Prakash Pipes: PAT up 38% & Revenue up 17% in Q1-25 at a PE of 15

Industry tailwinds providing strong demand with stable raw material prices. PPL is delivering margin expansion and available at reasonable valuations. Lack of management commentary is a challenge

1. Why is PPL interesting

prakashplastics.in | NSE: PPL

PPL is executing efficiently on the industry tailwinds which are generating strong demand with stable raw material prices. PPL is delivering margin expansion and available at reasonable valuations both on a PE and free cash flow yield perspective.2. PVC Pipes & Fittings & Flexible Packaging Manufacturer

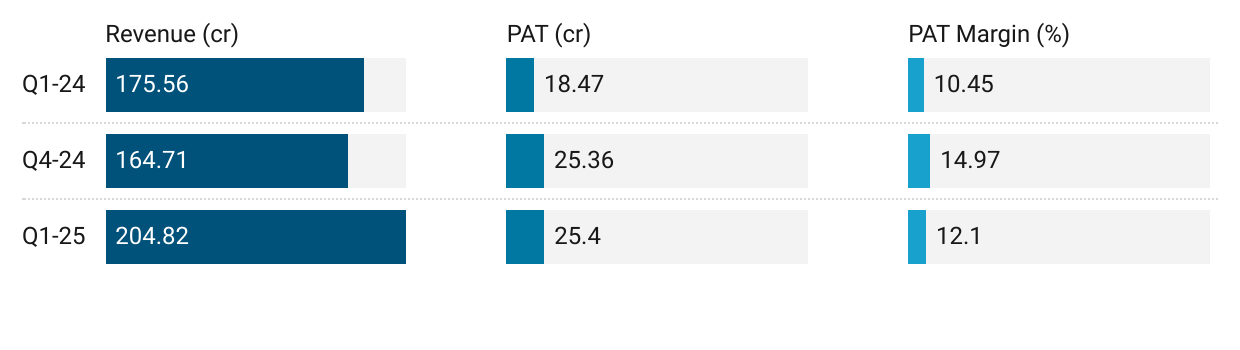

3. FY20-24: PAT CAGR of 38% & Revenue CAGR of 15%

4. FY24: PAT up 26% & Revenue down 6%

5. Strong Q1-25: PAT up 38% & Revenue up 17% YoY

PAT was marginally up & Revenue up 24% QoQ

6. Business metrics: Strong return ratios

7. Strong outlook

i. Strong growth in flexible packaging segment

we anticipate strong growth in our flexible packaging segment, alongside steady expansion in PVC Pipes and Fittings

ii. Capex to support future growth

PVC Pipes & Fittings: We are entering the next phase of expansion by adding CPVC and UPVC injection moulding machines to increase our production capabilities. Additionally, we are introducing a new product line for HDPE drums, which is crucial for the pharmaceutical, chemical, and food processing industries.

Flexible Packaging: We are expanding our capacities to 36,000 MT over the next two years, focusing on extrusion-coated and laminated structures. Significant investments are being made in high-output, high-performance machinery to meet the growing demand and set new industry benchmarks.

8. PAT growth of 38% & Revenue growth of 17% in Q1-25 at a PE of 15

9. Do I stay?

If I hold the stock then one may continue holding on to PPL

Based on Q1-25 performance, PPL looks on track to deliver as per the momentum seen during the last 5 years.

PPL is in the middle of a strong run and it has sequentially grown its PAT on QoQ basis for the last 7 consecutive quarters starting Q3-23. One can keep ride this business momentum till it lasts

PPL planning for capex in both PVC Pipes & Fittings and Flexible Packaging indicating the management is confident of the demand outlook in the coming years

PPL is executing efficiently on the demand of end-user industries and riding the industry tailwinds

Robust demand, driven primarily by key end-user industries such as irrigation, water supply, sanitation, and housing, which together account for over 80% of the total demand, has been the main catalyst for increased capital expenditure (capex) by PVC pipe manufacturers both this fiscal year and the next.

Healthy volume growth, combined with stable PVC resin prices—which constitute 70-75% of total costs—will enhance operating leverage and improve profitability by 100-150 basis points

Packaging industry in India is experiencing significant growth, driven by the adoption of innovative packaging technologies and the expanding flexible packaging market. The industry is poised to witness significant volume growth in upcoming years.

10. Do I enter?

If I am looking to enter PPL then

PPL has delivered PAT growth of 38% and revenue growth of 17% in Q1-25 at a PE of 15 which makes the valuations quite reasonable in the short term.

PPL on a current market cap of Rs 1,469 cr generated free cash flow of Rs 100.5 cr in FY24 which implies that its available at a FY24 free cash flow yield of 6.8% which makes the valuations quite attractive.

The lack of any management commentary or public information is the biggest problem one faces in taking a call on PPL. However, a PE of 16, and an attractive free cash yields provides some safety in terms of valuations.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer