Shriram Pistons & Rings: PAT up 68% & revenue up 15% in H1-24 with strong cashflow available at PE of 11

SHRIPISTON is a free cash flow compounder available at attractive PE and free cashflow yields on the back of a strong H1-24, delivering QoQ growth in H1-24.

1. Manufacturer of automotive components

shrirampistons.com | NSE : SHRIPISTON

Shriram Pistons & Rings Ltd (SPRL) is the largest manufacturer of Pistons, Pins, Rings, and Engine Valves in India with a manufacturing unit in Ghaziabad and Rajasthan . Its products are marketed to almost all OEMs and Aftermarkets under the brands SPR and USHA.

SPR is the largest exporter of Pistons and Rings from India to marquee customers, including Perkins, Fiat Power Train, Cummins, Yanmar, BMW, Daimler, BRP Rotax, Kubota, Wabco, Cummins, etc.

Working to grow business model beyond IC engines

Acquisition of 51% shares in EMF Innovations Private Limited, a electric motor design & manufacturing company

The Company aims to expand its presence in Electric Vehicle space to supply Electric Powertrain Components such as Motor & Controller covering all the vehicle segments from Two Wheelers, Three Wheelers, Passenger Vehicles, Commercial Vehicles and Buses.

Acquisition of 62% shares in Takahata Precision India Private Limited, a precision injection moulded components manufacturing company

2. Strong Growth from FY21-23

82% PAT CAGR & 28% Revenue CAGR from FY21

Became a Rs 2000+ cr company in FY22

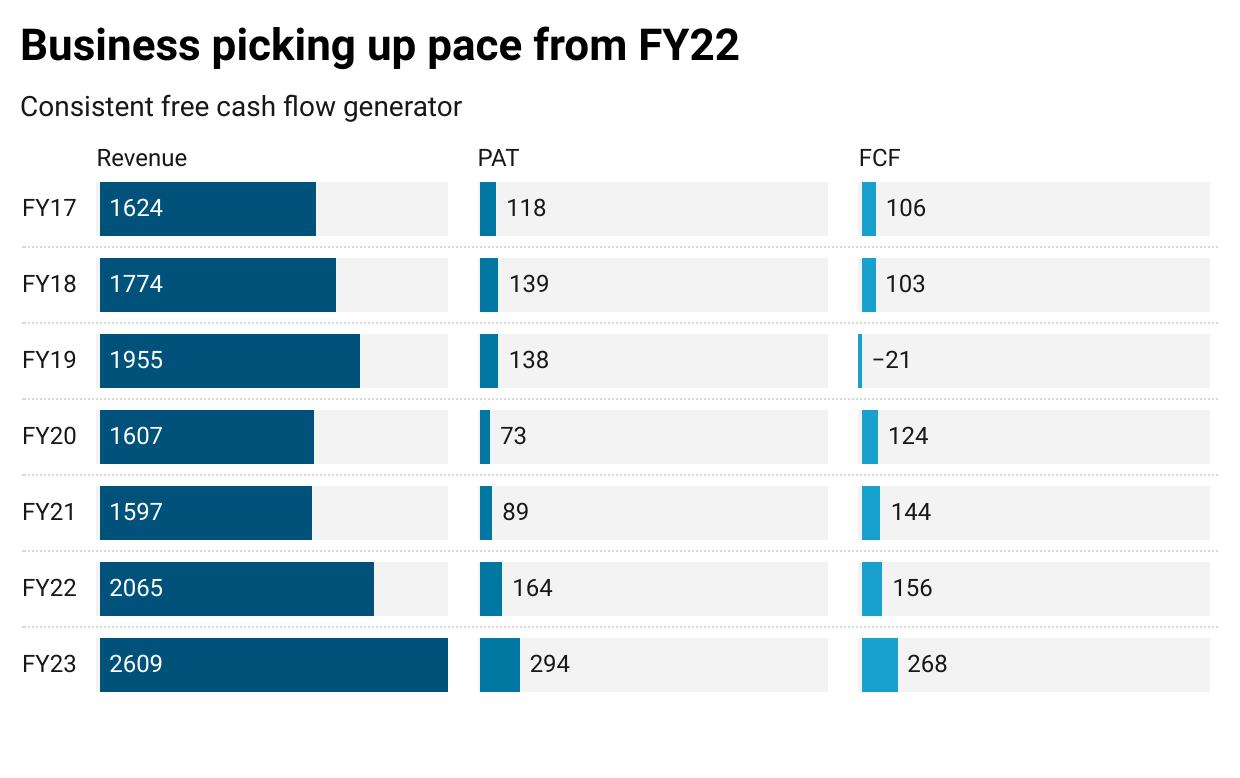

Unexciting yet solid growth from FY17-23

Revenue CAGR = 8%

PAT CAGR = 16%

Free Cashflow (FCF) = 17%

3. A strong FY23: PAT up 80% and Revenue up 26% YoY

Company’s revenue from operations grew by 26% from Rs. 20,647 Million (previous year) to Rs. 26,050 Million (during the year)

Company’s exports registered growth of almost 21% from Rs. 4,010 Million to Rs. 4,841 Million. This was due to strengthening of relationship with the existing customers, range expansion and entering new markets & product segments.

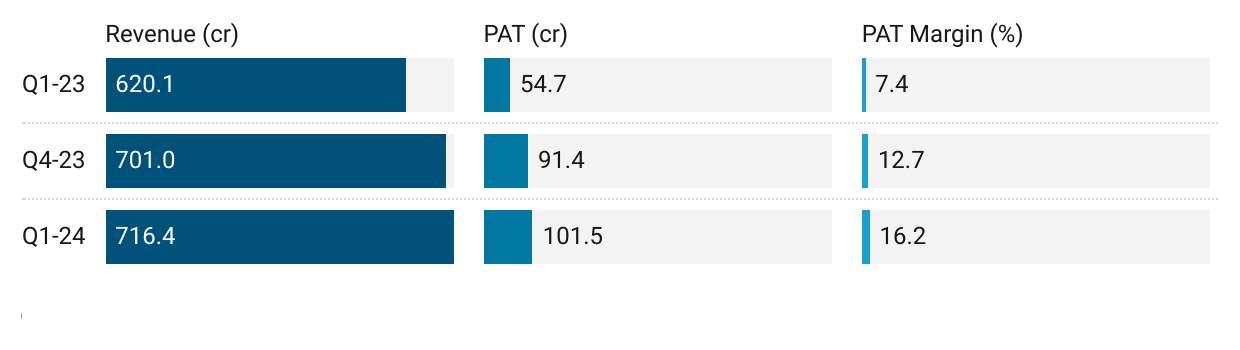

4. Momentum carries on in Q1-24: PAT up 86% & Revenue up 16% YoY

PAT up 11% & Revenue up 2% QoQ

Improvement in margin both YoY and QoQ

4. Strong Q2-24: PAT up 55% & Revenue up 15% YoY

PAT up 11% & Revenue up 5% QoQ

Improvement in margin both YoY and QoQ

5. Strong H1-24: PAT up 68% & Revenue up 15% YoY

Improvement in margin YoY and compared to FY23

6. Business metrics are strong and consistent

The business has delivered returns consistently. Cash conversion has been strong.

Metrics are at an all time peak in FY23

7. Outlook: 45% PAT & 15% revenue growth in FY24

In the absence of any management commentary or public information on the SHRIPISTON, one is relying on H1-24 repeating itself for FY24.

Revenue growth = 15%, PAT Margin = 14.2% (same as H1-24)

FY24 PAT = 2609.33*(1+15%)*14.2% = 427 cr

FY24 PAT growth = 45% over FY23

8. 45% PAT growth in FY24 at a PE of 11

9. So Wait and Watch

If I hold the stock then one may continue holding on to SHRIPISTON.

Coverage of SHRIPISTON was initiated after Q1-24 results. The investment thesis has not changed after a strong H1-24. The only changes are the delivery of a strong H1-24 and the increased confidence in the management to deliver a stronger FY24

If I hold the stock then one may continue holding on to SHRIPISTON only if one is satisfied by a slow and steady compounder.

Its not easy to find a company at a PE of 11 which is compounding free cash flow at long term CAGR of 17%.

It may not be suited for those looking for excitement in a stock.

Keep a watch on the impact of increased penetration of EV in 2W segment

In the coming years, the Company is expected to face challenges due to the increased penetration of electric vehicles in two wheeler segment. The management is working to overcome these headwinds in the coming year and are also working diligently to find further avenues of growth for the Company.

10. Or, join the ride

If I am looking to enter the stock then

SHRIPISTON has a a long term track record of growing PAT at a 16% CAGR and free cash flow at a CAGR of 17%. Against this track record it is available at a PE of 11 which makes the valuations quite attractive.

Outlook for 45% PAT growth in FY24 on the back of a strong H1-24 at a PE of 11 makes the valuations quite attractive.

SHRIPISTON is a consistent free cash flow generator.

It generated FCF of Rs 268 cr in FY23 and is available at market cap of Rs 4,687. This makes the free cash flow yield of 5.7% which makes the valuations look very attractive.

It generated FCF of Rs 194 cr in H1-24. This makes the free cash flow yield of 8.3% (annualized) which makes the valuations look very attractive.

The lack of any management commentary or public information is the biggest problem one faces in taking a call on SHRIPISTON.

Previous coverage of SHRIPISTON

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades