Time Technoplast - Tepid growth for a fair price

Efficiently run company. Stock is priced attractively. Growth outlook is tepid

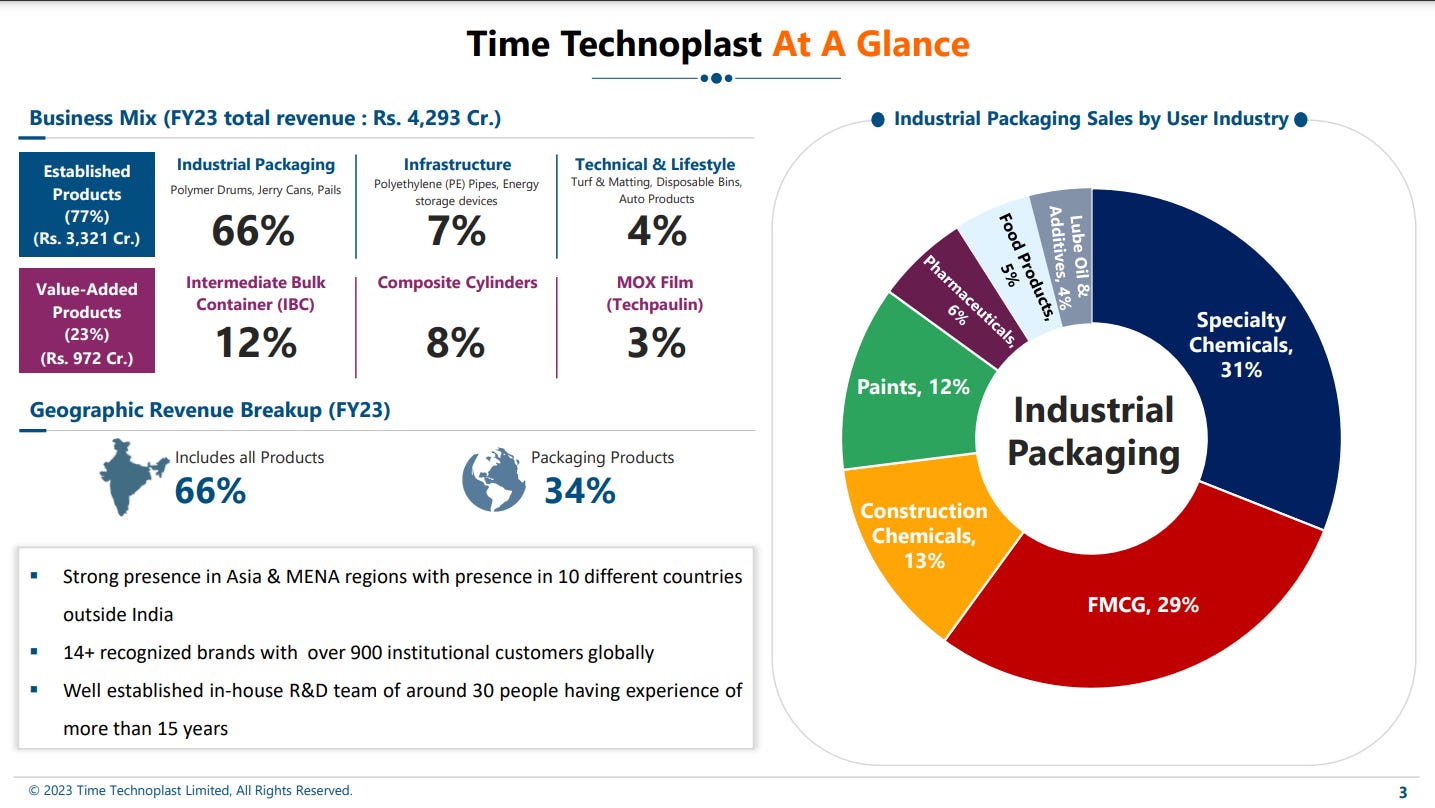

Company Overview

Time Technoplast Ltd is a packaging solutions provider.

TIMETECHNO is the

World’s largest manufacturer of large size plastic drums.

2nd largest Composite Cylinder manufacturer worldwide.

3rd largest Intermediate Bulk Container (IBC) manufacturer worldwide

60% market share in domestic Industrial packaging.

2nd largest MOX film manufacturer in India

Major Player in manufacturing of HDPE pipes in India

TIMETECHNO has approved the consolidation cum restructuring of overseas business in full/part by way of disinvestment of majority stake to Strategic Partner/ Investor Partner. The proceeds will be used for Repayment of Debt, Capex for Composite Cylinders (LPG/CNG/Hydrogen) & Core Business in India

Share Details

NSE:TIMETECHNO ( timetechnoplast.com)

Quality: Returns on capital employed in cash

Return ratios have been consistent over the years. Cash conversion is solid. We are looking at the return ratios of an efficiently run company. However the return ratios are not exceptional

Growth

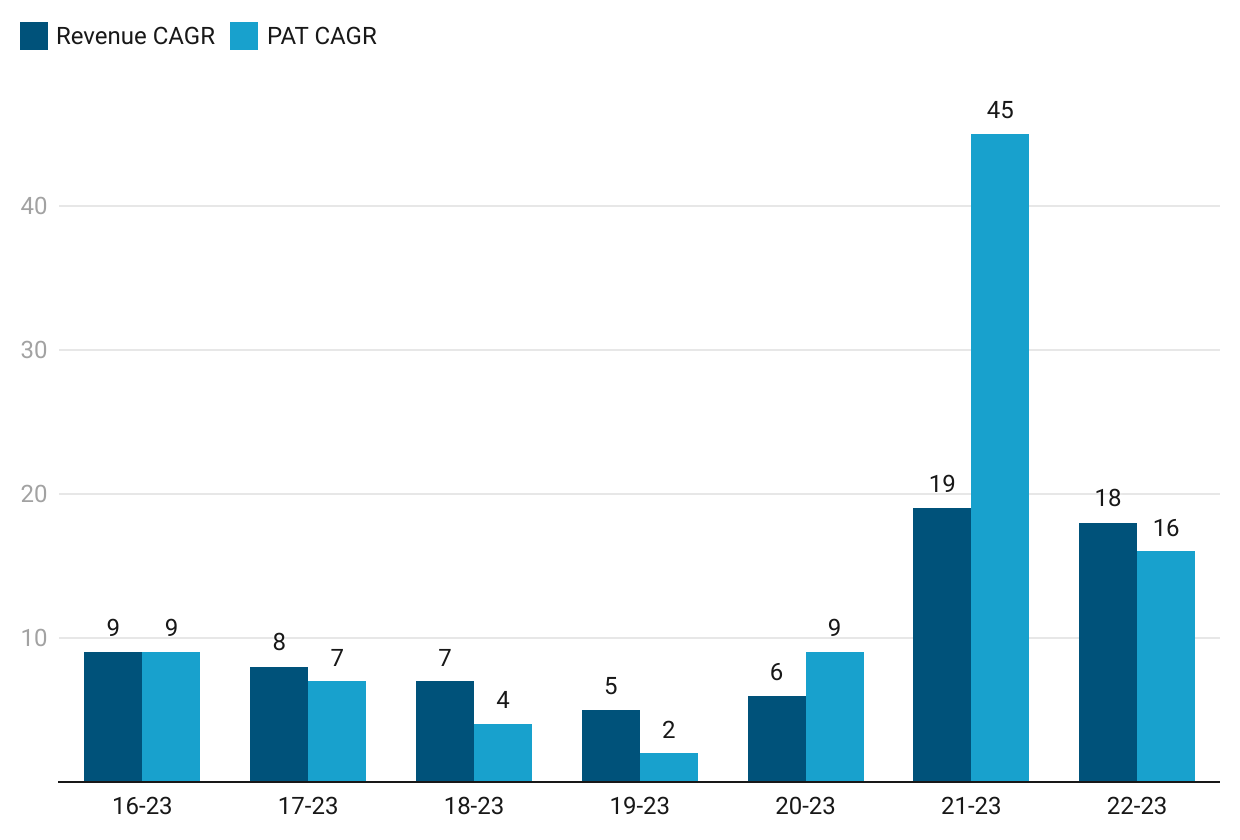

The top-line and bottom-line growth CAGR of 9% is quite an ordinary growth. The company hit a peak in FY19-20 then went down to recover and hit a higher peak in FY22-23 which generates interest in the company.

Growth Momentum

The growth momentum after slowing down has picked up from FY19 onward both on the top-line and bottom-line.

Outlook

Guidance for FY24 does not indicate for a higher growth. Growth will be from 18% in FY22 to a “more than 15%“ growth in FY24. Though improvement in EBITDA will help the bottom-line growth.

Definitely, we will have more than 15% growth and EBITDA level will reach to the 14% as far as current financials is concerned, that is with the present projections.

Guidance for FY24 for the established business (77% of FY23 revenue) indicates a slow down from 15% growth in FY22 to 12% in FY23.

So, as far as the packaging business is concerned, we are estimating growth in the range of around 12%

Future growth will be driven by value-added products.

Today, our value-added products sales is 23%, which I'm projecting will go up to 25% this current year. But if you ask me 3 years down the line, definitely, we will have a 30% value added product. If you ask me the 5 years down the line, then we will have a 35% value added sale. And value-added products very well includes IBC, MOX Film and CNG Cascades.

The company is guiding for a 20%+ ROCE by FY25-26

As far as ROCE target is still there to achieve over 19% in 2024, '25. If you ask me next 3 years, it will be over 20%, that by 2025, ‘26. If you ask especially this year, definitely, the ROCE will be over 16%

The management feels that the stock is undervalued and has increased its stake in the business from 51.33% (Dec-21) to 51.47 (Mar-23) to 51.69% (Jun-23)

So, definitely, as somebody mentioned the Company is undervalued. Yes, promoter will also think on that and that will be the right time to take the entry by the promoters because they have surplus funds available because of this the pledged shares have been paid.

So What????

If I currently hold the stock, I may continue holding it based on my past returns, expectations for future returns, and the availability of alternative stock ideas. One has to keep a watch on the guidance of 15%+ growth. We don’t want to be in the stock which delivers a 9% growth CAGR over the long term.

If I don't currently own the stock, I will have a hard time deciding to enter into the stock. The promoters feel the company is undervalued and are increasing stake. There is a guidance for improving ROCE and EBITDA given a higher contribution of value-added products which makes TIMETECHNO an interesting stock. On the other side a guidance of 15% future growth does not make it a very exciting growth story. Also a PE of around 14 makes it fairly valued so one has to give importance to the entry price.

For those who track book value the stock appears undervalued at book value of around Rs 100 against the current market price of around Rs 133.

Quick back of the envelope book value calculation

ROE of 10% on a PAT of 224 cr implies equity of around Rs 2240 cr.

Market cap of about Rs 3010 cr implies price to book is around 0.74 (2240/3010)

Book value of is about 100 (133*0.74)

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades