Transformers & Rectifiers India: PAT growth of 2126% & revenue growth of 72% in 9M-25 at a PE of 103

FY25 revenue growth of 43% & EBITDA growth of 87-94%. FY24-27 guidance of EBITDA CAGR of 75-85% & Revenue CAGR of 52-57%. Margin expansion 10.5% to 16-17% by FY27. Order book 1.5X FY25 revenue.

1. Transformer & Reactor manufacturer

transformerindia.com | NSE: TARIL

2. FY20-24: PAT CAGR of 196% & Revenue CAGR of 17%

3. FY24: PAT up 11% & Revenue down 7%

4. Strong Q3-25: PAT up 252% & Revenue up 51% YoY

PAT up 21% & Revenue up 21% QoQ

5. Strong 9M-25: PAT up 2126% & Revenue up 72% YoY

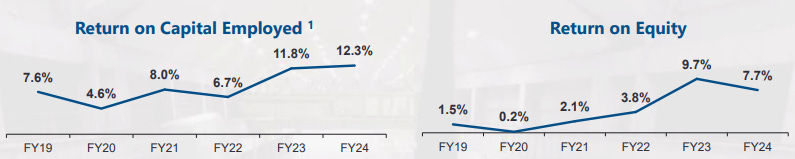

6. Business metrics: Return ratios are not exceptional

7. Outlook: Strong Revenue growth & margin expansion supported by order book

i. FY25: Revenue growth of 43%

Revenue of Rs 2,000 cr in FY25 is a 43% growth over FY24

Rs. 2000 crores is quite achievable and we are working on that

ii. FY25: EBITDA growth of 87-94%

EBITDA margin expansion from 10.4% to 12.5-13% in FY25 implies an EBITDA growth of 87-94%

And EBITDA margin will remain somewhere between 12.5% to 13% levels

iii. FY26: Revenue growth of 75%

Growing to Rs 3,500 cr in FY26 from an expected revenue of Rs 2,000 cr implies a 75% growth in in FY26 and revenue CAGR of 64% for Fy24-25

iv. FY24-27: EBITDA CAGR of 75-85% & Revenue CAGR of 52-57%

Stand alone revenue growing from Rs 1291 cr in FY24 to Rs 4500-5000 cr by FY27 implies a FY24-27 revenue CAGR of 52-57%. EBITDA margin expansion from 10.4% to 16-17% in FY27 implies an FY24-27 EBITDA CAGR of 75-85%

next 3 years we are well posed to reach Rs. 4500 crores to Rs. 5000 crores numbers on a standalone basis with the EBITDA beta levels or somewhere 16% to 17% levels.

Targeting a 17% plus EBITDA margin by FY27.

v. Order book: 1.8X FY25 revenues & 1.1X FY26 Revenue

Order book as of end of Q3-24 is 1.84 times the Rs 2,000 cr revenue expected in FY25. An order book of Rs 4,000 cr by the end of FY25 is 1.14 times the Rs.3,500 cr revenue expected in FY26.

Aiming for an order book of Rs 4,000 cr+ by the end of FY25.S

vi. $1 million revenue by FY28 F29

Will the ambition of $1 bn is noted, our focus is on performance till FY27

Journey towards US$ 1 Billion Revenue in next 3 Financial Years.

8. PAT growth of 2126% & Revenue growth of 72% in 9M-25 at a PE of 86

9. Hold?

If I hold the stock then one may continue holding on to TARIL

Based on H1-25 revenue of Rs 784 cr, the FY25 guidance of Rs 2,000 cr looks achievable. FY26 guidance is achievable with a strong order book to support Rs 3,500 cr revenue.

Revenue target for current Financial Year remains intact

TARIL is pursuing backward integration to secure critical component supplies, and support the guidance for margin expansion. Is is expected to generate significant cost savings and potentially open new revenue streams.

Minimum 4% increase in PAT margin when all backward integration projects are online. Aims to reach a 10% profit after tax (PAT) level.

Acquired controlling stake in a CRGO (Cold Rolled Grain Oriented) processing unit.

Entered into a supply agreement for mother coils.

Three technological tie-ups are aimed at supporting backward integration goals and are expected to be operational by Q4-FY26.

15,000 MVA pre-expansion project is on track and expected to be completed by February-March, with operations starting early next year. This will bring the company to around 55,000 MVA levels.

Aims to be 100% backward integrated in radiators.

Plan to sell some raw materials on the market, but no more than 15% of total capacity.

The Indian power transmission and distribution (T&D) sector is experiencing robust demand driven by government initiatives, grid expansion, and renewable energy investments.

No perceived slowdown in infrastructure development in India, which suggests strong opportunities for business.

10. Buy?

If I am looking to enter TARIL then

TARIL has delivered PAT growth of 2126% and revenue growth of 72% in 9M-25 at a PE of 103 which makes the valuations fully priced in the short term.

TARIL is guiding for EBIDTA growth of 87-90% and revenue growth of 43% in FY-25 at a PE of 103 which makes the valuations fully priced from a FY25 perspective.

TARIL is guiding for for revenue CAGR growth of 64% in FY24-26 at a PE of 103 which makes the valuations fully priced from a FY26 perspective.

The guidance of EBITDA CAGR of 75-85% & Revenue CAGR of 52-57% by TARIL for FY24-27 with improving margins at a PE of 103 creates opportunity from a long term perspective.

Opportunity in TARIL is based on strong execution till FY27. At a PE of 103 the margin of safety is limited. If the execution does not happen as per the guidance there will be substantial downside in TARIL.

For new entrants in the stock it would be a long wait for value to emerge for a beyond FY27 perspective.

Previous Coverage of TARIL

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer