Time Technoplast: PAT growth of 40% & Revenue growth of 14% in H1-25 at a PE of 25

Revenue CAGR of 15% for FY24-27. Favorable demand outlook to support revenue growth. Margin expansion as contribution of value added products to increase. Debt reduction to support margins.

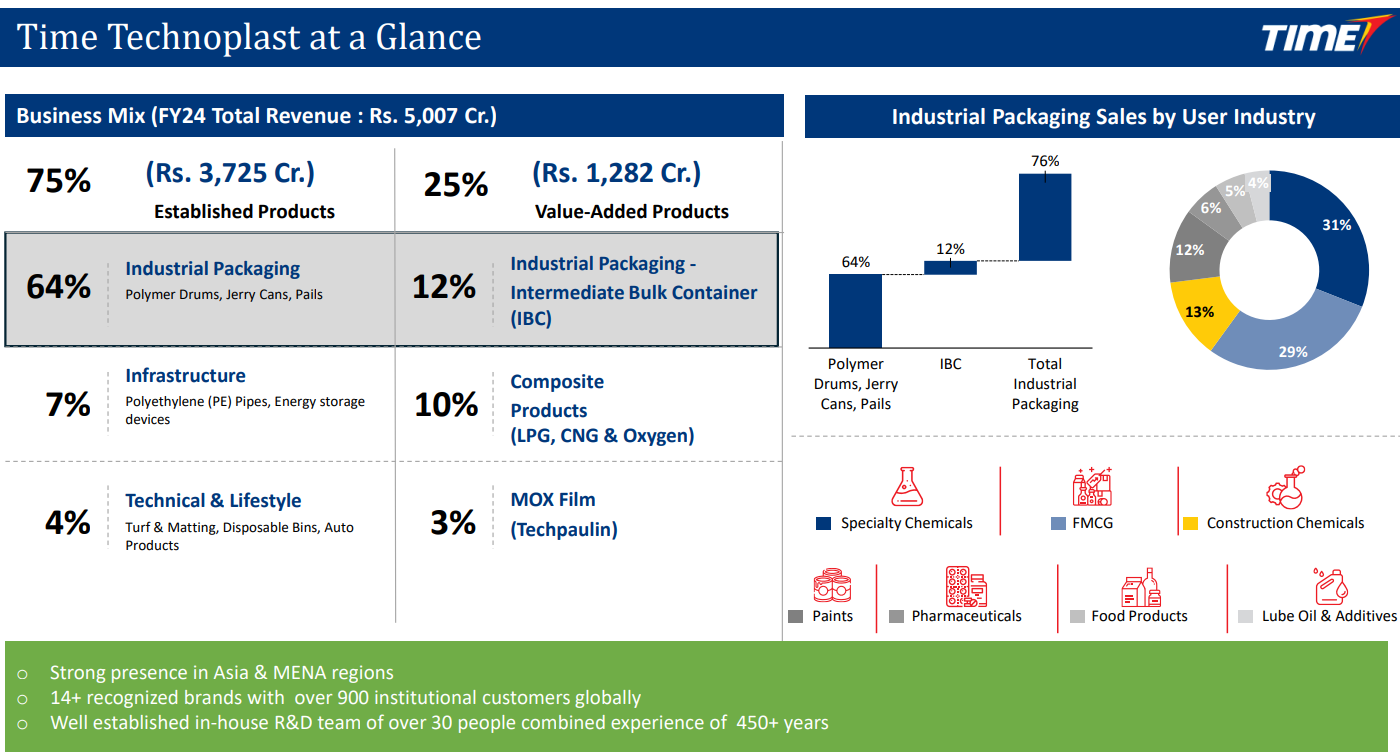

1. Industrial Packaging Company

timetechnoplast.com | NSE : TIMETECHNO

Products

2. FY20-24: PAT CAGR of 16% & Revenue CAGR of 9%

3. Strong FY24: PAT up 42% & Revenue up 17% YoY

4. Strong Q2-25: PAT up 40% & Revenue up 15% YoY

5. Strong H1-25: PAT up 40% & Revenue up 14% YoY

6. Business metrics: Improving return ratios

Return on Capital Employed – H1FY25 : 17%

Focus on increasing ROCE by 2% annually

Achieving an RoCE of ~20% over the next 2 years

7. Outlook: 15% revenue CAGR for FY24-27 with PAT growing faster

Revenue Growth: Time Technoblast is projecting a volume growth of 15% for the next two to three years. This growth is expected to be driven by both its industrial packaging business and its value-added products, including composite cylinders. Revenue growth may vary depending on the pricing of products.

Value-Added Products: The company aims to increase the share of value-added products to 35% of total sales in the next two to three years. Value-added products are projected to grow at 30% year-on-year for at least the next three years. These products command higher margins.

Capacity Utilisation and Margin Expansion: With increasing capacity utilisation and a growing share of value-added products, Time Technoblast is seeing an improvement in its EBITDA margins. The company has consistently achieved quarter-on-quarter EBITDA margin improvement of 20 to 30 basis points.

Cost Reduction Initiatives: Time Technoblast is actively pursuing cost reduction measures through automation, re-engineering, and exploring alternative energy sources. For instance, the company expects to save around 12 crore rupees in power costs next year through its solar power initiatives. These efforts are expected to contribute to margin expansion.

i. 15% revenue growth in FY24-27

Revenue growing to Rs 7,500 cr by FY27 implies a revenue CAGR of 15%

Last year revenue we did around INR5,000 crores. So definitely, three years we would like to have. I can say the revenue around INR7,500 crores.

ii. Bottom lime to grow much faster than top-line FY24-27

EBITDA Margin expected to expand from 14.2% as Q1-25 to 15.5%+ by FY27

Value added sales is around 25%. In 3 years down the lines we are projecting it will be 35%

Current has achieved 14.2%. We can definitely achieve the 3 years down the line, maybe 15.5% from there or even above that.

8. PAT growth of 40% & Revenue of 14% in Q1-25 at a PE of 25

9. Hold?

If I hold the stock then one may continue holding on to TIMETECHNO

TIMETECHNO delivered a strong FY24 followed by an excellent H1-25 where bottom-line performance has been quite strong. Increased confidence in the management to deliver top-line growth of 15% with margin expansion that FY24 targets were achieved.

The business outlook for H2-25 is strong. Despite challenges like extended monsoon seasons, TIMETECHNO remains confident about achieving its projected growth of around 15% for the fiscal year.

Robust demand: The order book for CNG cascade stands strong at approximately ₹185 crores.

Favorable trends in key business segments: Both industrial packaging and composite cylinders are expected to perform well.

Declining oil prices: This translates to lower polymer prices, benefitting the company and accelerating the shift from metal to polymer and composite products.

Margin profile of TIMETECHNO expected to improve and drive faster PAT growth with increasing contribution of value added products and reduction in interest cost as it reduces its debt. We can stay in as long as the value addition story plays out.

Substantial EBITDA margin increase which is currently 14% to 16%

Goal of becoming debt-free in 2-3 years.

10. Buy?

If I am looking to enter TIMETECHNO then

For a PAT growth of 40% on a revenue growth of 14% in H1-25, the PE of 25 looks acceptable.

TIMETECHNO is guiding for 15% revenue growth in FY25 with PAT expected to grow faster than the revenue at a PE of 25 which makes the valuations acceptable in the short term.

TIMETECHNO is guiding for FY24-27 revenue CAGR of 15% with EBIDTA margins expanding from 14.1% to 15.5%+ at a PE of 25 which makes the valuations reasonable in the short term.

TIMETECHNO generated Rs 93.3 cr free cash flow in H1-25. It is quoting a market cap of Rs 8401 cr. It is available at free cash flow yield of 1.11% (not annualized) which makes the valuations acceptable. FY25 should also deliver free cash flow generation

If the thesis of increased contribution of value added product which will drive bottom line growth higher than the top line is not delivered then it may not sustain current valuations.

Previous coverage of TIMETECHNO

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer