Shilchar Technologies: PAT up 149% & Revenue up 57% YoY in 9M-24 at a PE of 37

Solid execution in 9M-24 by Shilchar. Industry tailwinds. Strong demand outlook reflected in strong order book. Order book is sufficient for H1-25. Capacity expansion by 88% in FY25 to support growth.

1. Transformer Manufacturer

shilchar.com | BOM: 531201

Shilchar Technologies Ltd. a manufacturers of Electronics & Telecom and Power & Distribution transformers.

The Company has concentrated on catering needs of renewable energy sector including solar and wind energy in local market where in the Company has been enjoying commendable position being one of the top companies in India supplying transformers for renewable energy.

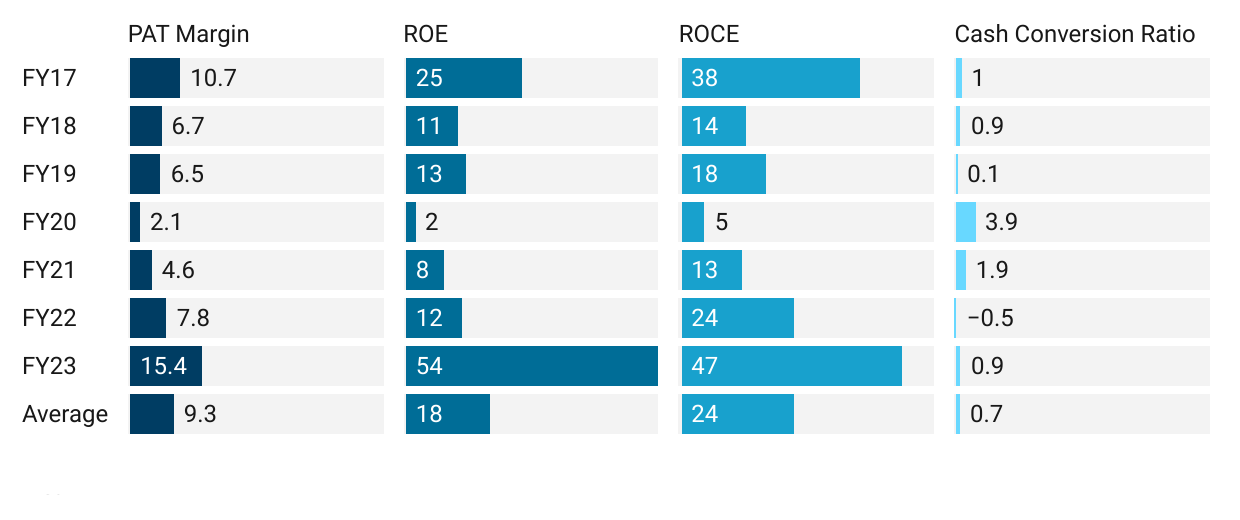

2. FY20-23: Delivering growth and profitability

3. FY23: PAT up 207% and Revenue up 56% YoY

Operational income of Rs. 280 cr compared to Rs. 180 cr for the previous year. Profit after tax is Rs. 43 cr as compared to previous year figure of Rs. 1.9 cr.

4. Strong H1-24: PAT up 173% & Revenue up 48% YoY

Margin expansion is explained by the management on account of export orders, and may be unsustainable and needs to be watched out for. 24% PAT margin for a transformer manufacturer looks too good to be true for long.

5. Strong Q3-24: PAT up 119% & Revenue up 72% YoY

6. Strong 9M-24: PAT up 149% & Revenue up 57% YoY

7. Business metrics recovering strongly after FY20

8. Outlook: Order book in place to support H1-25 revenue

i. Strong revenue visibility: Order book is sufficient for H1-25

With Rs 300 cr revenue in 9M-24, one could expect FY24 revenue to be Rs 400+ cr. The order book of Rs 355 cr should be sufficient for H1-25.

Total order booking as on 1st January 2024 is INR 355 crores.

ii. Capacity expansion by 88% in FY25

The full impact of the capacity expansion will be felt in FY26. FY24 will see a partial impact of the capacity expansion

Manufacturing for phase 1 expansion to start from 1st April 2024

Capacity to increase from 4000 MVA p.a. to 5500 MVA p.a.

Manufacturing for phase 2 expansion to start from 1st July 2024

Capacity to increase from 5500 MVA p.a. to 7500 MVA p.a

9. PAT growth of 149% & Revenue growth of 57% in 9M-24 at a PE of 37

10. So Wait and Watch

If I hold the stock then one can definitely hold on to Shilchar

Coverage of Shilchar was initiated after Q1-24 results. The investment thesis has not changed after a strong Q3-24. The delivery of a strong 9M-24 and the increased confidence in the management to deliver a stronger FY24 and continue the trend of YoY growth since FY20

One can stay the course with Shilchar as it keeps delivering strong quarterly results and the growth planned thru the capex kicks in.

One needs to keep a watch on the planned capacity getting executed and not getting delayed.

11. Or, join the ride

If I am looking to Shilchar then

Shilchar has delivered PAT growth of 149% & Revenue growth of 57% in 9M-24 at a PE of 37 which makes the valuations acceptable.

The outlook for 88% capacity expansion provides headroom for growth and provides a justification for the PE of 37.

If the momentum continues as delivered in the past, there is significant opportunity in Shilchar however the margin of safety is reducing. The stock would not be able to sustain even a single weak quarter at a PE of 37

In the short term opportunities in Shilchar would be limited. FY25 performance would create the next short term opportunity.

Previous coverage of Shilchar

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

Perspectives may change based on evolving understanding of the company.

Focus is on identifying potential stock ideas for long-term market-beating returns.

Content does not constitute explicit stock recommendations.

Investors should conduct thorough stock research and seek professional advice.

Information is for educational purposes and not financial advice or a call to action.