Senores Pharmaceuticals FY26 Results: PAT up 105%, On-track FY26 Guidance

Guiding 50-60% PAT growth in FY27 with 30-40% revenue growth. Revenue CAGR of 25-30% & PAT CAGR of 20-30% for next 3-5 years. At reasonable forward valuation

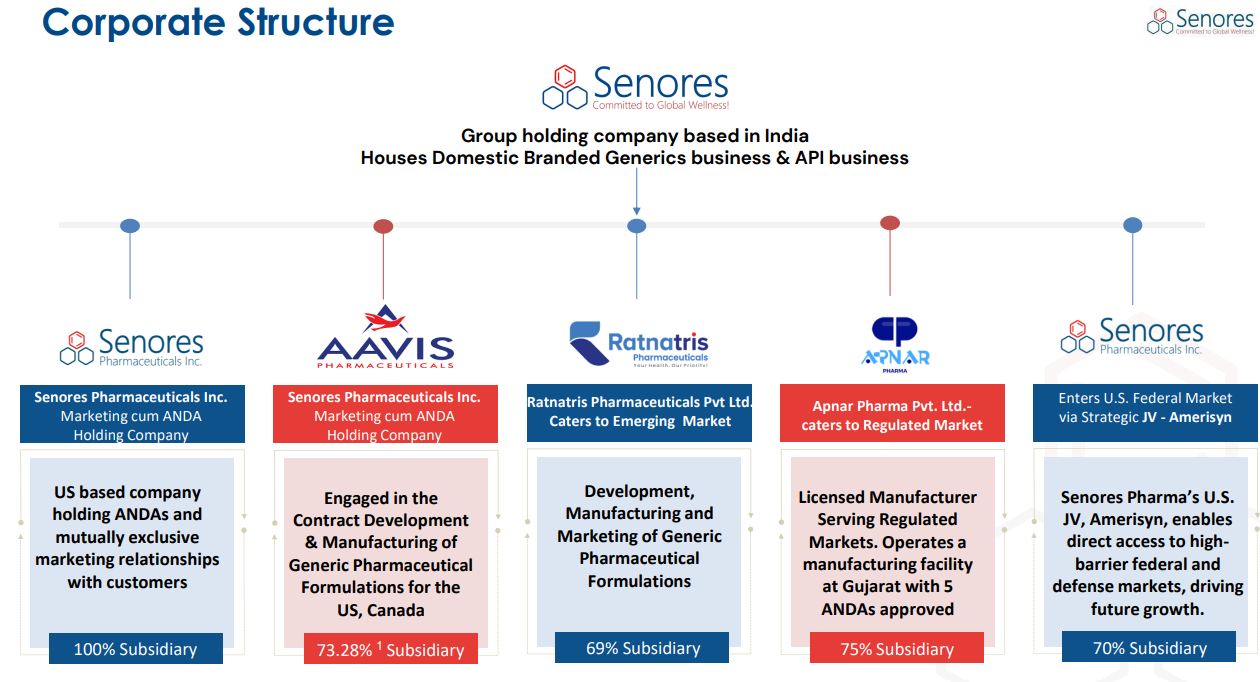

1. Pharmaceutical Company

senorespharma.com | NSE: SENORES

Regulated markets — the core business

Serves US, Canada and UK through approved ANDAs and marketing/distribution partnerships.

Model is to identify specialty and complex niche products, develop them, get approvals, and commercialize them through partners or its own platforms.

CDMO / CMO business

Focuses on specialty products, government supplies and controlled substances, with contracts for more than 40 products across the US, Canada, UK, South Africa, UAE, Israel, Denmark, Saudi Arabia and Vietnam.

Emerging markets business

Sells generic products in 40+ countries, mainly emerging markets.

Top emerging markets include the Philippines, Peru, Ghana, Nigeria, Myanmar, Guatemala and Kenya.

Lower-margin than regulated markets, but it gives geographical diversification.

India branded generics

Critical-care injectable products in India through hospitals and distributors.

Still a small business, but management is using hospital approvals and field-force expansion to grow it.

API business

Strategically useful because it can reduce dependence on third-party suppliers and improve cost control. But it also requires capital and execution.

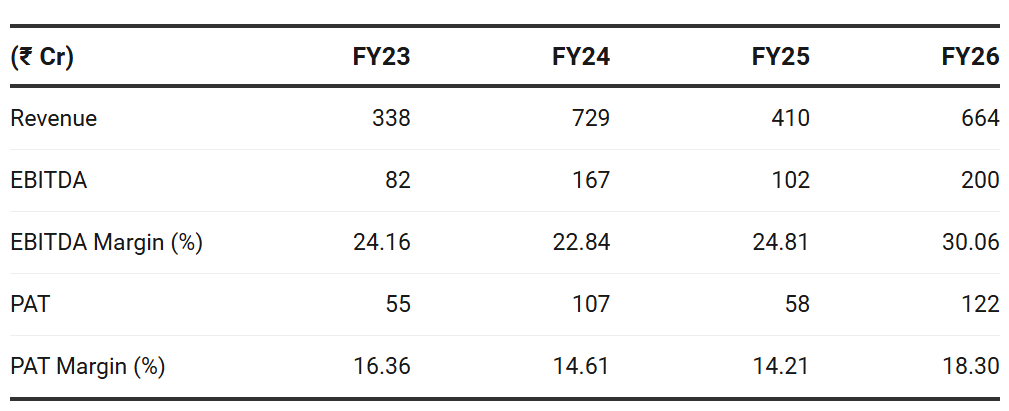

2. FY23-26: PAT up 48% & Revenue up 25% CAGR

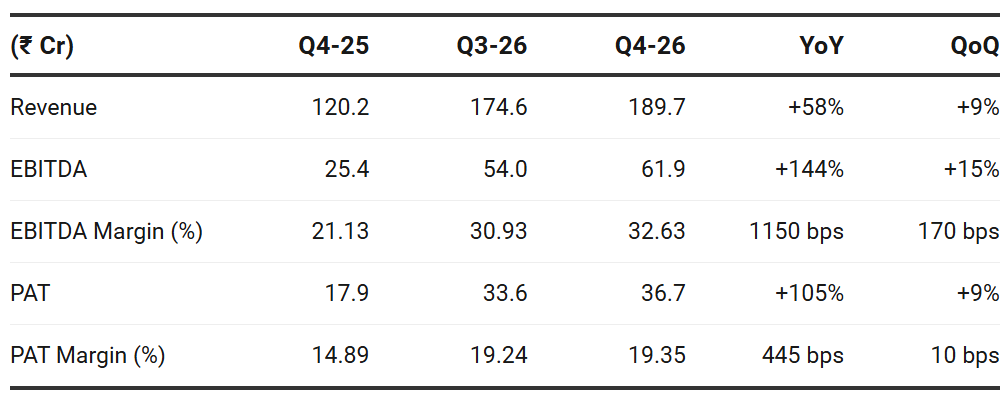

3. Q4 FY26: PAT up 105% & Revenue up 58% YoY

PAT up 9% & Revenue up 9% QoQ

4. FY26: PAT up 108% & Revenue up 62% YoY

Acquisition of Zoraya Pharmaceuticals

Zoraya is being established as strategic initiative to strengthen vertical integration, from the acquired ANDA portfolio to be commercialized under the Zoraya platform, which will serve as a dedicated market-facing brand.

Acquisition of Apnar Pharmaceuticals

Entered U.S. Federal Market via Strategic JV

Entered into a 70% joint venture, Amerisyn, in the U.S., creating a direct pathway to supply pharmaceuticals to federal, veterans, and defense sectors.

Opens access to a high entry barrier market and is expected to drive future growth

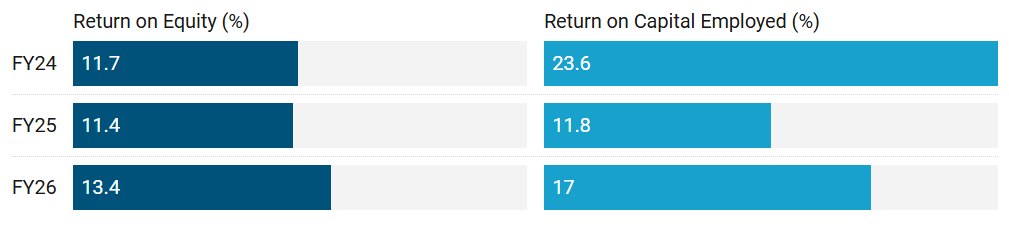

5. Business Metrics: Improving Return Ratios

6. Outlook: 50-60% PAT Growth in FY27

6.1 FY27 Guidance

Guiding for 30–40% revenue growth this fiscal year, with profit after tax expected to expand at an even sharper 50–60% clip

We expect steady-state EBITDA margins to return to around 29–31%, which we have consistently guided for and delivered over the last few quarters. That should happen as we ramp up on the Apnar over the next few quarters.

Management emphasized that this top-line guidance is currently a conservative, “minimum achievable” estimate.

Because of external uncertainties—such as issues with shipping lines and inflationary pressures in the US—they are choosing to wait for one or two quarters to observe global macroeconomic conditions before potentially revising this guidance upwards.

Regulated Markets & US Operations

Growth strategy for its US operations, setting a target to build ₹2,500-3,000 Cr in revenue from the US over the next 3 to 4 years. Key drivers for this outlook include:

Product Rollouts: Senores has 51 approved ANDAs, of which 20 are currently launched. They plan to commercialize 90% to 95% of these approved ANDAs over the next 6 to 8 quarters.

Upnar Facility Contributions:

Newly acquired Upnar plant projected to generate ₹80-100 Cr FY27 revenue with the potential to scale to ₹180-200 Cr within 2-3 years.

US Joint Venture (Amiring): The strategic JV focused on US government procurement contracts is expected to contribute approximately ₹50-80 Cr in its first year, operating at strong EBITDA margins averaging around 40%.

Emerging Markets

Expecting revenue to reach approximately ₹180 crores in FY27.

Segment’s EBITDA margin, currently around 18-19%, is expected to settle between 20-21% in FY27.

Anticipates an additional 200 to 300 basis point jump in margins once segment revenue crosses the ₹220-250 Cr threshold.

India Branded Generics

To achieve ₹60-70 Cr in FY27.

Capital Expenditure & Cash Flow

CapEx: Total capital expenditure planned for FY27 is around ₹200 Cr.

Cash Flow: Bolstered by disciplined working capital management, the company expects to generate positive free cash flow in FY27.

6.2 FY26 Performance vs FY26 Guidance

Achieved FY26 guidance

Raised FY27 guidance when compared to the outlook for FY27 provided during Q3-FY26 earnings call

FY26 Guidance

Confident of delivering at least 50% growth in top line and 100% growth in PAT for FY26 over FY25.

FY27 Onwards

Revenue Growth: So post this year FY 27 I think sustainable growth on a CAGR basis should be between 25 and 30%. That is what we’ve targeted. I mean with a positive launches it this could well exceed but from our internal target perspective — at least 30% CAGR sustainable growth over over next 3 to 5 years is very much visible for us and which will continue to deliver.

PAT Growth: 20 to 30% is what we are looking at from next year onwards

PAT as a percentage will improve by couple of hundred bips that’s what we are looking at

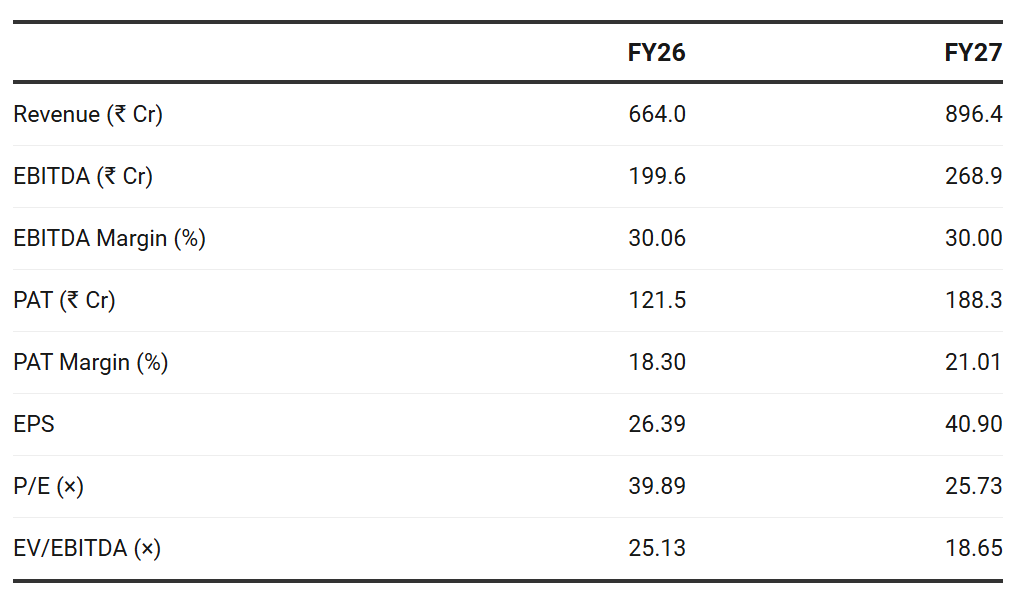

7. Valuation Analysis — Senores Pharmaceuticals

7.1 Valuation Snapshot

Current Market Price — ₹1,052.6

Market cap ₹ — 4,847.60 Cr

Assumptions:

Revenue growth at 35% for FY27 — mid-point of guidance

PAT growth at 55% for FY27 — mid-point of guidance

Stable EBITDA margins

Market cap is already ahead of FY26 fundamentals and is waiting for FY27 earnings to justify it.

If FY27 guidance is delivered, the stock moves from expensive on FY26 earnings to reasonable-but-still-premium on FY27 earnings.

But on the 3–4 year US revenue opportunity, the stock still has meaningful upside if management executes.

The key valuation trigger is: ₹2,500-3,000 Cr US revenue with stable margins

If that happens, Senores can justify a 2-3x market cap.

But if US revenue scales slower than guided, the current valuation already leaves limited margin of safety.

7.2 Opportunities at Current Valuation

FY27 earnings can make today’s valuation look reasonable

Senores is not cheap on FY26 numbers. The opportunity is not “value stock cheapness.” The opportunity is earnings catch-up + execution-led re-rating.

Regulated-market business is already high-margin

64% of total revenue, with 39% EBITDA margin — The strongest part of the business.

That matters because a high-growth, high-margin regulated-market business can deserve a premium valuation if execution continues.

30 approved ANDAs are yet to launch

This is the biggest operating trigger.

90–95% of the 51 approved ANDAs expected to be commercialized over 6–8 quarters, though peak revenue may take 2–5 years.

FY27/FY28 earnings can grow faster than the market expects if these pending launches convert into revenue without major pricing pressure.

Apnar can unlock capacity and improve operating leverage

Apnar is important because it gives Senores an India-based regulated-market manufacturing asset.

Apnar has USFDA, MHRA and Health Canada approvals, 5 ANDAs / 15 strengths approved, and acquired products with total addressable market of about USD 722 Mn.

Apnar suppressed FY26 margins by about 100 bps because expenses came before revenue.

US revenue aspiration can create multi-year upside

Management’s longer-term aspiration is much larger than FY26 revenue.

On the Q4 call, they spoke about building ₹2,500-3,000 Cr, even ₹3,000–4,000 Cr, of US revenue over the next 3–5 years.

This is the big long-term optionality.

If the US business scales even to the lower end of management’s aspiration, current valuation can still leave meaningful upside.

Senores is not a margin-of-safety stock. It is an execution-led compounding opportunity

8.3 Risks at Current Valuation

FY27 growth is already priced in

Delivering FY27 guidance will require exceptionally strong performance

If FY27 earnings disappoint even slightly, the stock can de-rate sharply because the FY26 valuation does not offer much protection.

Cash conversion risk: PAT is not yet converting well into cash

FY26 PAT of ₹121.5 Cr, but net cash flow from operating activities was only ₹62 Cr.

At 45x FY26 earnings, weak cash conversion is a valuation risk.

The market may tolerate it during a high-growth phase, but only if FY27 shows improvement.

Revenue turning in to Receivables + other financial assets

Trade receivables of ₹324.8 Cr and other current financial assets of ₹172.7 Cr as of Mar-26. That is ₹497.5 Cr — very high versus FY26 revenue of ₹632.6 Cr — as % of revenue ~79%

Management explained on the call that other financial assets relate to profit-share / unbilled revenue under the B2B model and should be collected over 1–6 months.

If this line item keeps rising, the market may start questioning earnings quality.

Apnar ramp-up risk

Apnar is now central to FY27.

Management expects Apnar to contribute ₹80–100 Cr revenue in FY27, after only modest Q4 contribution.

They also said Apnar suppressed FY26 margins by around 100 bps because costs came before revenue.

ANDA commercialization risk

This is the biggest opportunity, but at current valuation it is also a risk.Approval is not revenue. Senores still has to launch, gain market share, manage US price erosion, collect profit share, and convert sales into cash.

Launch delays, lower-than-expected market share, or pricing pressure in US generics could turn opportunity to risk

Free cash flow risk

Management said FY27 capex could be around ₹200 Cr, including ₹100 Cr of IPO-funded sterile manufacturing and another ₹100 Cr for other growth/maintenance capex. They also suggested FY27 free cash flow should be positive.

The risk is in the definition.

IPO funds can finance capex, but they do not make free cash flow positive. True free cash flow is:

Net CFO − capex

FY26 net CFO was only ₹62 Cr. To generate true positive FCF after ₹200 Cr capex, Senores needs a very large jump in operating cash flow.

Risk trigger: CFO improves, but not enough to cover capex.

Previous Coverage of SENORES

Help your group stay ahead. Share now!

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer