SBI Life vs HDFC Life vs ICICI Pru: Valuation Analysis FY26

FY26 performance analysis of SBI Life, HDFC Life, and ICICI Prudential. Comparison on growth, margins, and relative valuations to find the best stock opportunities

1. FY26 Business Performance

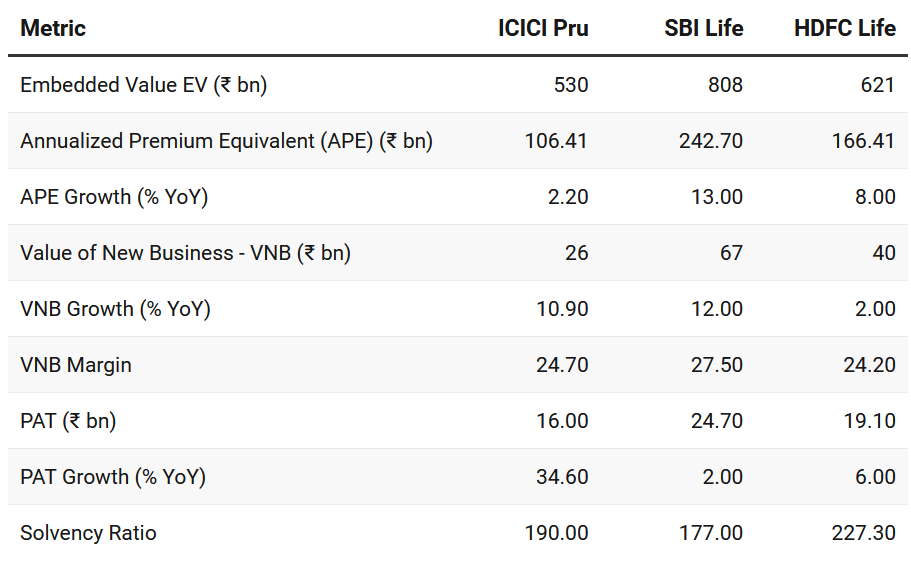

Operational Scorecard (FY2026)

The following table summarizes the key operational metrics that drove business performance in FY26 of

ICICI Prudential Life Insurance Company

SBI Life Insurance Company

HDFC Life Insurance Company

FY26 Performance Analysis

The Growth Leader (SBI Life): SBI Life continues to be the only company delivering a “Double-Double”—double-digit growth in both sales (13%) and profitability (12%). Its massive distribution network (Bancassurance) allows it to maintain a industry-leading 27.5% VNB margin, showing that it can grow fast without sacrificing quality.

The Efficiency Play (ICICI Prudential): ICICI Pru presents a fascinating story. Its top-line sales growth was nearly stagnant at 2.2%, yet its Value of New Business (VNB) grew by 10.9% and its Net Profit jumped by a massive 34.6%. This indicates a successful pivot: they are selling fewer but far more profitable products and aggressively cutting operational costs.

The Defensive Fortress (ICICI Prudential): With a 227.3% Solvency Ratio, ICICI Pru is the safest “fortress” in the sector. This high capital buffer suggests they have significant room to increase dividends or reinvest aggressively when market conditions improve.

The Resilience Story (HDFC Life): HDFC Life faced a tougher year, with VNB growth lagging at 2%. Regulatory impacts on their specific product mix (Annuities and Protection) acted as a drag. However, their 8% APE growth shows they are still successfully defending their market share.

2. Valuation Analysis: Market Cap vs. Intrinsic Value

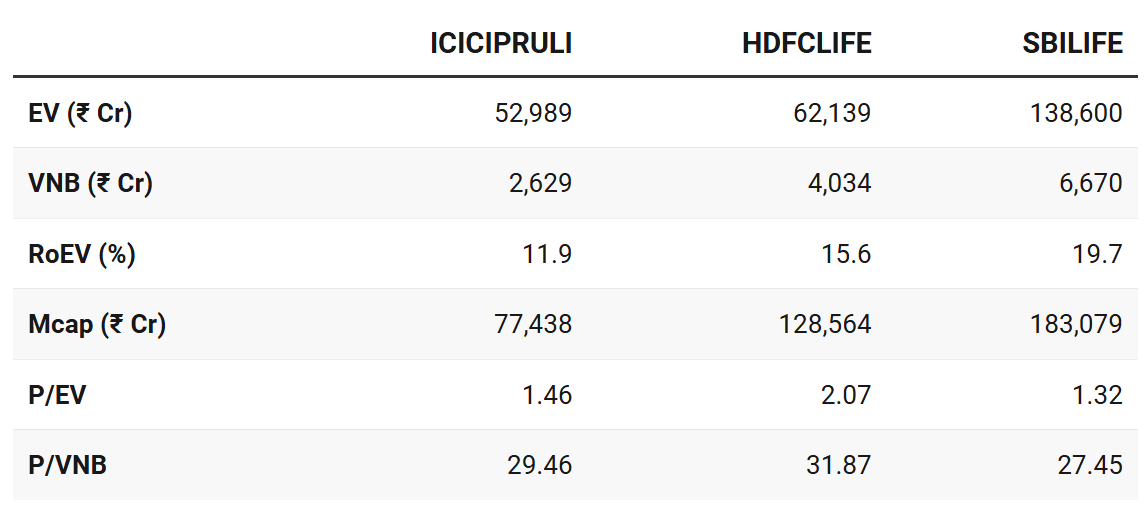

Valuation Matrix (FY2026)

Analysis of the Valuation Gap

The SBI Life: The most striking takeaway is that SBI Life is the cheapest stock despite being the best performer. It has the highest internal compounding rate (19.7% RoEV) but trades at the lowest multiple (1.32x P/EV). The market is effectively pricing it at a discount, likely due to its PSU-parentage perception, creating a classic “Growth at a Reasonable Price” (GARP) opportunity.

The HDFC Premium: HDFC Life remains the most expensive stock at 2.07x P/EV. Investors are clearly paying a “brand and pedigree premium.” Despite lower RoEV than SBI Life, the market values HDFC’s sophisticated product mix and dominant retail presence, resulting in a high P/VNB of 31.87x.

The ICICI Pru Stability: ICICI Pru sits at a fair 1.46x P/EV. Its valuation reflects its current status as a stable, high-solvency player with lower RoEV (11.9%). However, if its high PAT growth continues, it is the prime candidate for a valuation “re-rating.”

3. Identifying the Opportunities

SBI Life

SBI Life represents a absolute value play. A company compounding its internal value (RoEV) at nearly 20% while trading at just 1.32x its book value (P/EV) is an opportunity.

This is not just “relative value” because it’s cheaper than HDFC; it is real value. SBI Life’s VNB margin of 27.5% is the highest in the sector, yet its P/VNB multiple (27.45x) is the lowest.

For long-term portfolios, SBI Life offers the best “Safety Margin.” You are buying the industry’s most efficient growth engine at a discount price.

ICICI Prudential

The opportunity in ICICI Pru is a valuation re-rating play. While its current RoEV (11.9%) justifies its lower 1.46x P/EV, the massive 34.6% PAT growth suggests that the company has fixed its cost structure.

There is hidden value here. ICICI Pru has essentially “over-capitalized” its balance sheet (227.3% Solvency). This extra capital is currently a drag on RoEV, but it provides the company with “dry powder” to either hike dividends significantly or fund an aggressive acquisition without needing fresh equity.

This is a play for investors betting on a “Mean Reversion.” If that profit growth eventually drives RoEV toward 15%, the stock could re-rate from a 1.4x multiple to a 1.8x multiple.

HDFC Life

HDFC Life is currently a momentum and brand play, but the FY26 numbers suggest caution. Trading at 2.07x P/EV (a 56% premium over SBI Life) while its VNB growth has slowed to a mere 2% creates a potential “Expectation Gap.”

This is relative overvaluation. While HDFC Life is a high-quality business with superior 61-month persistency (64%), the stock market is charging a “perfection premium.” For the current price to be “real value,” VNB growth needs to accelerate significantly to catch up with its high P/VNB multiple of 31.87x.

HDFC Life remains a core “blue-chip” hold, but at current levels, it offers the least “valuation upside” compared to its peers.

Summary Comparison for Stock Investors

Highest Upside Potential

SBI Life — Highest growth (20% RoEV) at the lowest price (1.3x P/EV)

Downside Protection

ICICI Pru — Strongest capital buffer (227% Solvency) and massive profit growth.

Brand & Stickiness — HDFC Life — Best long-term customer retention and premium product engine.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer