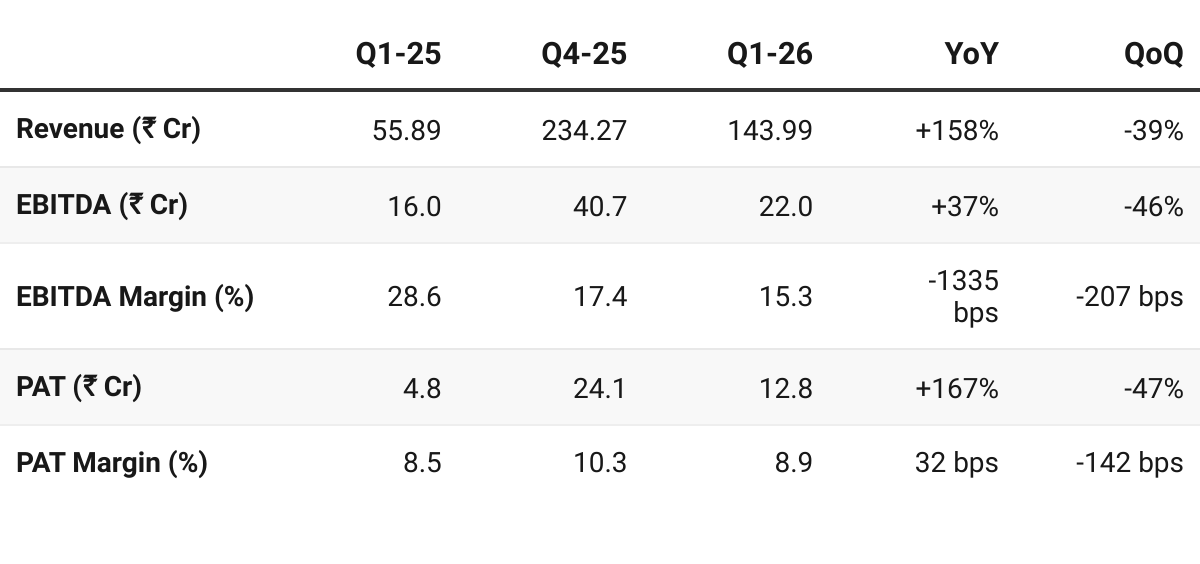

SRM Contractors Q1 FY26 Results: PAT up 167%, On-track FY26 Guidance

Guidance of 66% revenue growth in FY26 with stable margins, steady order-inflows and strong revenue visibility. At reasonable valuations based on FY26 guidance.

1. Engineering Procurement Construction Company

srmcpl.com | NSE: SRM

Operates in high-margin, high-entry-barrier hilly terrain EPC niche.

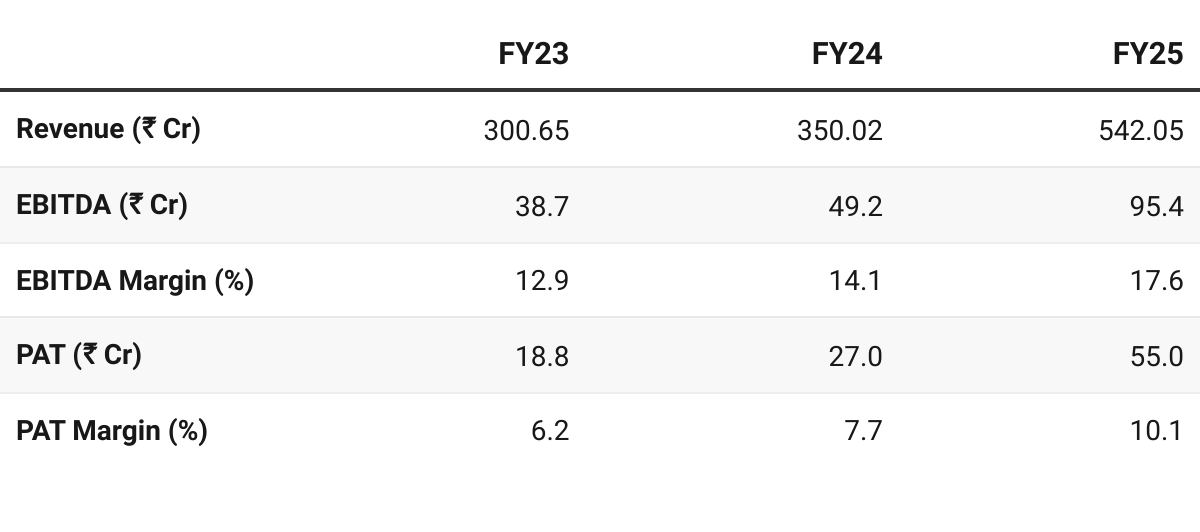

2. FY23–25: PAT CAGR of 71% & Revenue CAGR of 34%

3. FY25: PAT up 104% & Revenue up 55% YoY

Growth driven by road, bridge, and slope stabilization projects in J&K, Uttarakhand, and Gujarat.

J&K (41%), Uttarakhand (20%), Gujarat (18%), Ladakh (10%), Himachal (7%), Odisha (4%).

Margin improvement came from clustering of projects, equipment ownership, and backward integration.

Focus on clustering projects in J&K, Ladakh, Himachal, Uttarakhand to optimize logistics and margins.

IPO in FY25

Forayed into hydropower & aerial ropeways (planned vertical diversification).

4. Q1 FY26: PAT up 167%, Revenue up 158% YoY

PAT down 47% & Revenue down 39% QoQ

Strategic acquisition of 51% stake in Maccaferri Infrastructure Pvt. Ltd.

Expertise in geotechnical and environmental solutions, including slope stabilization, soil retention, and erosion control.

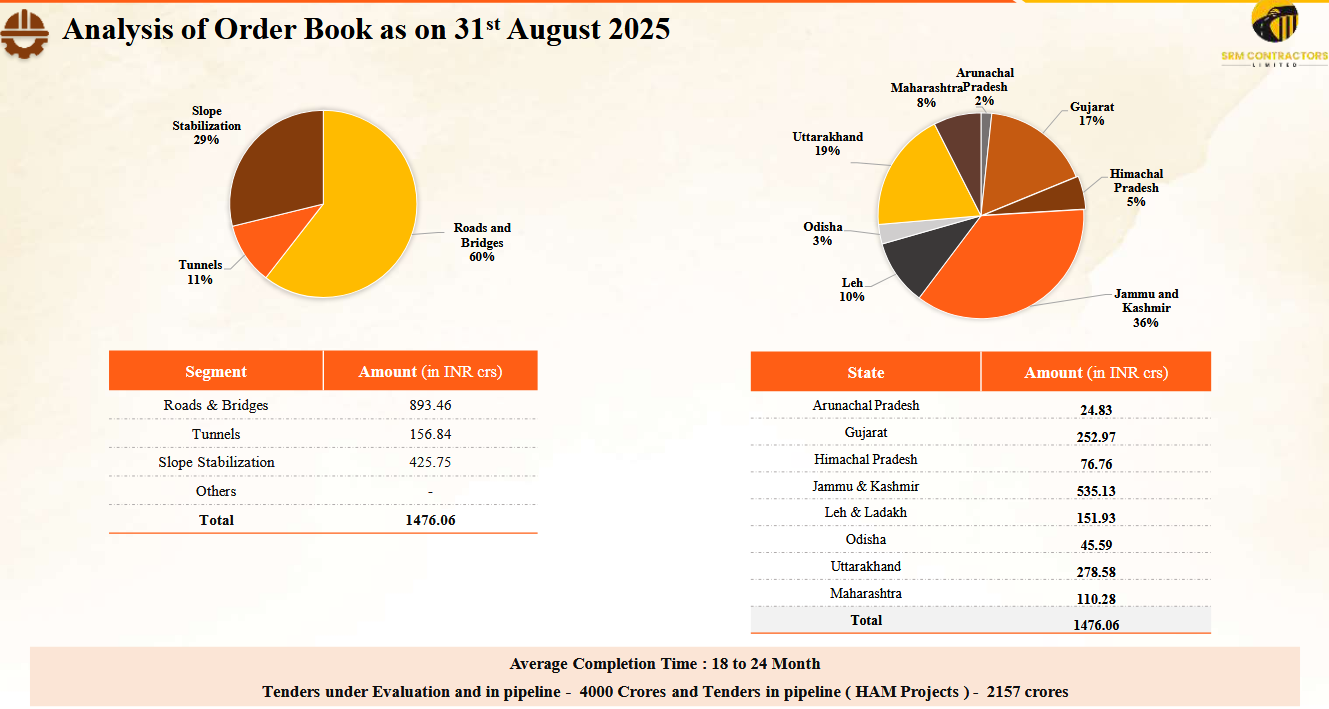

Order book of ₹211 crores, — consolidation in the upcoming quarter

Order book (31-Aug-2025): ₹1,476.06 Cr = 1.64 × FY26E revenue

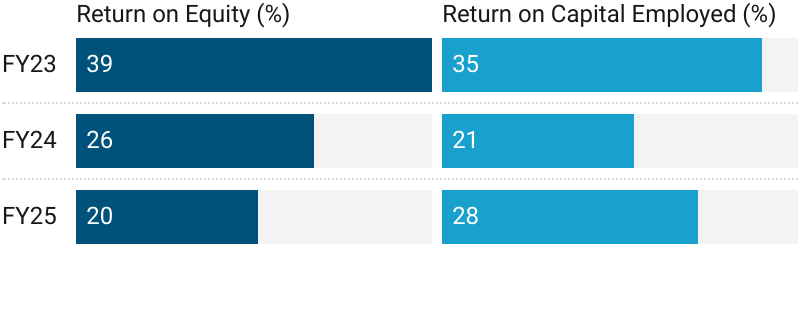

5. Business Metrics: Strong & Improving Returns

ROE muted by IPO funds in FY24 — yet to recover to FY23 levels

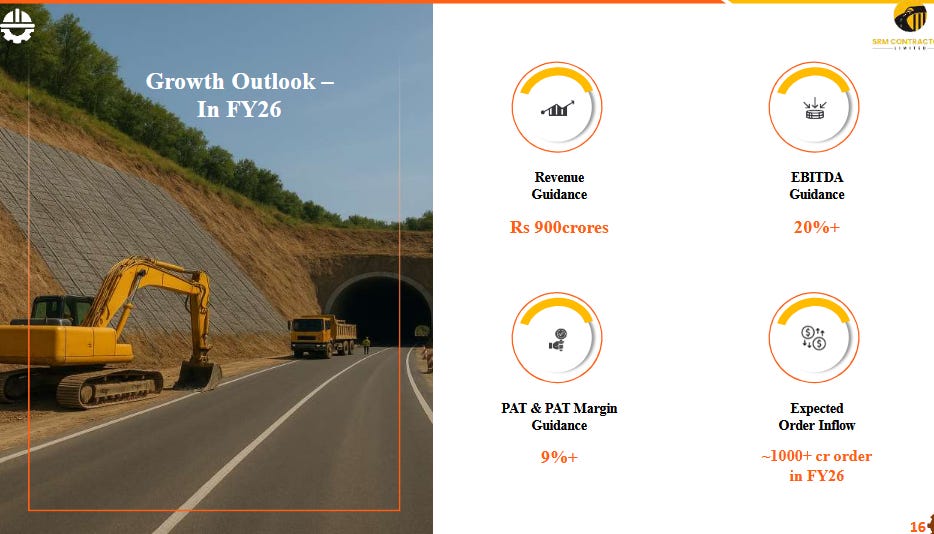

6. Outlook: 66% Revenue Growth in FY26

6.1 Guidance

Guidance for FY26 given post Q1-26 results

Outlook for FY27

Based on the order book math:

FY26(E) closing order book = Opening OB (₹1,460.6 Cr) + Expected inflow (~₹1,000 Cr) – FY26 revenue (₹900 Cr)

Implied closing OB FY26 = ~₹1,560 Cr

With an average execution cycle of 18–24 months, this points to a potential FY27 revenue run-rate of around ₹1,000 Cr.

One needs to keep a watch on early indicators for FY27 order-book as it will decide FY27 revenue outlook. This order-book calculation does not take into account the impact of the acquisition

6.2 Q1 FY26 vs FY26 Guidance — SRM Contractors

On-track FY26 guidance on revenue growth

Topline:

To reach ₹900 cr, execution must step up to ~₹250 cr/quarter in Q2–Q4 vs ₹144 cr in Q1.

Q1-25 contributed 10% of FY25. Q1-26 at 16% of FY26 guidance appears to be an improvement over FY25.

The ₹1,476 cr order book and a healthy pipeline support that ramp.

Margins:

PAT margin of 8.9% is tracking guidance given the seasonally weak Q1, but EBITDA 15% needs accretion through operating leverage, clustering, and claim/cost discipline. Q1 EBITDA = ₹22 cr vs ≥₹180 cr implied for the year.

Inorganic growth: Consolidation of Maccaferri Infrastructure (MIPL) with ~₹211 cr order book is flagged to kick in from upcoming quarters—this can aid both topline and mix.

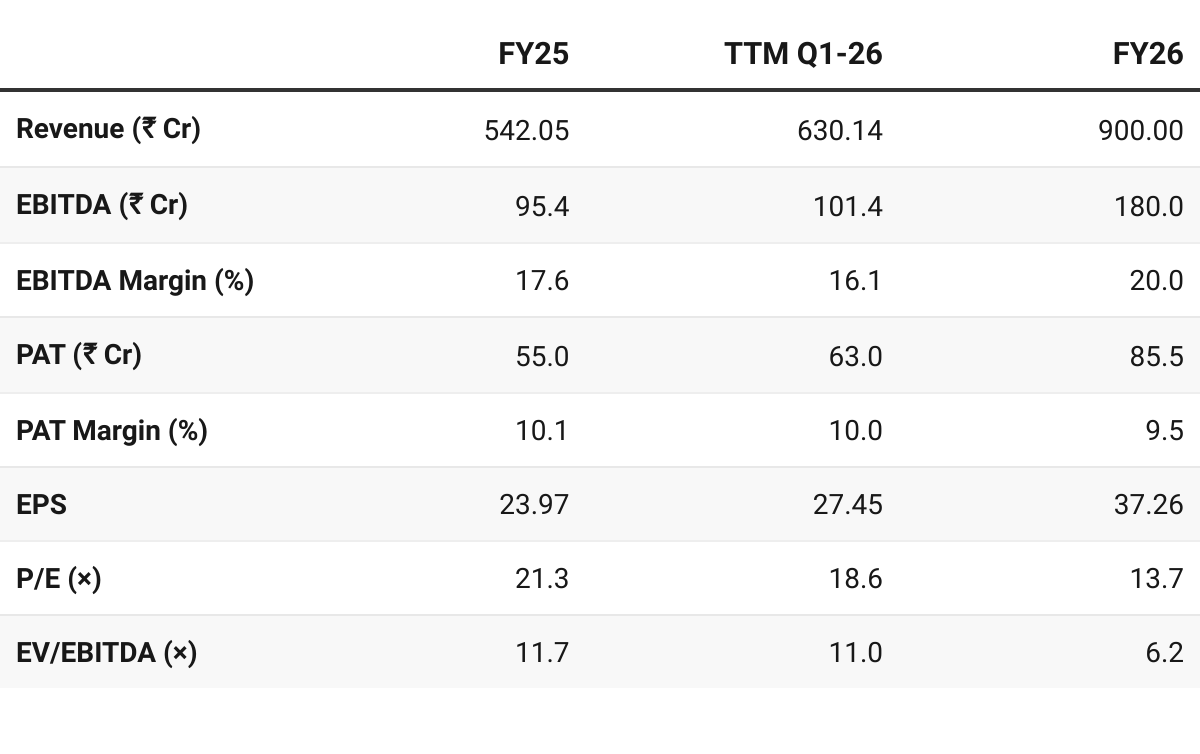

7. Valuation Analysis

7.1 Valuation Snapshot — SRM Contractors

CMP ₹510; Mcap ₹1,167.8 Cr;

Attractive Forward Valuation:

On FY26(E), SRM looks reasonably valued to attractive: EV/EBITDA ~6.2×, P/E ~13.7×, EV/Sales ~1.24× with net cash.

If ~₹900 Cr revenue and ~₹90 Cr PAT materialize, stock could see re-rating back to high-teens

7.2 Opportunity at Current Valuation

Sector Tailwinds: Government’s thrust on border connectivity, tunnels, highways, and hill-road infra aligns with SRM’s niche expertise; execution in high-entry-barrier terrains creates sustainable edge.

Margin Leverage: FY25 PAT margin reached 10.2%; management guides for 9%+ PAT in FY26. There could be an upside if FY25 margins of 10% are maintained in FY26.

Inorganic Growth (Maccaferri acquisition): 51% stake adds ~₹211 Cr order book, advanced geotechnical/soil stabilization capabilities, and nationwide client base—broadening SRM’s portfolio and margins.

Continuation of growth into FY27: If the historic growth momentum of FY23-25 continues into FY27, significant opportunity would emerge based on FY27(E) valuations. Even, at a ~20% growth into FY27, the forward valuations move to a PE closer to 10 which make it attractive.

7.3 Risk at Current Valuation

Execution & Seasonality: Operations in high-altitude terrains face weather disruptions, short working seasons, and risk of cost/time overruns.

Geographic Concentration: ~36–41% of order book is still in J&K; high exposure to a single geography raises dependency risk.

Working Capital Pressure: FY25 CFO was muted despite PAT doubling, as inventories and receivables expanded. WC intensity could stretch cash flows during scale-up.

Order Book Traction: OB declined from ₹1,668 Cr (Sep-24) → ₹1,461 Cr (Mar-25), only modest recovery to ₹1,476 Cr (Aug-25). Sustained inflows are crucial to support FY26 revenue target of ₹900 Cr.

Government Dependence: Heavy reliance on NHAI, NHIDCL, BRO, and state bodies exposes SRM to policy changes, budget allocations, and payment delays.

HAM Exposure Ahead: Planned diversification into HAM projects (~₹2,157 Cr in pipeline) adds equity-funding and lifecycle risks beyond EPC.

Integration Risk: Smooth consolidation of Maccaferri Infrastructure (MIPL) will be essential; integration challenges or margin dilution could offset expected synergies.

Valuation Execution Risk: Current multiples (P/E ~18.6× TTM, EV/EBITDA ~11×) already price in growth. Any shortfall in FY26 delivery (₹900 Cr revenue / 20% EBITDA) could pressure stock performance.

Help your group stay ahead. Share now!

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer