Satin Creditcare Network: 41% revenue growth & return to profitability in H1-24 for a PE of less than 7 and price to book of 1.24

After losses in the last 3 years, delivering a strong H1-24. Performance in H1-24 ahead of FY24 guidance. At reasonable valuations. Risks remain even after a strong H1-24 & reasonable valuations

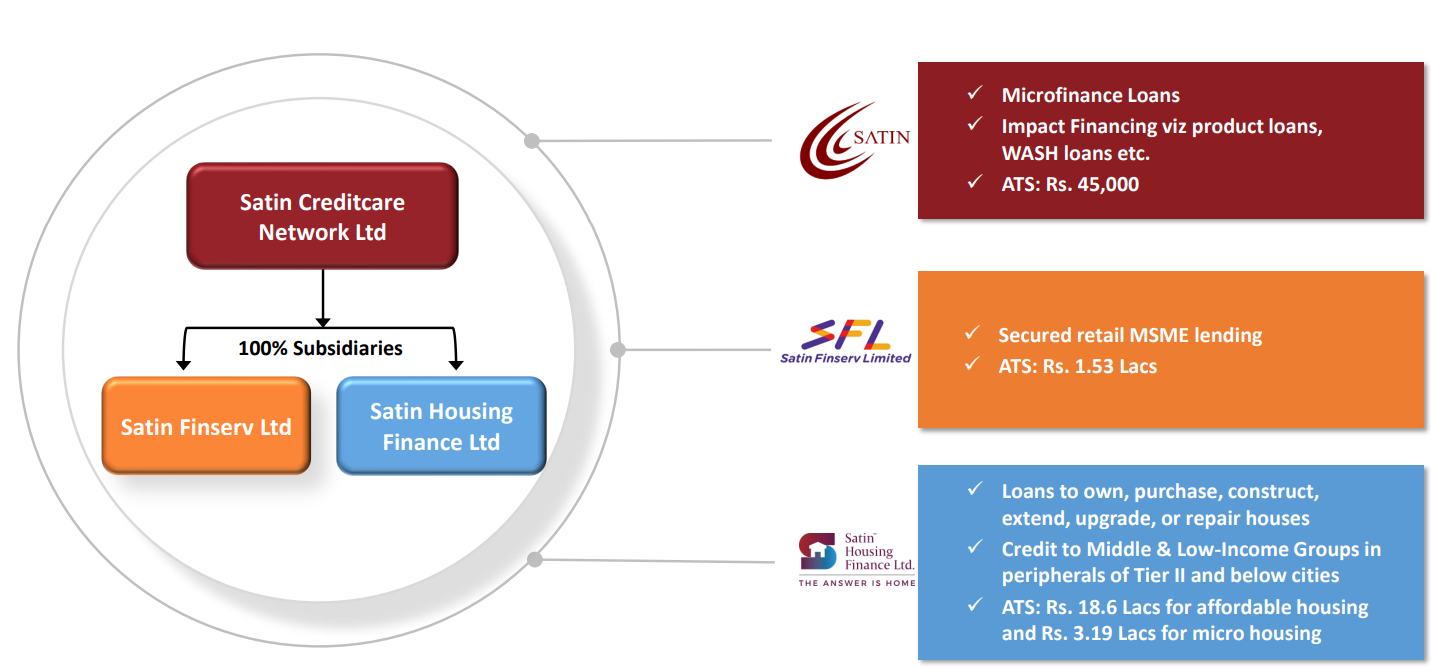

1. Microfinance company

satincreditcare.com | NSE: SATIN

Group Structure

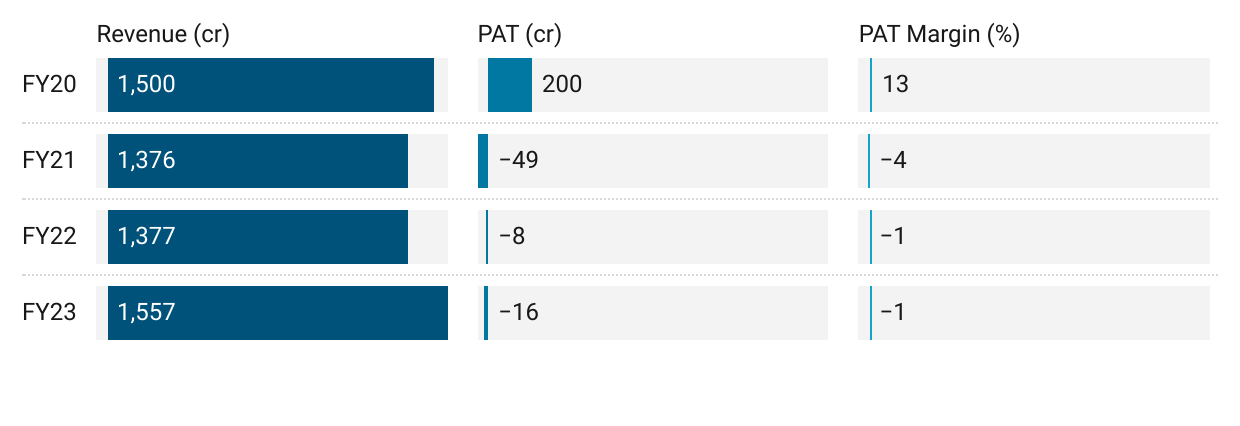

2. Weak FY20-FY23: A weak track record. 3 years of losses

3. Strong Q1-24: Revenue up 34% YoY and back in profit

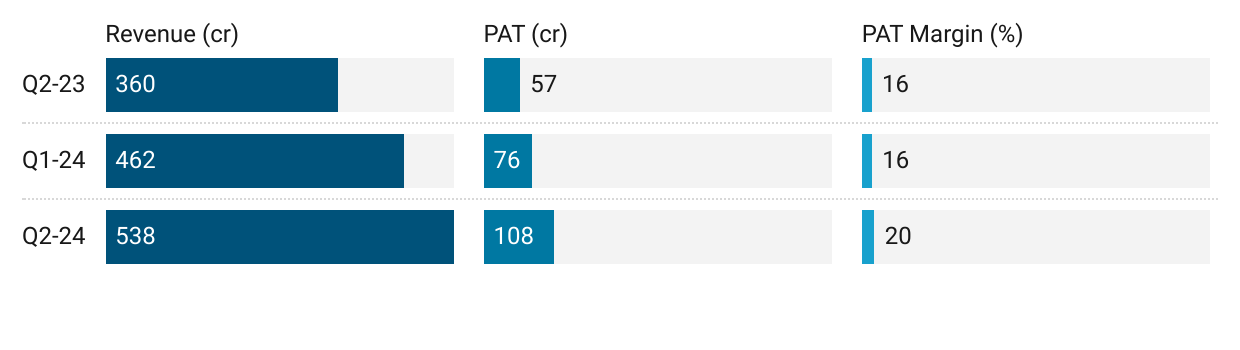

4. Strong Q2-24: PAT up 90% and Revenue up 49% YoY

PAT up 41% Revenue up 16% with expansion in margin QoQ

ROA of 4.8% and ROE of 23.6%.

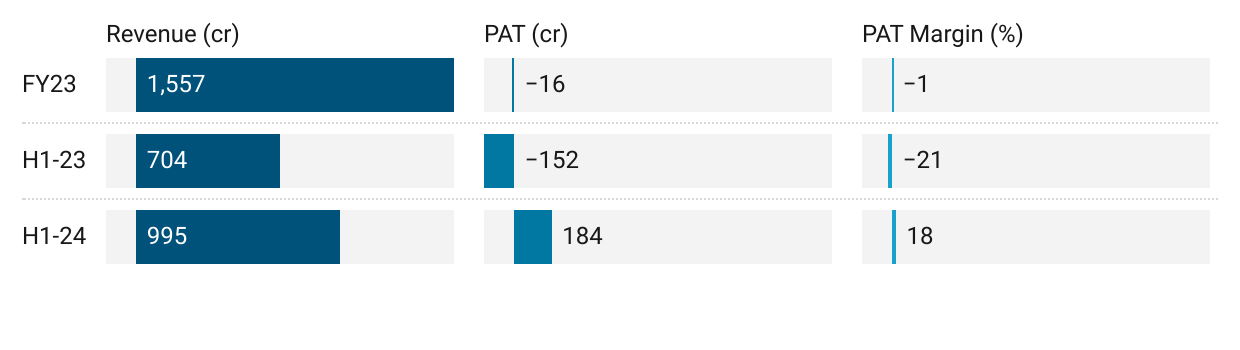

5. Strong H1-24: Revenue up 41% YoY and back to profit

Highest ever H1 profitability in last 5 years

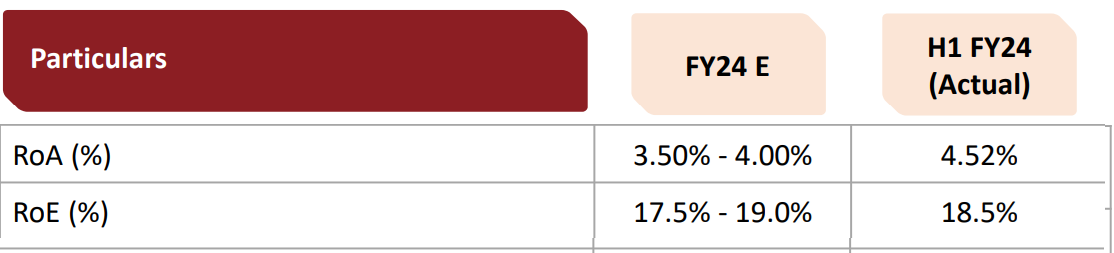

6. Business Metrics: Return ratios looking positive in FY24

Strong RoA & RoE as of H1-24 which are ahead of FY24 guidance.

7. Outlook: On-track to beating guidance for FY24

i. H1-24 performance ahead of FY24 guidance

ii. Risks in business model: PAT generated has been written-off

Most of the PAT generated has been written-off on account of various crises.

7. 41% revenue growth with return to profitability at a PE of less than 7

6. So Wait and Watch

If I hold the stock then one can hold on to SATIN

SATIN is looking to delivering a FY24 guidance beating performance based on H1-24 results. One can stay in as long as top-line and bottom-line growth is being delivered.

Price of the stock provides some margin of safety

Along with a weak track record in terms of FY20-23 performance, the reduction in promoter holding in Q2-24 has added to questions around SATIN

The promoters have decreased holdings from 41.70 percent in the June quarter to 39.98 percent in September quarter. FIIs and DIIs hold 6.9 percent and 4 percent of the shares, respectively. The public is the largest shareholder, with holdings of 48.6 percent.

One needs to watch for performance on a quarter to quarter basis and be willing to exit quickly if performance weakens. SATIN track record in the recent past has been weak.

7. Or, join the ride

If I am looking to enter SATIN then

For the growth SATIN has delivered in H1-24, the PE of less than 7 looks attractive against the management guidance for FY24.

At a book value of Rs 191 the stock is available at price to book (P/B) of less than 1.3 which offers headroom for increase in the P/B multiple

Possibility of SATIN delivering ahead of the guidance in FY24.

However, the weak track record, ability of the business to grow its net worth on account of the write-offs and the reduction in promoter holding makes it a risky stock.

On the other side, highest ever H1 profitability in last 5 years was achieved in H1-24 and if we get more of such quarters then why cant the stock price be the best price in the last 5 years?

Previous coverage of SATIN

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades