove consistency across channels.

Scale vs. Perception

While UGRO has scaled AUM rapidly (₹12,000 Cr+ in under five years), it lacks the legacy trust premium that benefits players like Bajaj Finance or Shriram Finance. The market appears to be in a “wait and watch” mode, demanding sustained profitability and stable asset quality before awarding a valuation uplift.

Capital Efficiency

UGRO Capital’s co-lending model—where 42% of AUM is off-book—is a structural strength that many peers are only beginning to adopt. This allows for capital-light expansion, which, if executed well, could drive superior Return on Assets (ROA) and Return on Equity (ROE) over time.

Valuation Disparity

Peers with similar or even slower AUM growth command higher price to book multiple, while UGRO trades at ~0.77x. This disparity is stark and could narrow meaningfully if UGRO continues to deliver on credit quality, profitability, and operating leverage.

3.3 What’s Built Into the Price Today

At a valuation of ~0.77x P/B and ~11.5x P/E (FY25), UGRO Capital’s current market price reflects a cautious investor stance. The stock appears to be pricing in growth—but with heavy discounting on sustainability, profitability, and credit quality.

Rapid AUM Growth Is Expected

The market acknowledges UGRO’s consistent 30%+ AUM growth and its ability to originate loans across diverse MSME segments. The current valuation does reflect that UGRO is no longer a startup—it has achieved scale.

Moderate Return Ratios in the Near Term

With ROE at 8.7% and ROA at 2.4%, investors seem to be assigning value based on near-term profitability ceilings. There’s an implicit assumption that return ratios will take time to reach peer benchmarks.

Execution Risk from Portfolio Mix

The discount to book suggests that investors are pricing in volatility from the unsecured and high-yield lending book, particularly business loans and emerging market LAP, where GNPA trends require close monitoring.

Early-Stage Operating Leverage

With 235 branches and large parts of the distribution still in ramp-up phase, there is limited expectation—yet—of significant cost-to-income improvement. Market pricing seems to reflect a wait for operational maturity.

3.4 What’s Not Fully Priced In Yet (Optional Upside)

Despite its strong AUM growth and differentiated model, UGRO Capital’s current valuation does not reflect the full extent of its long-term upside. Several structural and strategic levers remain underappreciated by the market—and could trigger a re-rating as execution plays out.

Tech-Led Underwriting at Scale

UGRO’s Gro Score 4.0, built on alternate data (GST, bureau, banking), enables faster and more accurate credit decisions. Unlike legacy NBFCs, UGRO is embedding data-science-driven underwriting across all verticals. If loss ratios remain controlled, this capability could justify a premium tech-NBFC valuation over time.

Operating Leverage from Branch Productivity

UGRO has made front-loaded investments in a 235-branch network. However, most branches are still in ramp-up mode. As disbursement per branch rises in FY26 and FY27, cost-to-income ratio could decline meaningfully, boosting ROA and ROE—an inflection the market hasn’t yet priced in.

High-Yield Embedded Finance Model

With ~₹743 Cr AUM and growing monthly disbursals, UGRO’s embedded finance (MSL) segment delivers 26% yields with sub-0.5% GNPA. If this segment scales to ₹1,500 Cr+ as planned, it could meaningfully lift blended NIMs and drive upside surprise on profitability.

Capital-Light Expansion via Co-Lending

With 42% of AUM already off-book, UGRO’s co-lending strategy allows it to grow without heavy capital infusion. As this share expands, it could drive structural ROE uplift—a lever that few NBFCs have activated at scale.

Brand Recognition and Market Re-rating

Currently, UGRO does not command a legacy premium like Bajaj Finance or Aavas. But if it delivers consistent earnings, improves ROE, and keeps GNPA in check, investor perception could shift—unlocking multiple expansion.

UGRO Capital’s stock is still priced for execution risk, not for strategic leverage. As embedded finance scales, branches mature, and co-lending lifts ROE, the company could move into the "reliable compounder" bracket—where NBFCs typically command 2–3x P/B.

4. Implications for Investors: What to Watch

4.1 Bull, Base, and Bear Case Scenarios for UGRO Capital

4.2 Reasons to Stay Invested or Add on Dips

Valuation Offers Margin of Safety

At ~0.77x P/B and ~11.5x P/E (FY25), UGRO Capital is priced well below sector peers despite similar or higher AUM growth. With a reported net worth of ₹2,046 Cr and strong balance sheet metrics, the stock trades below its intrinsic book value, offering limited downside unless there’s a major deterioration in fundamentals.

Multi-Engine Lending Model Enables Resilient Growth

UGRO’s diversified product mix across secured LAP, machinery loans, embedded finance, and co-lending ensures that growth is not dependent on a single segment. This multi-pronged strategy reduces portfolio concentration risk and supports 25–30% AUM growth without excessive capital consumption.

With embedded finance (26% yield, sub-0.5% GNPA) and emerging markets driving volume, the lending engine is robust even in challenging macro environments.

Early Operating Leverage Set to Kick In

UGRO has already made the upfront investment in building a 235-branch network, data infrastructure, and embedded sourcing partnerships. As these assets mature in FY26 and beyond, incremental disbursements will come with lower marginal cost, improving ROA and ROE.

Co-Lending and Capital-Light Growth Boost Returns

42% of UGRO’s AUM is already off-book through co-lending arrangements, which helps grow without proportionally increasing risk-weighted assets. This is key to boosting return on equity (ROE) without frequent dilution or capital raises—an edge over traditional asset-heavy NBFCs.

Co-lending also diversifies funding sources and reduces dependence on bank lines or bond markets in tight liquidity cycles.

Long-Term MSME Credit Tailwind

UGRO is strategically positioned in the underserved ₹20 lakh–₹2 crore MSME loan segment, where formal credit penetration is still low. As digital adoption and platforms like GST/ONDC expand, UGRO’s tech-enabled approach is poised to ride the next wave of MSME formalization.

India’s MSME credit gap remains a multi-trillion-rupee opportunity—UGRO is playing directly in the heart of it.

4.3 Key Risks & What to Monitor in UGRO Capital

Credit Quality Slippage in High-Yield Segments

The most visible risk is rising GNPA in unsecured business loans and emerging market LAP, where delinquencies can spike in tough economic conditions. In FY25, GNPA rose modestly to 2.3%, and while provisions are adequate for now, any deterioration in borrower behavior or underwriting discipline could lead to a sharp uptick.

What to monitor: Segment-wise GNPA (especially business loans), restructured accounts, and credit cost trends.

ROE Compression from Sticky Operating Costs

UGRO’s ROE stands at 8.7%—lower than peers due to upfront investment in branches and people. If branch productivity doesn’t improve meaningfully in FY26–27, ROE may remain subdued, keeping valuation multiples depressed.

What to monitor: Disbursements per branch, cost-to-income ratio trajectory, and hiring vs growth alignment.

Execution Complexity in Embedded Finance

While embedded finance is a high-growth opportunity, scaling it responsibly is not easy. Challenges include managing ultra-small ticket loans, ensuring real-time fraud detection, and aligning with tech partners (OEMs, fintechs). Any breakdown in these ecosystems could hurt both asset quality and customer experience.

What to monitor: Embedded finance AUM growth, NPA levels in MSL book, partner/channel retention.

Market Perception and Re-Rating Risk

Despite strong AUM growth, UGRO trades at ~0.77x P/B. This reflects a trust discount. If the company fails to consistently improve profitability and ROE, the market may continue to view it as a tactical, not structural, NBFC, limiting investor interest and liquidity.

What to monitor: ROE trends, earnings beat/miss cycles, broker coverage and institutional shareholding.

Macro & Regulatory Overhangs

NBFCs are vulnerable to broader liquidity cycles and regulatory changes. Any tightening in capital norms, restrictions on co-lending, or funding constraints (e.g., rising cost of borrowing) can impact margins and growth.

What to monitor: RBI circulars on NBFCs, bond yield trends, UGRO’s funding mix and cost of capital.

4.4 Investor Segmentation Outlook: Who Should Consider UGRO Capital?

UGRO Capital is not a conventional “blue-chip” NBFC. It is a high-growth, early-stage financial stock in the midst of proving out its operating leverage and credit quality at scale. As such, it appeals to a specific type of investor profile while requiring others to exercise caution.

Long-Term Growth Investors

Best suited for: Investors with a 3–5 year horizon, comfortable with near-term volatility in exchange for the potential of long-term compounding.

Why it fits: UGRO has already proven its ability to scale AUM consistently at 30%+ CAGR. As branch-level productivity and ROE improve, the company could transition into a quality compounder—offering significant price-to-book multiple expansion.

Value Investors

Best suited for: Investors seeking deep value opportunities in sectors with strong structural tailwinds.

Why it fits: UGRO trades at ~0.77x P/B, with improving fundamentals and a differentiated lending model. It presents a classic “value-in-disguise” case where growth is visible, but not yet priced in. If earnings compound at 20–25% CAGR, valuation could rerate without multiple expansion.

Momentum Traders

Caution advised for: Short-term traders looking for breakout charts, near-term triggers, or headline-driven moves.

Why it doesn’t fit: UGRO lacks near-term triggers or institutional momentum. Its re-rating depends on gradual delivery of performance rather than event-based upside. Price discovery will likely be slow and data-driven, not sentiment-fueled.

Risk-Averse Retail Investors

Approach with caution if: You're uncomfortable with earnings volatility, mid-cap illiquidity, or sharp price movements based on quarterly results.

Why it may not fit: The business model is still scaling. Credit cost fluctuations, operating leverage lag, or even macro events could drive price corrections. UGRO requires active tracking, not passive ownership.

UGRO Capital is ideal for investors who can think like owners. If you’re willing to absorb short-term noise, track execution, and align with the long-term MSME lending thesis, this is a stock that could compound from both earnings and valuation multiple expansion.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer