Power Finance Corp: PAT growth of 17% & Net Interest Income growth of 21% in 9M-25 at a PE of 6

AUM growth of 12-14%, PAT growth of 15%+ at attractive price to book makes PFC a mix of value, growth & dividend yield. Strong tailwinds of renewable energy, smart metering & grid modernization

1. NBFC focused on Power Finance

pfcindia.com | NSE: PFC

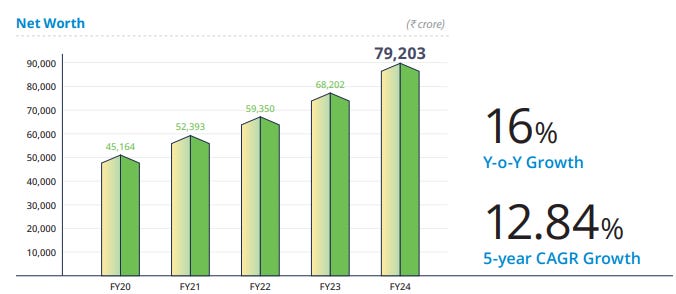

2. FY20-24: PAT CAGR of 16% & Revenue CAGR of 10%

3. FY24: PAT up 25% & Net Interest Income up 9% YoY

4. Q3-25: PAT up 23% & Net Interest Income up 16% YoY

5. 9M-25: PAT up 17% & Net Interest Income up 21% YoY

6. Business metrics: Strong return ratios

7. Outlook: AUM Growth of 12-14%

Growth Guidance

AUM Growth: Management expects to maintain 12–14% year-on-year loan book growth, similar to the previous year.

Loan Disbursements: Q4 disbursements are expected to be stronger, in line with historical patterns where ~37% of yearly disbursements occur in Q4.

Key Growth Drivers:

Distribution Sector: Largest disbursement focus (~60% share).

Renewables: Strong momentum with 28% YoY loan book growth; ₹69,423 crore as of Dec 2024.

Conventional Generation: Some activity; select sanctioned projects underway.

Revamped Distribution Sector Scheme (RDSS): Execution expected to pick up as 94% of sanctioned work and 90% of smart metering projects have been awarded.

Profitability Outlook

Net Interest Margins (NIM): Expected to remain stable despite portfolio shift toward renewables (which typically have slightly lower spreads).

FY25 YTD NIM: 3.65%.

Yield on Earning Assets: 10.07%, with cost of funds at 7.47%, maintaining a healthy spread of 2.60%.

Asset Quality & Resolution Guidance

Gross NPA Ratio: Expected to decline further to ~2%, pending resolution of key assets.

Currently at 2.68% standalone; 2.30% consolidated.

Key Resolutions in Pipeline (₹4,961 crore total):

KSK Mahanadi (₹3,300 crore): Resolution plan filed with NCLT; more than 100% recovery expected.

Shiga Energy (₹522 crore) and TRN Energy (₹1,139 crore): Resolutions pursued outside NCLT; likely to close in Q4 FY25.

Provisioning: 73% on Stage III assets; potential for provision reversals upon resolution.

Risks

Forex Exposure Management: 5% of foreign currency debt is unhedged.

Impact of 1 INR depreciation ≈ ₹45 crore loss; total Q4 impact estimated around ₹400–500 crore if INR hits 88.

8. PAT growth of 17% & Net Interest Income growth of 21% in 9M-25 at a PE of 6

9. Hold?

If I hold the stock then one may continue holding on to PFC.

Based on 9M-25 performance one can look forward to PFC delivering FY25 in-line with its 12-14% AUM growth guidance.

PFC is indication to a strong Q4-25 following a strong 9M-25.

If you see the last year trend, 37% of our total disbursement is happening in the Q4. So on that basis, we are expecting that we will be able to maintain our guidance, which we have given for the loan growth.

We have in pipeline good disbursement planned out for the current quarter for the financial year FY '25. So we are quite hopeful that this quarter also, we are going to have a disbursement on distribution as well as on the renewable side.

Things to watch out for closely in PFC

NCLT resolution timing: Delay in KSK Mahanadi or others could delay profit reversals.

RDSS execution: Disbursement ramp-up in Q4 is critical to meet growth targets.

Renewables risk: Delays in PPAs or state DISCOM pressure could hit future growth.

Forex volatility: INR depreciation beyond ₹88 could significantly dent Q4 earnings.

10. Buy?

If I am looking to enter PFC then

PFC has delivered PAT growth of 17% & Net Interest Income growth of 21% in 9M-25 at a PE of 6 which makes valuations reasonable in the short term.

PFC is guiding for 12-14% revenue CAGR which at a PE of 6 which makes valuations attractive over the longer term.

AUM Growth: For the current financial year, we are expecting that we will be able to maintain the similar level as was done in the previous year.

PFC had a consolidated net worth of Rs 1,51,338 cr as of Q3-25 end and is available at market cap of Rs cr. PFC is at a price to book of 0.8 which makes valuations quite attractive.

On a standalone basis PFC has a track record of growing its net-worth at a 5 year CAGR of 13%. If the business momentum continues then on a current standalone price to book of 1.5 makes valuations quite attractive.

Standalone Book Value Per Share Rs.267.76

PFC is not to be seen as a “momentum” stock. Price may move slowly even with good news. However, if resolution of key stressed assets (like KSK Mahanadi) materializes in Q4, and forex volatility stays contained, the stock has rerating potential

Dividend + Growth Play: PFC offers a strong dividend yield while growing AUM by 12–14% annually, and earnings by 15%+ a rare combo in PSU NBFC space.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

It's definitely a great company, the dividend was 15.75 in FY 25-26, and 15.50 in FY24-25. historically increased it 4% yoy. A great stock!