Talbros Automotive Components: PAT growth of 98% & Revenue growth of 20% in FY24 at a PE of 17

Roadmap for 20%+ revenue CAGR for FY24-27 set for TALBROAUTO. FY25 guidance with 15%+ revenue growth. Roadmap to deliver EBITDA margin of 15-16% & ROCE of 20%+ by FY27 with reasonable debt

1. Auto Component manufacturer

talbros.com | NSE : TALBROAUTO

~50% Market share in Gaskets: 3x the nearest competitor Market Leader in — Two-Wheeler, Agri & Off Loaders, HCV & LCV segment

2. FY20-24: PAT CAGR of 73% & Revenue CAGR of 19%

3. Strong FY23: PAT up 24% and Revenue up 12% YoY

Expansion of PAT margin to 8.5% in FY23 from 7.7% in FY22

4. Strong 9M-24: PAT up 56% & Revenue up 22% YoY

5. Strong Q4-24: PAT up 35% & Revenue up 15%

6. Strong FY24: PAT up 98% & Revenue up 20%

Profit After Tax (Before Exceptional ltems) is up 49%

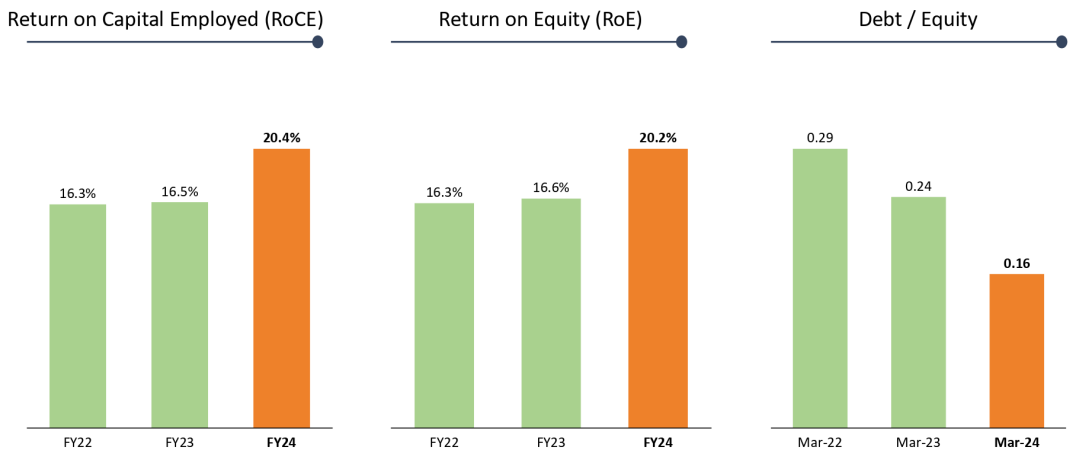

7. Business metrics: Strong & improving return ratios

8. Outlook: FY24-27 Revenue CAGR of 20%+

i. FY24-27: Revenue CAGR of 20%+

Talbros group including JV expected to grow to Rs 2200 cr of which TALBROAUTO would be Rs 1400-1500 cr. This implies a growth of TALBROAUTO from Rs 791 cr in FY24 at CAGR of 21-24%

FY27: So Talbros will be around INR1400 crores - INR1500 crores out of that.

Gasket: Plan to grow revenues by 13% CAGR till FY27 to Rs. 700 crores

Forgings: Plan to grow revenues by 23% CAGR till FY27 to Rs. 500 crores

ii. FY25: 15%+ revenue growth

Yes, plus we are hopeful that next year also at present we can see a growth of minimum 15% plus.

iii. Talbros 2.0: Margin expansion, improved ROCE & reasonable debt

9. PAT growth of 98% & Revenue growth of 20% in FY24 at a PE of 17

10. So Wait and Watch

If I hold the stock then one may continue holding on to TALBROAUTO

Coverage of TALBROAUTO was initiated after Q1-24 results. The investment thesis has not changed after a strong FY24. The delivery of a strong FY27 has increased confidence in the management to deliver on its roadmap for Talbros 2.0

Management is on track to deliver as per the roadmap to Rs 2,200 cr by FY27

We are assure of achieving our group sales target of INR2,200 crores by FY '27, of which 35% export -- will be from export. This will come from the U.S., the U.K., Europe as well as Japan.

Revenue outlook is supported by the order book.

11. Or, join the ride

If I am looking to enter TALBROAUTO then

TALBROAUTO has delivered a PAT growth of 98% and Revenue growth of 20% in FY24. TALBROAUTO at a PE of 23 makes valuations quite fair in the short term.

In the medium term, 15% revenue growth for FY25 is a slow down compared to FY24. Yet, at a PE of 17 makes valuations quite acceptable in the medium term

The long term outlook for 20%+ revenue CAGR for FY24-27 creates opportunity in the stock at a PE of 17 makes valuations quite attractive.

Previous coverage of TALBROAUTO

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer