Shilchar Technologies Ltd. is one of India’s prominent manufacturers of Electronics & Telecom and Power & Distribution transformers. Shilchar can manufacture transformers up to 50 MVA, 132 KV Class. Up to 4000 MVA of transformers can be manufactured annually.

The Company has concentrated on catering needs of renewable energy sector including solar and wind energy in local market where in the Company has been enjoying commendable position being one of the top companies in India supplying transformers for renewable energy.

2. FY20-23: Delivering growth and profitability

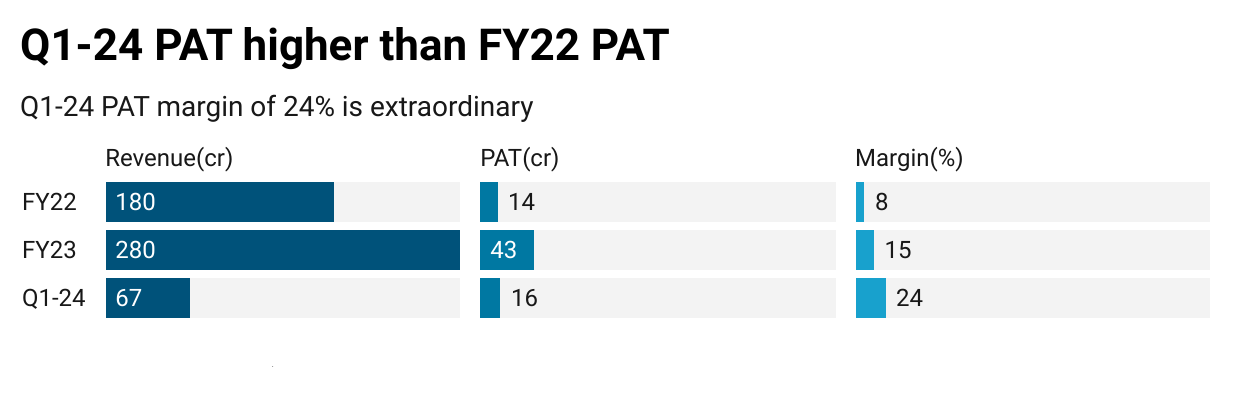

3. FY23: PAT up 207% and Revenue up 56% YoY

Operational income of Rs. 280 cr compared to Rs. 180 cr for the previous year. Profit after tax is Rs. 43 cr as compared to previous year figure of Rs. 1,9 cr.

4. Q1-24: PAT up 182% and Revenue up 17% YoY

One needs to watch out for the 24% PAT margin as it looks extra-ordinary and may not be sustainable.

Discussion in an online forum based on comments made my management in AGM

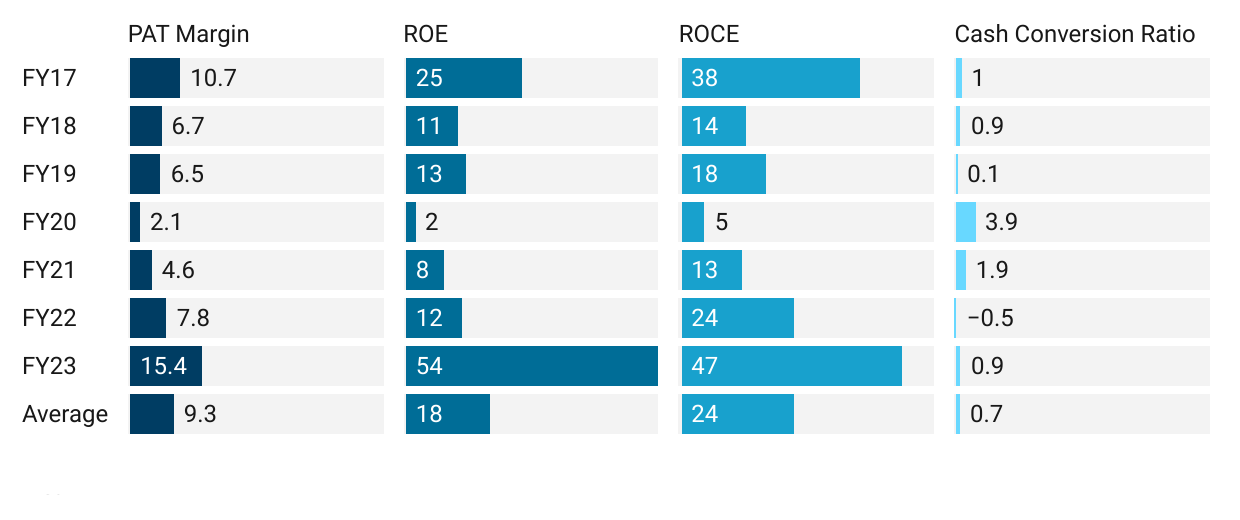

5. Business metrics recovering strongly after FY20

6. Outlook: 2.8X revenue by FY26

i. Management commentary is positive but lacking specifics

Industry tailwinds

A number of government initiatives to upgrade the current grids along with the installation of cutting-edge technology will fuel the expansion of the power transformer industry. Global demand is anticipated to be driven by an increase in the use of 100 MVA to 500 MVA products in transmission networks.

Domestic & Export demand strong

The government has also announced large target for installation of renewable energy capacity. This is generating high requirement of transformers for solar & wind applications.

Various governments in Middle East & Africa are also taking initiatives in renewable energy production which is driving high demand for transformers.

FY23 margins sustainable

Major threat for transformer industry is fluctuation in raw material cost like Copper, Steel, Oil, etc … The material cost has stabilize in last one year and there is no indication of any major fluctuation hence risk is minimal.

Strong order book

Distribution transformer division is having large orders on hand and it will continue to receive orders throughout the year due to high demand in foreign countries.

Medium power transformer division is also having good orders and due to large projects coming up in renewable sector all over the world, the demand will be generated continuously.

ii. Generic commentary corroborated by a capacity expansion

An Aug-23 post on Linkedin by Shilchar talking about a capacity expansion underway without any supporting details

Potential revenue of Rs 500 cr in FY25 looks reasonable and believable given the company has formally confirmed the capacity expansion

Discussion in an online forum based on comments made my management in AGM

iii. 40% revenue CAGR for FY23-26

Q1-23 contributed a bit more than 20% of FY23 revenue. Assuming no changes in FY24, one can extrapolate a revenue of Rs 329 cr for FY24 based on Rs 67 cr revenue in Q1-24. So the discussion about Rs 350 cr revenue in based on comments made by the management in the AGM looks reasonable and believable.

The aspiration for Rs 800-1000 cr revenue by FY26 makes it interesting even if we take a conservative view of Rs 800 cr by FY26 implying a 42% revenue CAGR.

Discussion in an online forum based on comments made my management in AGM

If I hold the stock then one may continue holding on to Shilchar. Potential of revenue becoming Rs 500 cr by FY25 and Rs 800 cr by FY26 is a good enough reason to hold the stock. Reaching Rs 500 cr by FY25 implies a 34% revenue CAGR. Reaching Rs 800 cr by FY26 implies a 40% revenue CAGR.

One needs to keep watching the quarterly results to check if Shilchar is on track to reach the revenue milestones.

9. Or, join the ride

If I am looking to enter the stock then

40%+ revenue CAGR till FY26 at a PE of 20 looks reasonable.

The industry tailwinds, the demand outlook, the order book and the proposed capacity expansion makes Shilchar a very interesting stock to look at. It is an efficiently run company.

The absence of information about the company makes it quite difficult for a retail investor to take a strong view on the stock.

Discussion in an online forum based on comments made my management in AGM

Given the limited information around Shilchar one can take very small positions and keep building them if the investment thesis is borne out.

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Thanks for reading Money Muscle! Subscribe for free to profit from new stock ideas.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades