Servotech Power Systems: Tripling in FY21-23, doubling in FY24, 5 times in FY23-25

First mover advantage in implementation of EV charging infrastructure. Well-positioned to capitalize on the growing demand for EV chargers & solar products

1. Producers & distributors of Solar products & EV charging solutions

servotech.in | NSE : SERVOTECH

Manufacturing, procurement and distribution of a range of high-end advanced solar products

Electric vehicle charging solutions

Manufacturing & selling of LED, UVC, and medical-grade products in India

25% market share in EV charging solutions

We continue to remain one of the dominant players in the sustainable energy space, capturing ~ 25% of the market share in EV charging solutions

A first mover advantage in implementation of EV charging infrastructure as reflected by a strong and growing major market share owing to continued patronage from its esteemed clients like BPCL, Nyara and other OMC’s.

Product Categories

Subsidiaries

Rebreathe Medical Devices India Private Ltd: Manufacturing medical grade oxygen concentrators and other medical appliances and instrument

Techbec Industries Limited (63.5%) engaged in manufacturing Li-Ion, Tubular Battery, and Energy Storage Solutions

2. FY21-23: 12X PAT as revenue tripled between FY21-23

FY21-23

Revenue = Up from Rs 88 cr to Rs 279 cr at a CAGR of 78%

PAT = Up from Rs 0.9 cr to Rs 11 cr at a CAGR of 245%

ROE = Up from 2.4% to 13.5%

3. FY23: PAT up 173% on revenue growth of 93%

On the Financial performance front, we've experienced a robust growth as reflected by increased revenue which stood at Rs. 278.64.3 cr in FY23 showing a remarkable YoY growth of 93.2% against the revenue of Rs. 144.253 cr in FY22. Our EBITDA margins during Q4 & FY23 performance stood at 7.5% and 6.8% respectively

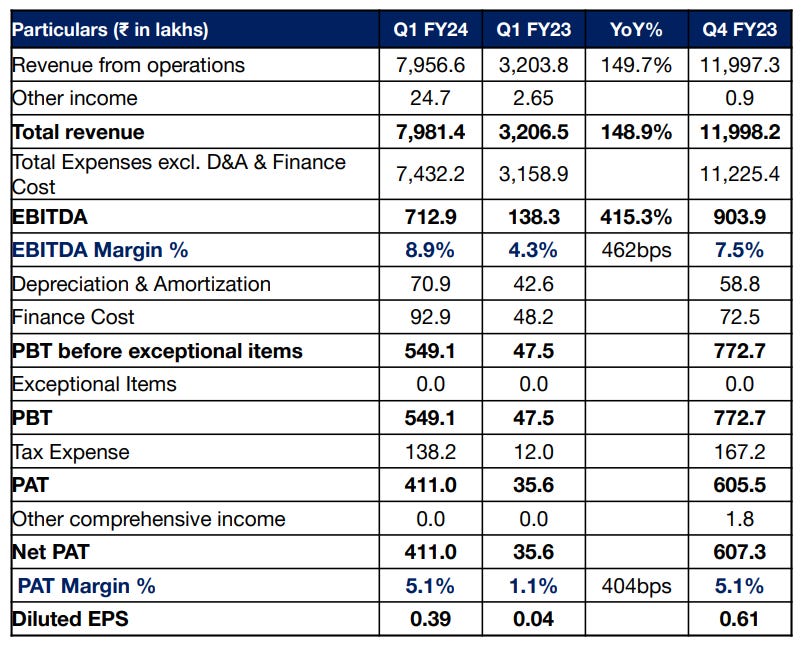

4. Q1-24: 11.6X PAT and 2.5X revenue YoY

Revenue from operations increased by 149.7% from ₹ 31.865 cr in Q1 FY23 to ₹ 79.566 cr in Q1 FY24.

EBITDA margins improved from 4.3% in Q1 FY23 to 8.9% in Q1 FY24

Net PAT margins improved from 1.1% in Q1 FY23 to 5.1% in Q1 FY24.

Net PAT stood at ₹4.11 cr in Q1 FY24, compared to ₹ 0.356 cr Q1 FY23.

5. Outlook: Doubling in FY24; growing 5 times by FY25

i. Doubling in FY24: Revenue to grow by 90%-110% for FY24

ii. Margin expansion: FY24 EBITDA of 9-11% vs 6.8% in FY23

iii. FY23-25 guidance to become 5X+ i.e. 132% CAGR growth

EV Chargers: To scale up the revenue from ₹240 Crs to ~₹1,200 Crs by 2025

Lithium Battery: To scale up the revenue from ₹85 Crs to ~₹850 Crs by 2027

Conservative estimate of FY25 revenue would be Rs 1500+ cr, this translates into SERVOTECH becoming 5X+ in size growing at 132%+ CAGR

iv. Ambition to be 20X in 6-7 years

Ambition of MD & Founder, noted but not considered in the analysis

Raman Bhatia: And, in the next 6-7 years, if we do a turnover of 5-7 thousand crores, then we have achieved nothing. We have not done anything big that we can say we have achieved something big. Despite this, as a Servotech, if we talk about it, it will become 20 times bigger than it is today.

6. Doubling in FY24 at PE of 55

Strong track record of revenue growth

FY21-23 = 78% CAGR

FY23 = 93%

FY24 guidance = 90%-110%

FY23-25 guidance = 132%+

8. So Wait and Watch

If I hold the stock then one can definitely hold on to SERVOTECH as long as the blistering pace of growth continues and one can see the EV story playing out. One should have the flexibility to patient if one weak quarter slip in between as doubling the company or growing it to five times the size by FY25 can be quite challenging as the base increases.

9. Or, join the ride

If I am looking to enter the stock then

SERVOTECH is guiding for a revenue growth of 90-110%+ for FY24 which makes the PE of 55 look very reasonably priced.

PAT expected to grow faster than the top-line as EBIDTA margin expected to expand from 6.8% in FY23 to 9-11% in FY24

Intent to take revenue to five times between FY23-25 implies a topline growth CAGR of 132%+.

SERVOTECH is running at a run rate of around 100% growth, but this growth may get tested as it becomes Rs 1000 cr company which could happen around H2-24.

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades