Sugs Lloyd FY26 Results: PAT up 72%, Strong FY27 Guidance

Guiding 100% revenue growth in FY27. FY26-28 revenue CAGR of 80%. Trading at cheap valuations. Issue is not valuations but the quality of growth for Sugs Lloyd

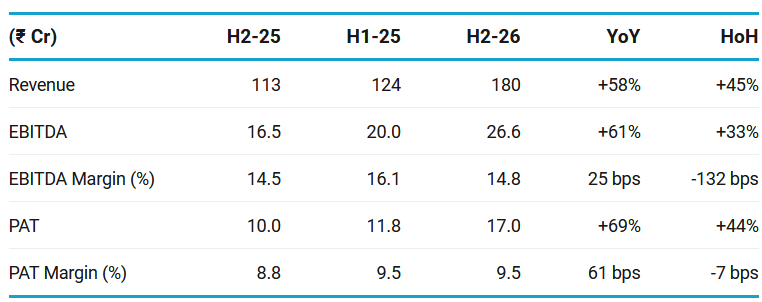

H2 revenue was strong, but H2 core EBITDA margin was softer than H1. Management attributed Q4 margin pressure partly to a shifted MAHAGENCO project and extra costs due to local/land-related issues.

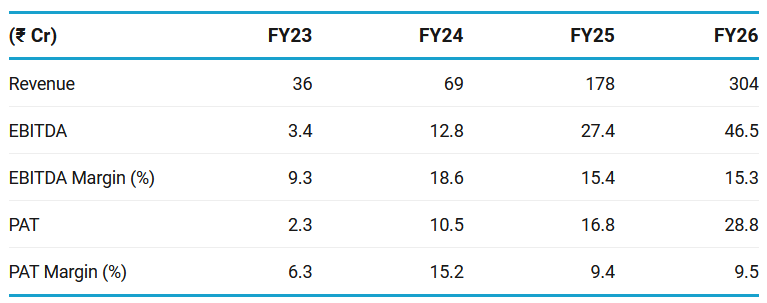

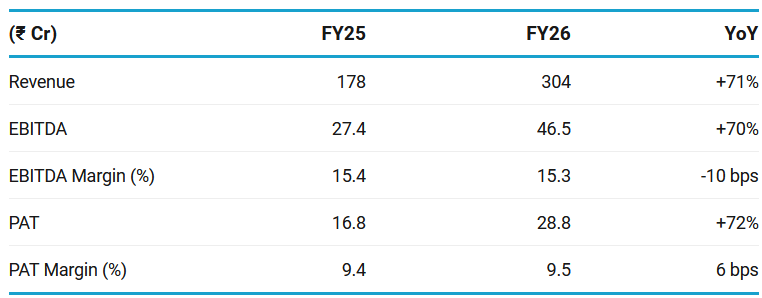

4. FY26: PAT up 20% & Revenue up 27% YoY

We have overachieved our guidance for financial year ‘26, delivering a turnover of INR300 crores against our stated guidance of INR270 crores

FY26 guidance was exceeded, and order book improved sharply. But the quality of growth is not yet clean because receivables doubled, operating cash flow remained negative, and cash balance stayed negligible.

FY26 was back-ended. This matches management’s comment that Q4/H2 is typically stronger. But it also explains why receivables spike at year-end.

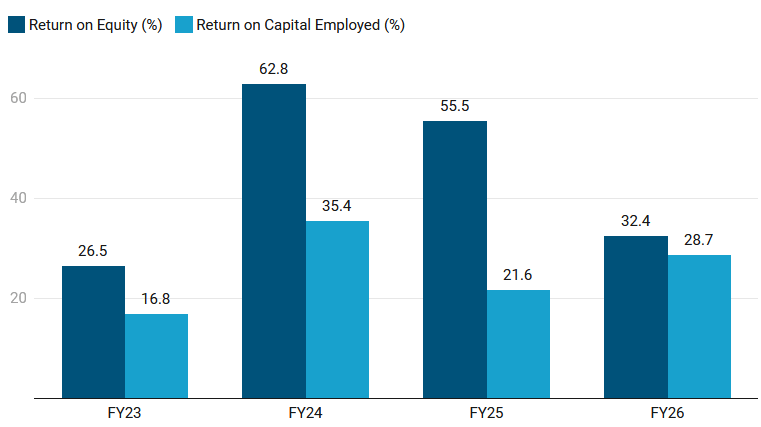

5. Business Metrics: Stable Return Ratios

FY26 ROE fell compared with FY25 because IPO equity increased the equity base.

On an increased capital base FY26 ROCE remained strong at ~29% — business generates attractive operating returns on capital.

The caution is that FY26 operating cash flow was negative.

So even though ROE and ROCE look good, the quality of these returns depends on whether receivables convert into cash.

For FY27, the key monitorable is not only ROE/ROCE. It is whether high ROCE converts into positive operating cash flow.

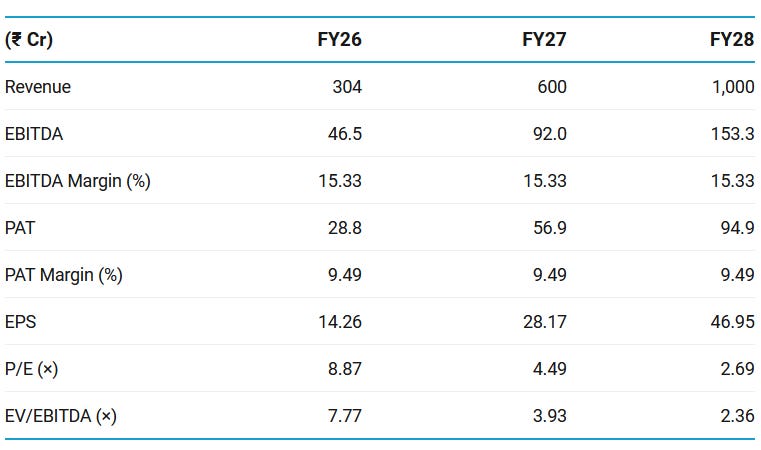

6. Outlook: Growing at 70%+ CAGR

6.1 FY27 Guidance

FY27 Guidance

FY27 Margins: As I said during my introductory call, we have been growing almost like an 1.7, 1.8x over the last year and we will maintain the momentum. And we have been able to retain both the EBITDA margin as well as the PAT margin. We are very confident that we will be able to maintain at least the trend over the next year and more.

Order book:

Our order book as of now stands around INR825 crores

Oder-book Pipeline:

Total tenders which are at various stages of evaluation is around INR1,225 crores — around 200 to 300 out of these we are going to book

FY28: Our target of INR1,000 crores revenue by financial year ‘28 is firmly on track.

7. Valuation Analysis — Sugs Lloyd

7.1 Valuation Snapshot

Current Market Price — ₹126.45

Market cap — ₹ 293.54Cr

Sugs Lloyd looks optically very cheap on FY27/FY28 earnings if management hits the ₹600 Cr / ₹1,000 Cr revenue path.

The company is not being valued like a high-growth infra-compounder. It is being valued like a risky SME EPC name. The market is probably discounting four things:

Forward valuation becomes very cheap if FY27/FY28 guidance is met

If Sugs delivers FY27 numbers, the market may not allow it to trade at 5x earnings for long. Even an 8–10x FY27 P/E gives meaningful upside.

Order book supports the growth case

This is the biggest reason the valuation is interesting.

Management said the current order book is heavily Power T&D-led, with Power T&D expected to be the largest contributor going forward.

The order book is not only large; it is moving toward Power T&D / smart grid / ADMS / SCADA-type projects, which can get better market valuation than plain solar EPC if execution is good.

Business mix shift can drive re-rating

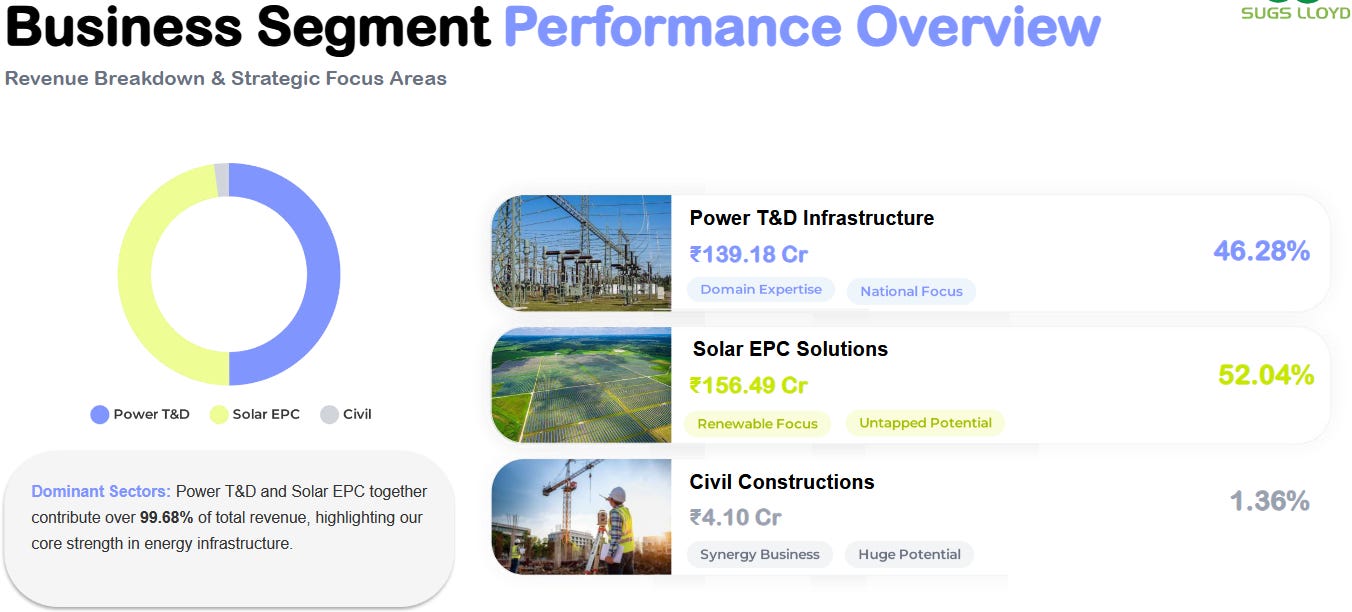

FY26 revenue was still solar-heavy:

But the order book is now ~86% Power T&D. That is a major mix shift.

If the market starts viewing Sugs Lloyd as a Power T&D / grid automation / RDSS execution company instead of just a small EPC contractor, the multiple

What is already priced in?

Priced in: Growth risk, SME liquidity risk, receivable risk, EPC risk, and cash-flow weakness.

Not fully priced in: FY27 ₹600 Cr revenue delivery, order-book conversion, Power T&D re-rating, positive CFO.

Opportunity is not just earnings growth. It is earnings growth + multiple re-rating.

8.3 Risks at Current Valuation

Operating cash flow was negative — That is the key problem.

The cash-flow statement shows working-capital absorption was heavy, mainly due to the sharp increase in receivables and other assets.

Receivables risk — profits stuck in balance sheet

Trade receivables increased from ₹70.56 Cr to ₹159.25 Cr. That is more than 50% of FY26 revenue. Other current assets also rose to ₹42.76 Cr, and other non-current assets stood at ₹50.28 Cr.

Cheap earnings can become a value trap if receivables keep rising.

FY27 execution risk — valuation depends on a steep ramp

Sugs Lloyd has to roughly double revenue in FY27, then grow another ~67% in FY28.

This is a very steep ramp for a working-capital-heavy company

Order-book conversion risk

FY27 revenue needs both execution of existing orders and fresh order inflows.

Any execution delay, site issue, working-capital bottleneck, or billing delay can hurt FY27 numbers.

Large-order concentration risk

A major part of the order-book jump came from the large ~₹640 Cr order

They expect ₹200–250 Cr billing from this order in FY27, with balance moving to FY28.

If this large order slows down, FY27 growth can disappoint. Large orders improve visibility, but they also increase concentration and execution dependence.

Business-mix risk — Power T&D shift is not yet proven in revenue

FY26 revenue was still slightly solar-heavy:

The order book has shifted to Power T&D, but FY26 revenue did not yet show that shift.

The market may wait for FY27 numbers before valuing Sugs Lloyd as a Power T&D / smart-grid company. Until then, it may continue to get an EPC discount.

Government/DISCOM exposure risk

Management says they prefer projects funded by Government of India or multilateral agencies, which reduces payment risk. But billing still often flows through government entities/DISCOMs.

Even if ultimate funding is secure, project approvals, billing certification, retention release, and collection timelines can stretch. This is exactly why receivables matter.

SME listing and liquidity risk

Sugs Lloyd is listed on the SME platform — listed on September 5, 2025.

SME stocks can have lower liquidity, wider spreads, higher volatility, and sharper drawdowns.

Entry may be easy; exit during bad news may not be.

The main risk is not overvaluation. The main risk is quality of growth.