Ramkrishna Forgings: PAT growth of 38% & revenue growth of 24% in FY24 at a PE of 34

Revenue growth of 18-30% in FY25. Revenue CAGR of 19-24% for FY24-26. Outlook of 15-20% volume growth till FY26. Order book & capex in place to support revenue growth till FY26

1. 2nd largest forging player in India

ramkrishnaforgings.com | NSE: RKFORGE

Product Portfolio

2. FY20-24: PAT CAGR of 144% & Revenue CAGR of 34%

3. FY23: PAT up 25% & Revenue up 38%

4. Strong 9M-24: PAT up 38% & Revenue up 27% YoY

5. Strong Q4-24: PAT up 37% & Revenue up 15% YoY

6. Strong FY24: PAT up 38% & Revenue up 24% YoY

7. Business metrics: Strong return ratios

8. Strong outlook: Growth CAGR of 19-24%

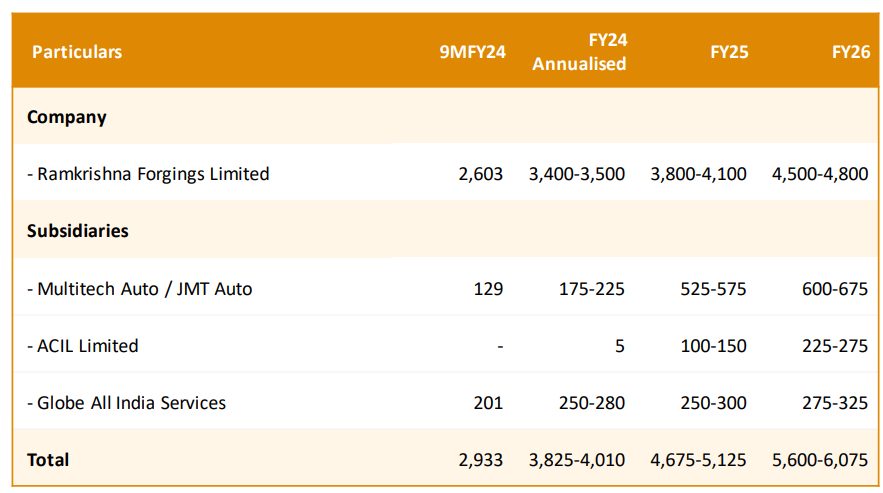

i. Revenue CAGR of 19-24% for FY24-26

Revenue growing to Rs 5,600-6,075 cr in FY26 from Rs 3,955 cr in FY24 implies a revenue CAGR of 19-24%. Revenue growth of 18-30% in FY25

we are looking at 15% to 20% volume growth in terms of our consolidated numbers.

ii. EBITDA margin expansion to 25% from 22%+

if you see constantly for 16 quarters, we have been maintaining a margin of 22% and above and I think very slowly but steadily we are working towards our goal of 25%

I can very safely say that we aspire to be 25% plus EBITDA margin making Company, while we will be able to safely maintain the current margin trajectory going forward.

iii. Orderbook with capacity expansion to support revenue guidance

9. PAT growth of 38% & Revenue growth of 24% in FY24 at a PE of 34

10. So Wait and Watch

If I hold the stock then one may continue holding on to RKFORGE

Coverage of RKFORGE was initiated after Q3-24 results. The investment thesis has not changed after a strong FY24. It has increased the confidence in the management to deliver a stronger FY25 given the outlook for 19-30% revenue growth guidance.

RKFORGE is in the middle of a strong run and has delivered sequential QoQ growth in top-line & bottom line in all the four quarters of FY24

The roadmap of 19-24% revenue growth till FY26 provides a reason to continue with RKFORGE

11. Join the ride

If I am looking to enter RKFORGE then

RKFORGE has delivered PAT growth of 38% and revenue growth of 24% in FY24 at a PE of 34 which makes the valuations fairly valued in the short term.

The long term past track record of FY20-24 PAT CAGR of 155% & Revenue CAGR of 32% makes the valuations at a PE of 32 quite reasonable from a performance perspective

With a revenue growth outlook of 19-24% and EBITDA margin expansion from 22% to 25% provides opportunities in RKFORGE over the longer term as one can expect for 20%+ earnings growth over the long term.

One may see limited opportunities in RKFORGE in the short-term at a PE of 32. Additionally one can see a reaction in case of a weak quarter given that the PE is 30+

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer