TD Power Systems Q3 FY26 Results: PAT Up 25%, On-track FY26 Guidance

Guidance of 40% growth in FY26 followed by ~25% growth in FY27. Industry tailwinds, order inflows and exports drive growth. Expensive valuations demand strong execution

1. Motors & Generators Manufacturer

tdps.co.in | NSE: TDPOWERSYS

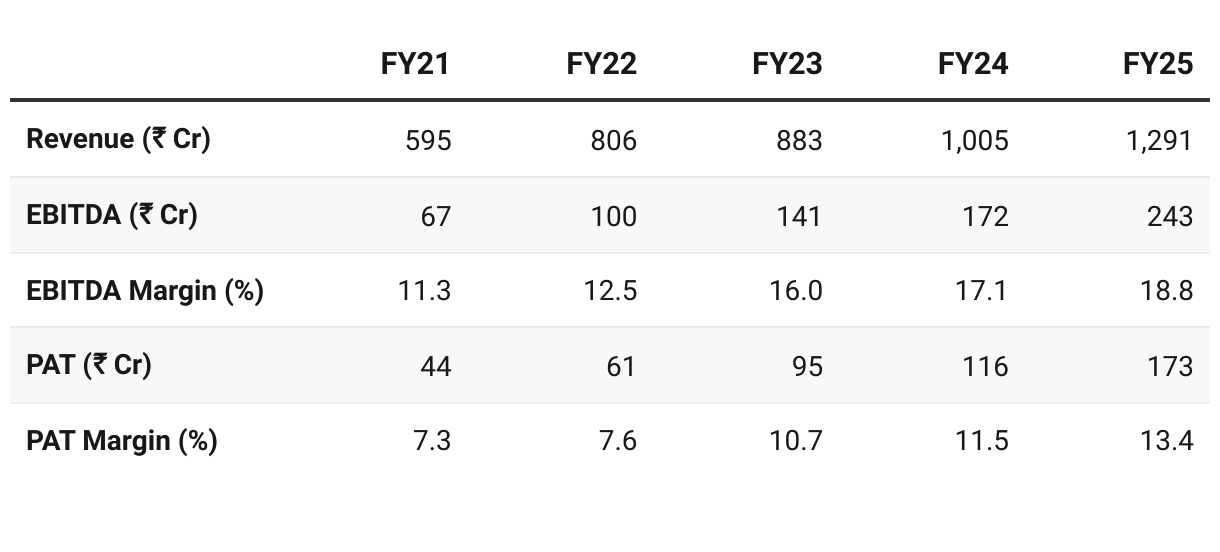

2. FY21-25: PAT CAGR 41% & Revenue CAGR 21%

Scale of Operations Doubled: Global market expansion, product diversification (motors, hydro, geothermal), and revival in domestic demand.

Margin Expansion: Increased export share, better product mix, leaner operations, and selective participation in higher-margin projects (e.g., data centers, geothermal, traction motors)

Exports Became the Growth Engine: Focus on clean energy, grid stabilization, and AI-linked infrastructure in export markets transformed the business

Product Portfolio Expansion: From Steam turbine generators to Gas & geothermal generators, Motors (synchronous, induction), Traction motors (NPCIL, export markets), Grid stabilization & data centers

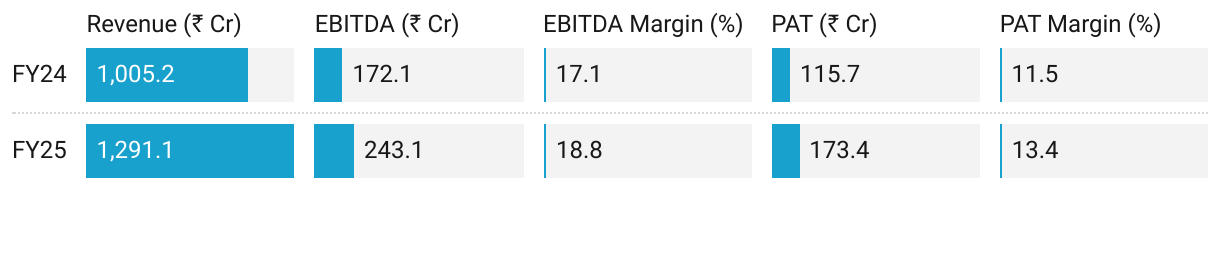

3. FY-25: PAT up 50% and Revenue up 28% YoY

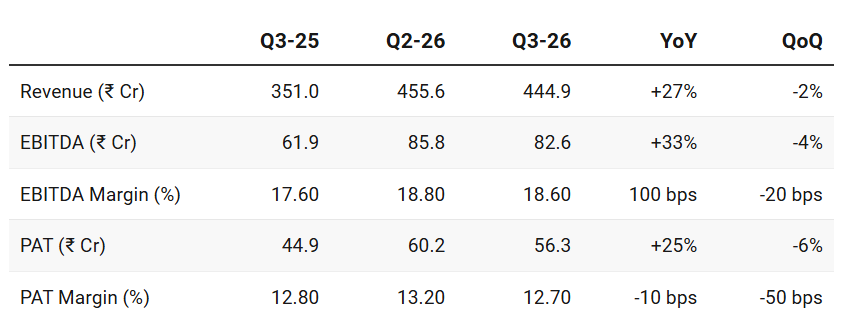

4. Q3-26: PAT up 25% and Revenue up 27% YoY

PAT down 6% and Revenue down 2% QoQ

Record Q3 Order Inflows & Order Book

All-Time Record Inflow: Q3 saw 61% year-on-year increase.

Export Dominance: Exports drove the Q3 performance, making up 84% of the quarterly order inflow. For the nine-month period, exports accounted for 79% of total order inflows.

Q3 Operational Developments

Third Plant Operationalized: The company declared its newly constructed third plant operational on December 18th. Because this occurred late in the quarter, the new capacity did not yet impact Q3 sales.

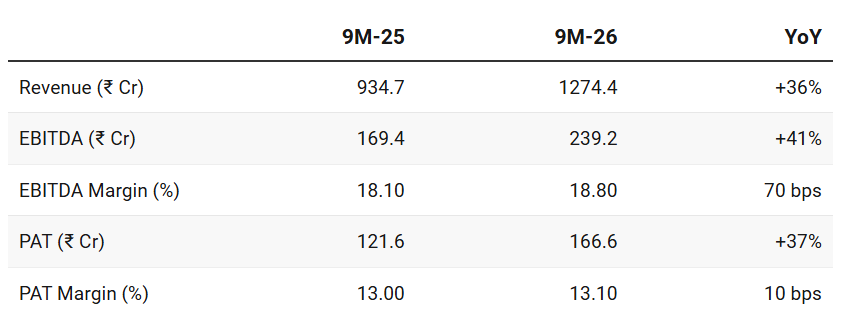

5. 9M-26: PAT up 37% and Revenue up 36% YoY

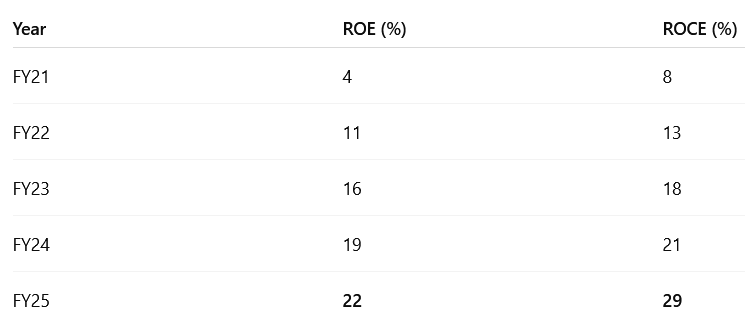

6. Business Metrics: Strong & improving return ratios

ROCE > ROE = Capital-Light Model — self-funded and not reliant on leverage to generate returns.

7. Outlook: Solid Growth Guidance till FY27

7.1 FY26 Guidance — TD Power Systems

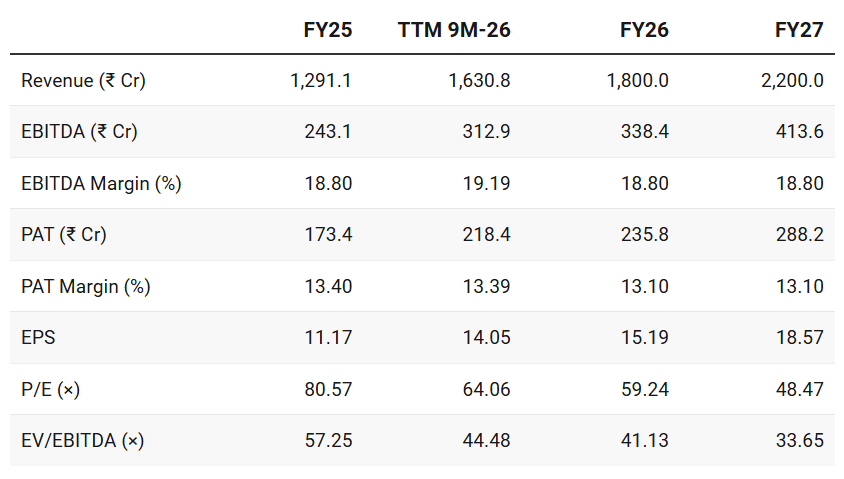

We maintain our top line guidance of 18 Billion INR for FY 26.

Additionally, we give a revised guidance for FY 27 at 22 Billion INR .

This is a conservative guidance based on the ramp-up of the order booking that we're seeing, which is around INR 575 crores to INR 600 crores per quarter, we see an extremely high probability to increase our guidance further.

The order inflow from exports continue to be the driver for growth .

The company has a diversified product range serving global markets for steam turbines, gas turbines, gas engine, geo-thermal, motor, and other special applications and wide range of global OEM’s ~45 spread over all business segments .

The key driver for growth is EXPORT — The order inflow clearly reflects the strength of the company’s business in International markets .

Export growth will continue to drive the company’s business in FY 27 & FY 28. With the third plant commissioned, the ramp up of the production and sales will be seen from Q4 FY 26 onwards .

To meet pipeline demands, production will ramp up to ₹550-575 Cr in Q4-26, and then move to around ₹600 Cr per quarter from Q1-27 onwards.

Segment Growth and Demand in Place till FY30:

Gas Engine and Gas Turbine Generators:

Strong visibility with firm forecasts from OEMs — showing a huge year-on-year increase up until 2030.

Driven largely by data centres moving to captive power to avoid grid dependency, as well as demand for grid stabilization and synchronous condensers.

Hydro:

FY27 projected to be the highest in the company’s history for hydro.

Strong visibility for at least the next two to three years — driven by a growing refurbishment market in India and abroad.

Steam Turbines (India): The domestic market is experiencing steady, moderate growth of around 10% to 12%, driven by captive power plants, biomass, waste heat recovery, and the steel industry.

Motors: Currently taking a backseat to the booming generator business, motors will grow at a steady 10-15% per year.

To become a major thrust area for the company from FY28 onwards.

Railways:

Expected to remain in a “steady state situation” for the next couple of years.

Existing Indian Railway contract is set to expire by FY28

TDPOWERSYS transitioning to exports — US, European, & Russian markets.

Capacity and Margins Outlook:

Capacity Expansion:

To maximize the utilization of its newly operational third plant and existing assets up to FY28

No capex until revenue reaches ₹2,600-2,800 Cr.

Will evaluate the need for further major capacity additions around Q4-27.

Profitability:

Gross margins are expected to sustain around 35%.

Bottom line will see significant benefits starting in Q4 and Q1 from the depreciation of the Indian rupee against the Euro and Dollar.

Stopped hedging its foreign exchange roughly six months ago to fully capture these depreciating spot rates.

Commodity cost increases (like copper) are being successfully passed on to customers through renegotiations.

7.2 9M FY26 Performance vs FY26 Guidance

Revenue — On-track ₹1,800 Cr guidance for FY26.

Asking rate of ₹525 Cr in Q4-26 vs ₹445 Cr delivered in Q3-26

Margins: Delivered 18.8% vs guided ~18% — execution ahead of plan.

Order Inflow: ₹1,572Cr (+48% YoY) — healthy momentum; 79% export-driven.

Order Book: ₹1,845.2 Cr — provides visibility till H1-27

Tariff Risks: US tariffs may impact 4–5% of sales, mitigated by Turkey plant; execution will be closely watched in H2.

8. Valuation Analysis

8.1 Valuation Snapshot

CMP ₹900; Mcap ₹14,110 Cr

P/E (64×): Very Expensive; justifiable — only if growth + margins sustain till FY30 based on the strong demand outlook

EV/EBITDA (45×): Market pricing in durable growth; comparable to high-quality capital goods leaders.

PEG: ~2→ expensive,

Rerating beyond FY27 depends on export demand, guidance upgrades, and smooth tariff mitigation.

Premium growth story — long-term opportunity — near-term valuation comfort is limited.

8.2 Opportunity at Current Valuation

Opportunities are limited

The price has run far ahead of its fundamentals.

The demand environment is strong and presents a lot of opportunities for the business but at current valuations:

No opportunity for fresh buying in the stock unless there is some market correction without changes in the business outlook

Opportunity to continue and ride the momentum as long as it lasts for those who already have a position in the stock

The next window of opportunity may open up when the management gives a guidance which is firmer than the minimum 20% growth in FY28

However growth will be constrained by the max revenue potential from the planned capacity expansion

Guidance Upgrade Likely: Guidance upgrade expected in FY27— not baked into the valuations

Even if ₹600 Cr per quarter from Q1-27 onwards is delivered — FY27 Revenue of ₹2,400 Cr implies P/E 44× and EV/EBITDA 31× which is not cheap either.

8.3 Risk at Current Valuation

FY27 Already Discounted — No room for disappointment

At FY27E P/E 49× and EV/EBITDA 34×, the strong demand environment, capacity expansion and all the optionality from the large generator product is all discounted.

Little room for disappointment in terms of business execution.

Tariffs:

Uncertainty around US tariff hikes add execution complexity.

Yet no let-up or hesitation in order inflows.

Customers are actively absorbing the tariffs, and none are insisting that TD Power Systems shift its production to Turkey to mitigate “risk perception” or reduce lead times.

Commodity Price Volatility:

Cost pressures from drastically rising commodity prices, specifically copper.

Utilizing a previously booked pipeline of lower-priced copper inventory to insulate near-term margins.

For future orders — renegotiating contracts to pass all increased costs on to customers.

Sector Concentration Risk:

Surge in demand driven by data centers — potential risk of over-reliance on this single sector.

Management dismissed concerns that a slowdown in U.S. AI investments would impact their order book, noting that tech companies are actually increasing their AI expenditures.

Previous Coverage of TDPOWERSYS

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer