Rategain Travel Technologies: Growing at a 50% CAGR FY21-23, 2X in FY24-26

Robust revenue growth and margin expansion year-over-year leading to upgrade of the FY24 growth guidance after Q1-24. Focused on the new aspirational goal of doubling revenues

1. India’s Largest SaaS company in hospitality & travel

rategain.com | NSE : RATEGAIN

RateGain Travel Technologies Limited is a provider of SaaS solutions for travel and hospitality, and one of the world’s largest processors of electronic transactions, price points, and travel intent data.

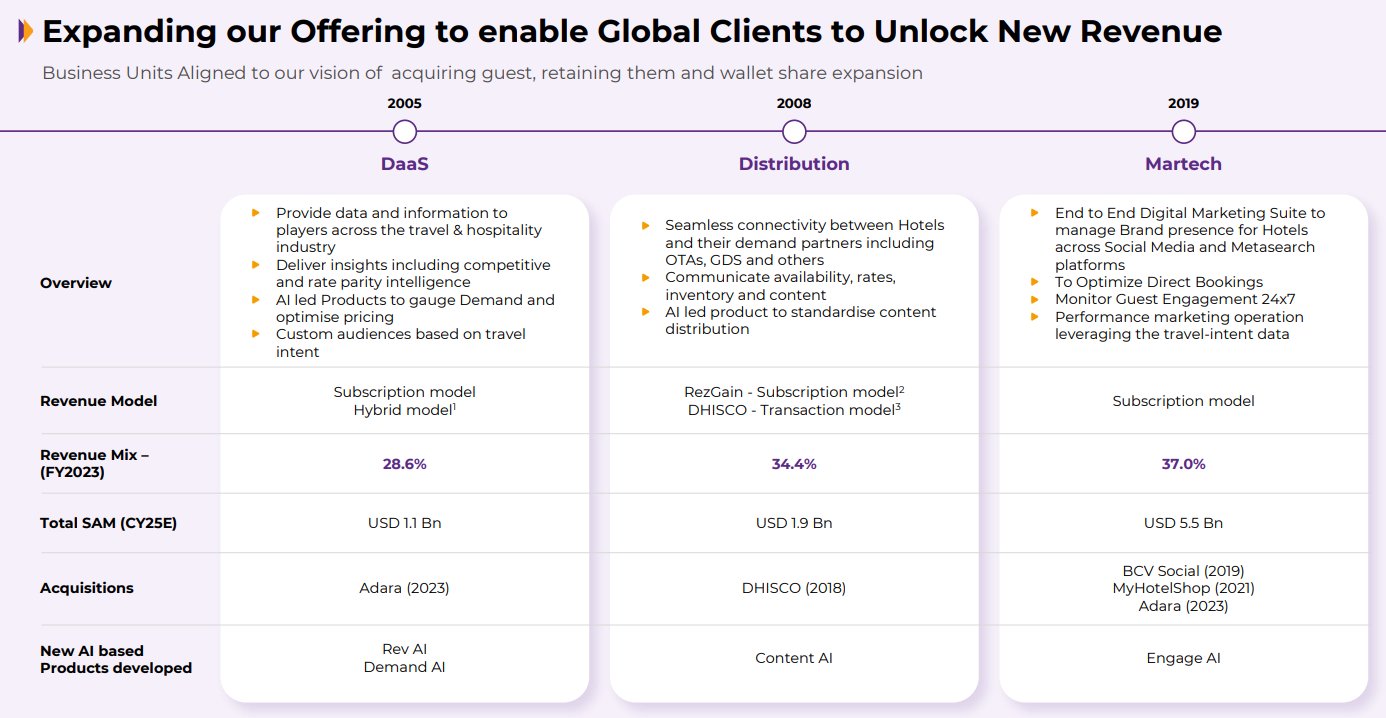

Business Units

MarTech: Helping hotels drive more ROI through digital

Distribution: Reaching the Right Guest

Data-as-a-Service: Enabling hotels, car rentals, and ferries plan their demand and pricing strategy using the automated AI powered pricing recommendation platform as well as a demand forecasting solution

2. Growing at a 50% CAGR FY21-23

Strong profitability metrics supported by improved positive cash flow generated from Operating Activities

3. FY23: PAT up 8X+ on revenue growth of 54%

Revenue for FY23 stood at INR565 crores with a growth of 54%. Margin improvement has been strong as we reported a 17.6% EBITDA margin in our Q4 and 15% for the full year, well ahead of the guidance given at the time of the IPO of 200 to 300 basis points expansion from the 8.3% margin we reported last year.

PAT grew significantly last year to 68.6 crores from INR8.4 crores almost eight times

4. Q1-24: PAT up 3X on revenue growth of 80% YoY

A revenue of INR214.5 crores with a year-over year growth of 80%. We had well rounded growth from all three verticals with DaaS growing 139% distribution at 27% and MarTech at 88% for the full year.

PAT grew three times compared to last year, coming to INR24.9 crores up from INR8.4 crores. Sequentially the PAT was lower on account of one-time benefit of deferred tax asset benefit which positively impacted the PAT last quarter. Without the one-time benefit, the PAT grew sequentially by 15%.

5. Revenue visibility: 90% revenue retention

Look 90% gross recurring revenue, gross retention -- gross revenue retention, which is called GRR, is a SaaS benchmark and 90% is a good metric for SaaS companies and on an NRR front, anything between 110% to 120% is a good benchmark for SaaS companies and we track them pretty seriously and this shows the mining of existing clients because our clear strategy is to land and expand. So, majority of our growth if we talk about, is coming from existing clients and that's how the net retention rates, we continue to try to thrive to increase the net revenue retention. NRR denotes the growth of our existing relationships.

6. Outlook:

i. Original guidance of 55-58% growth in FY24

In terms of guidance for financial year 2024, we expect to grow around 55% to 58% and end up around INR875 crores to INR890 crores revenue in FY ‘24. On the margin front, we expect to see a 200 basis point expansion year-over-year to 17%. Our Q1 is a soft quarter, both in terms of revenue and EBITDA due to seasonality of the business and also the annual pay review impact starts kicking in in Q1. Our EBITDA margin in Q1 will be around 13.5% and gradually increase to 20% in Q4, delivering an average 17% EBITDA for the year. We expect to deliver a PAT of around 12% and EPS around INR10 per share next year.

As of Q4-23

ii. FY24 guidance on growth and margins to be beaten

In terms of guidance for FY’24 for the full year, we're confident of beating the growth guidance given last time. And similarly, we would be looking to exceed the 17% margin guidance given for the full year.

As of Q1-24

ii. Doubling the revenue in the next three years i.e 41% CAGR growth for FY24-26

If you do a 25% growth, you can actually double the company in four years. And I do believe very, very strongly that given the tailwinds that we have the acceleration in our products and sales and marketing that we can achieve that 20%, 25% organic growth. And then in addition to that our inorganic play, which, we've demonstrated that we have a playbook that will add to the rest. So that gives us the confidence of aspiring to that goal of doubling revenues.

7. 60%+ EPS growth in FY24 to be followed up by 41% revenue growth for FY24-26 at a PE of 76 (TTM) and PE of less than 59 based on FY24 EPS

EPS expected to grow from 6.29 in FY23 to 10+ based on FY24 guidance. EPS of around 10 was the original guidance for FY24. Given that the EBIDTA guidance has been increased, one can expect a 10+ EPS for FY24. This implies that PE based on FY24 earnings will be less than 59.

This translates to an EPS growth of 60%+ in FY24

8. So Wait and Watch

If I hold the stock then one can definitely hold on to RATEGAIN as long as the blistering pace of growth continues. One should have the flexibility to patient if one weak quarter slip in between as top-line growth close to 50% can be quite challenging as the base increases.

9. Or, join the ride

If I am looking to enter the stock then

RATEGAIN is guiding for a PAT CAGR of 60%+ for FY24 which makes the PE (TTM) of 76 and around 59 based on FY24 EPS look fairly valued.

Intent to double revenues in during FY24-26 implies a topline growth CAHR of 41%. Given that PAT is growing faster than the revenue due to margin expansion one can expect earnings growth in the 50%+ range and making the PE of 59 (based on FY24 EPS) look reasonable.

RATEGAIN gross revenue retention (GRR) ratio has remained consistently high at 90% resulting in high renewal business from existing customers and helps in building predictive, stable, and sustainable revenue streams.

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades