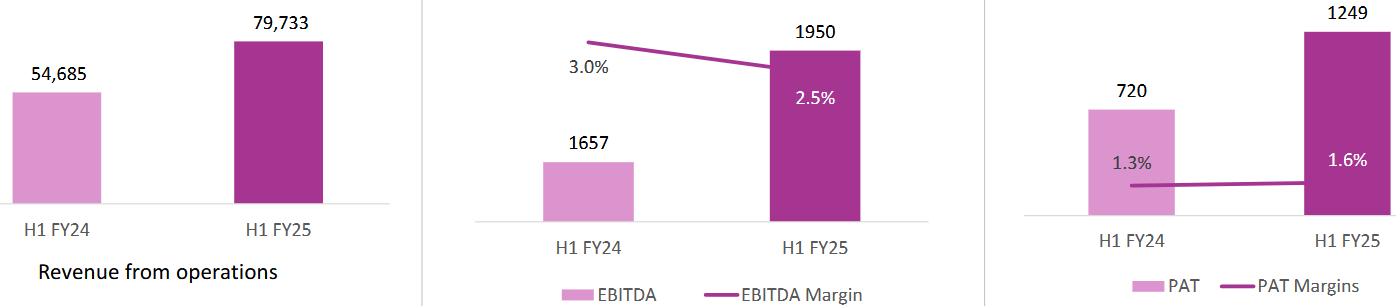

Rashi Peripherals: PAT growth of 64% & revenue growth of 46% in H1-25 at a PE of 14

Revenue CAGR of 20% delivered over the long term. FY-25 expected to be strong based on H1-25 performance. Available at reasonable valuations. At a price to book of 1.5

1. Ranks among top 5 Category-B IT hardware distributors

rptechindia.com | NSE: RPTECH

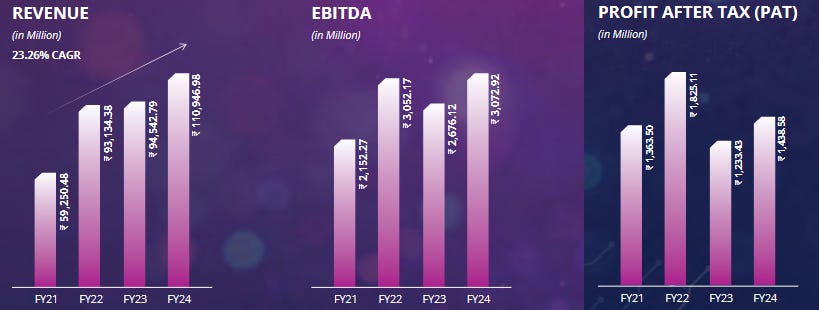

2. FY20-24: PAT CAGR of 34% & Revenue CAGR of 21%

3. FY24: PAT up 17% & Revenue up 17% YoY

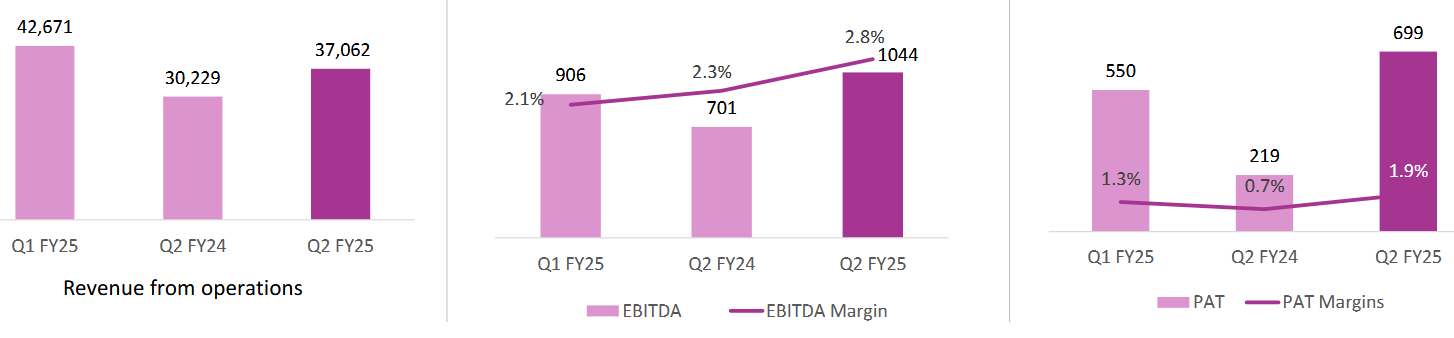

4. Q2-25: PAT up 219% & Revenue up 23% YoY

5. H1-25: PAT up 64% & Revenue up 46% YoY

6. Business metrics: Improving return ratios

we would like to assure that we keep on continuing our focus on ROCE and ROE rather than transaction wise EBITDA margin.

7. Outlook: 20% Revenue CAGR

Growth and Revenue:

Has historically demonstrated a CAGR of around 20% over the last 20 years. They have been able to maintain or overachieve this target to date.

While Q1 saw a growth of 74%, Q2 growth was 22%. The management acknowledges that the business is subject to volatility on a quarter-on-quarter basis.

The company is confident of achieving a double-digit growth rate in the coming months and year, excluding large project orders.

The company's enterprise business is experiencing substantial double-digit growth and is in line with the company's plan.

Margins:

EBITDA margins to be in the range of 2.5% to 3%.

EBITDA margin fluctuations are influenced by sales mix and the execution of larger deals, which may involve some discounts.

Management is focused on Return on Capital Employed (ROCE) and Return on Equity (ROE) rather than transaction-wise EBITDA margin.

Improvements in PAT margins a result of efficient volumes & interest benefits

Margins in the IT distribution industry are maturely defined, limiting significant variations.

Potential for margin improvements through economies of scale as the top line grows and bulk deals with lower operational costs are executed.

Data Center and AI:

Well-positioned to benefit from increasing demand for data centers in India.

Rashi Peripherals has a first-mover advantage in the AI space, being a leading distributor for NVIDIA, ASUS, and Lenovo, all of whom play a significant role in servers, storage, and GPUs.

Rashi Peripherals supplied servers for the first large AI data center set up by Yotta NMDC.

The company expects to see growth in sales of AI-enabled laptops, with projections of 30-35% of laptops and desktops being AI-enabled in three years.

The company is also anticipating a potential opportunity from a government tender for 10,000 GPUs.

Seasonality:

Q2 and Q4 typically compete to be the highest revenue quarters of the year. Q2 is a consumer-driven quarter, while Q4 is more commercial.

Q3 is typically the lowest quarter of the year.

September is the highest month of the year for online channel sales.

8. PAT growth of 64% & Revenue growth of 46% in H1-25 at a PE of 14

9. Hold?

If I hold the stock then one may continue holding on to RPTECH.

Based on H1-25 performance one can look forward to a strong FY25 providing a reason to continue with RPTECH.

RPTECH has given a EBITDA guidance of 2.5-3%. H1-25 EBITDA margin was at 2.5%. One needs to keep track that the margin does not fall below 2.5%

RPTECH is in the middle of a strong run and has delivered 4 consecutive quarters of PAT growth starting Q3-24. Q3 is the slowest quarter and hence we have an understanding of what to expect in Q3-25. Barring seasonality, one can hold on as long as the underlying business momentum is strong.

RPTECH has a track record of delivering around 20% revenue growth over the long term which gives insight into the strong execution of the management.

10. Buy?

If I am looking to enter RPTECH then

RPTECH has delivered PAT growth of 64% & Revenue growth of 46% in H1-25 at a PE of 18 which makes valuations quite attractive in the short term.

RPTECH has a long term track record of growing revenue at about 20% CAGR at a PE of 18 makes valuations look attractive from a longer term.

RPTECH has a net-worth of 1,660.7 cr as of H1-25 end and is available at a market cap of Rs 2495 cr. RPTECH is available at a price to book of 1.5 which makes valuations quite reasonable.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer