Piramal Finance FY26 Results: PAT up 210%, Solid FY27 Guidance

PAT of 50% with AUM growth of 25% in FY27. Post FY26 result & FY27 guidance, potential of re-rating. Trading at attractive valuations with a margin of safety

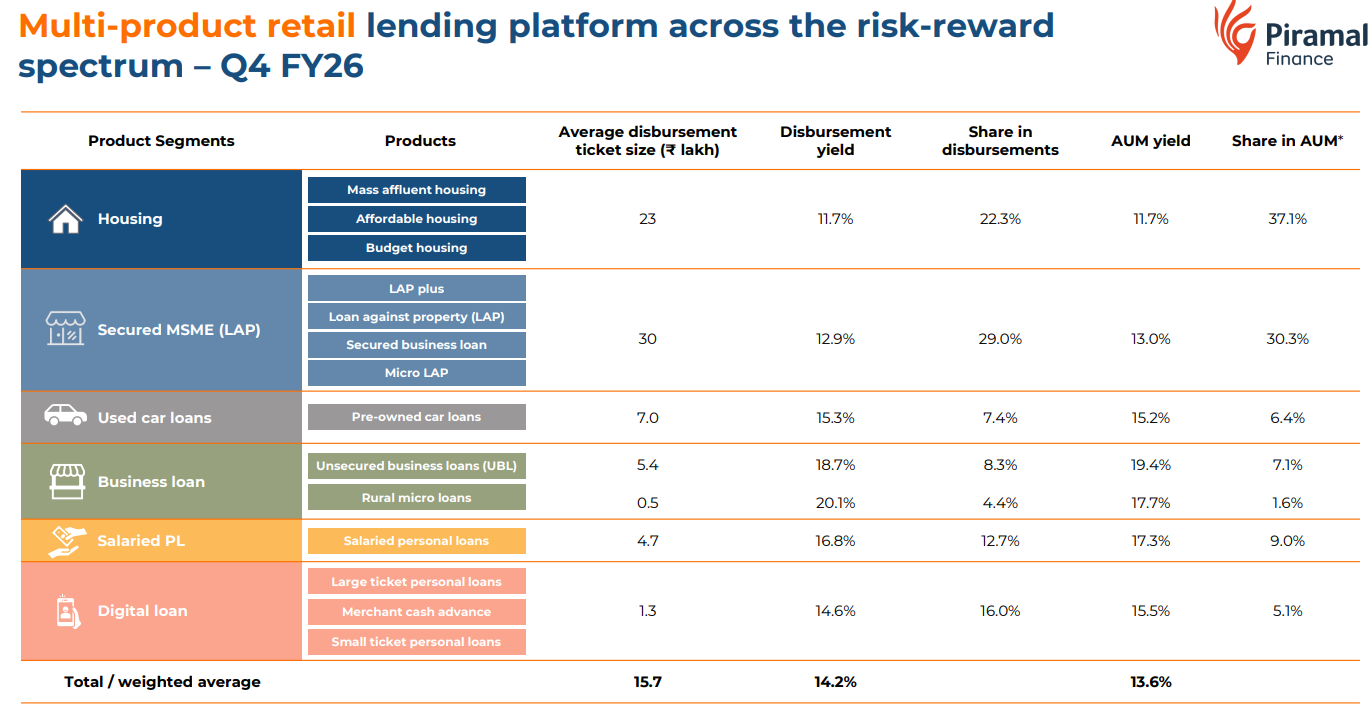

1. Retail Focussed NBFC

piramalfinance.com | NSE: PIRAMALFIN

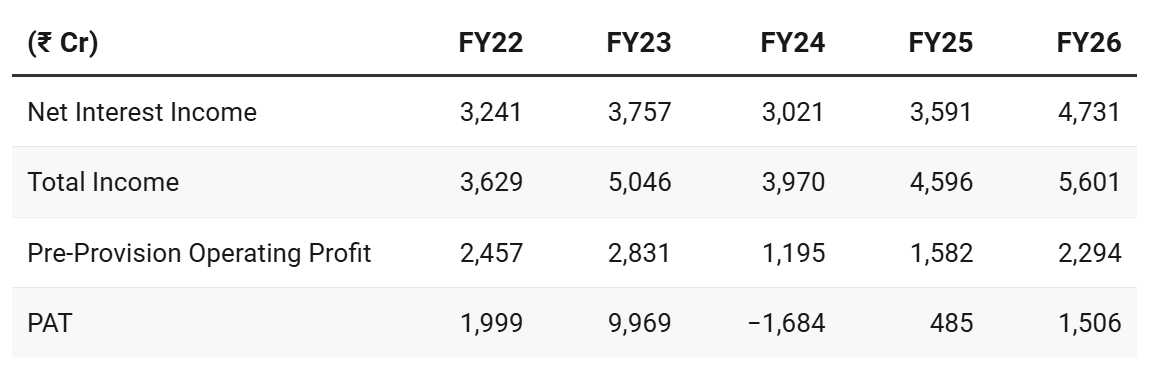

2. FY22-26: A period of transition

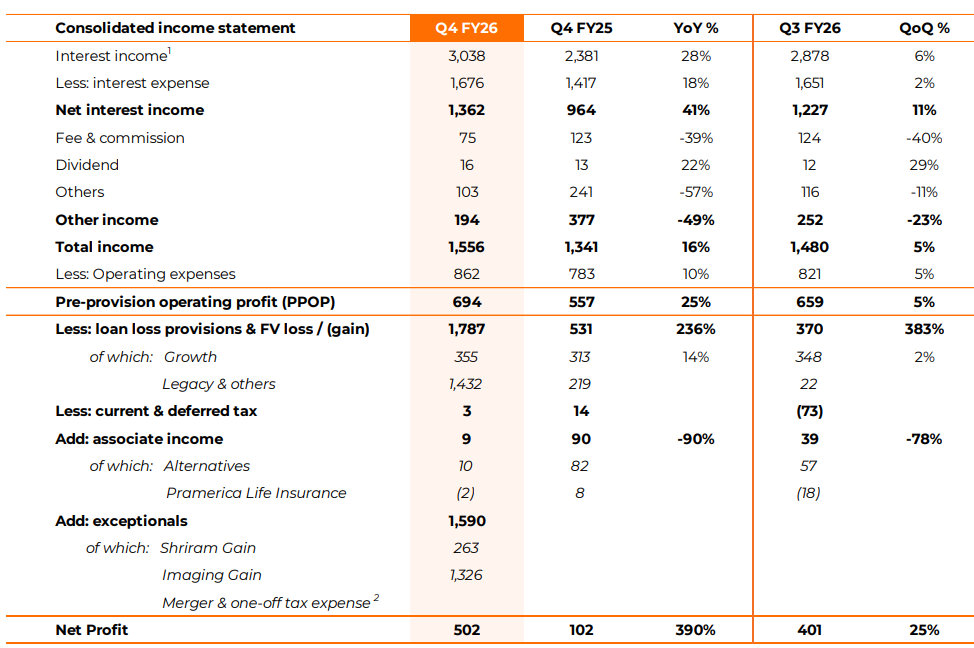

3. Q4-26: PAT up 390% & Net Interest Income up 41% YoY

PAT up 25% & Net Interest Income up 11% QoQ

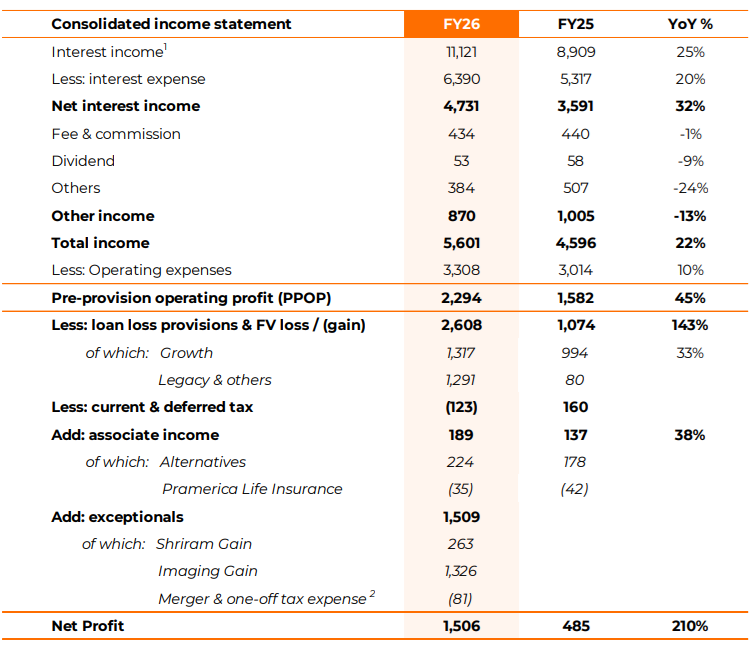

4. FY26: PAT up 210% & Net Interest Income up 32% YoY

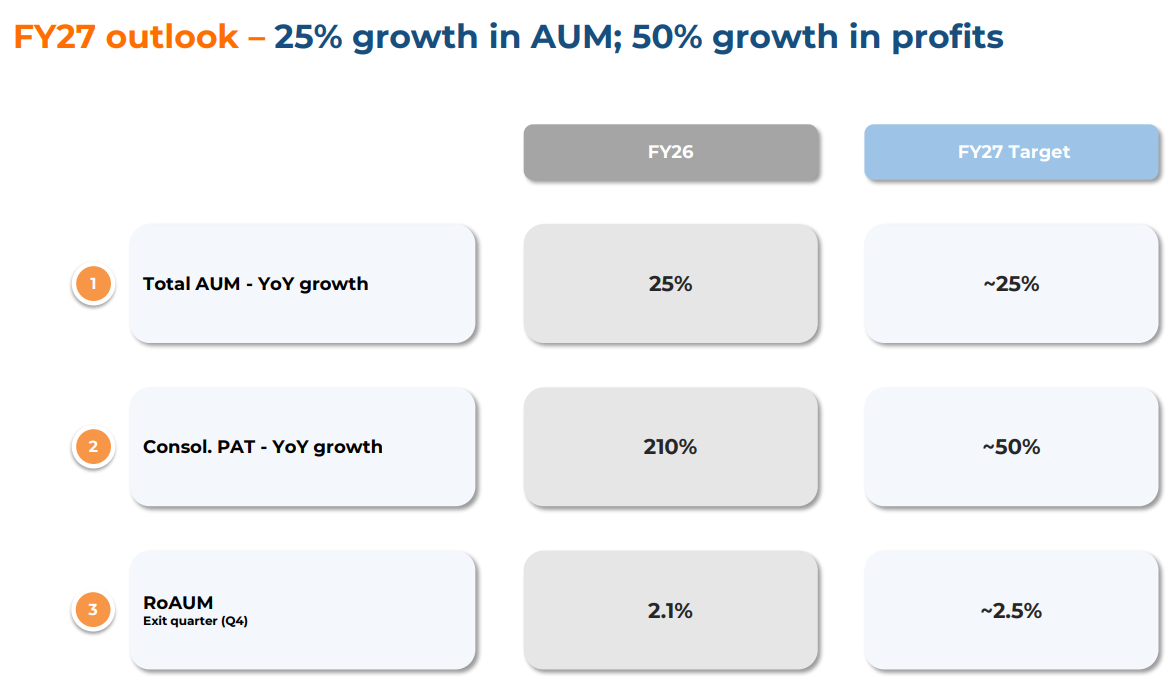

5. Outlook: 25% AUM Growth; 50% PAT growth

5.1 Management Guidance and Outlook

Bottom-line growth driven by improving profitability

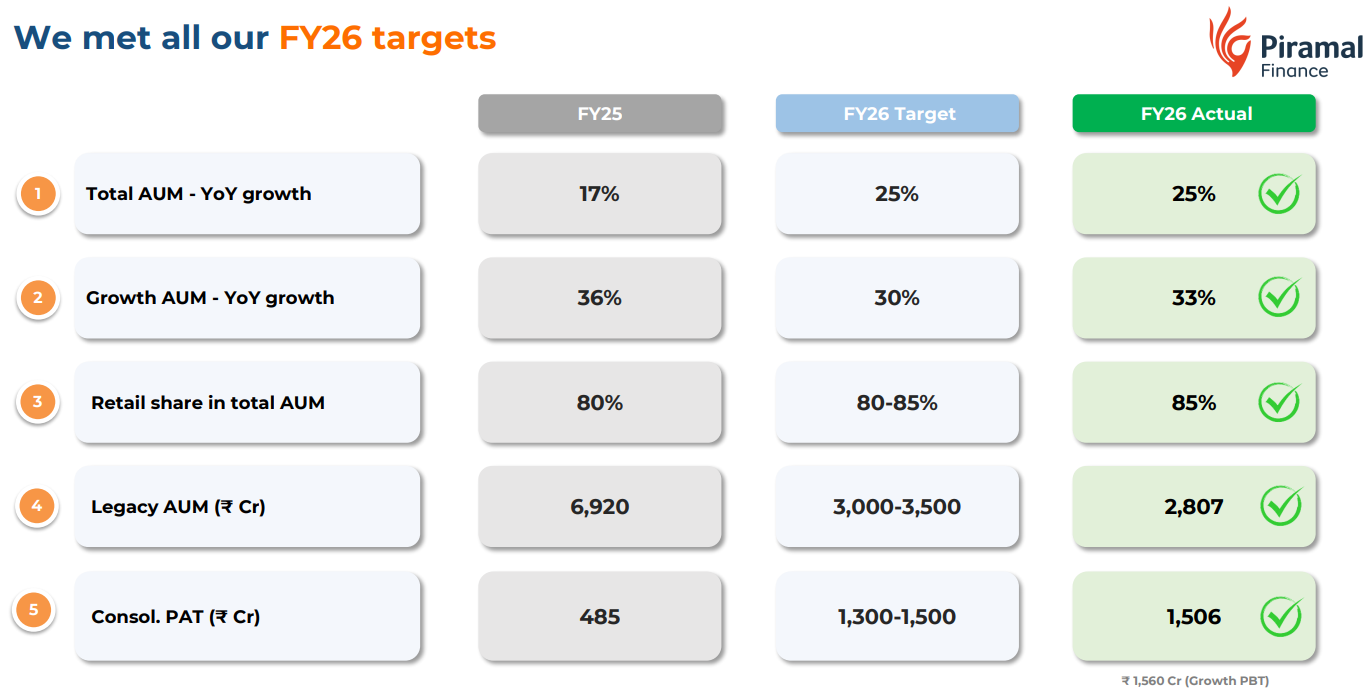

5.2 FY26 Performance vs FY26 Guidance

No complaints — FY26 guidance delivered

6. Valuation Analysis

6.1 Valuation Snapshot — Piramal Finance

Current Market Price — ₹1,837.9

Market cap — ₹41,537 Cr

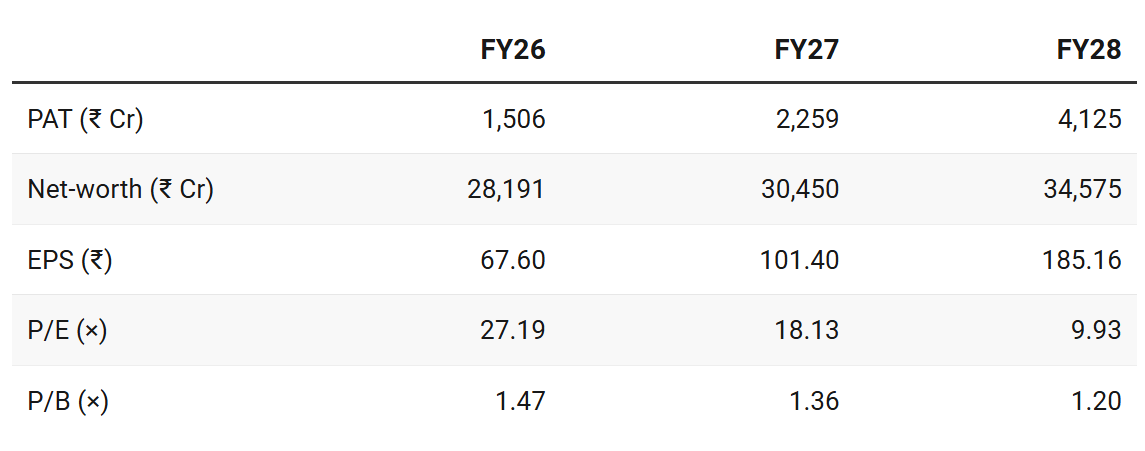

FY27 PAT = 1.5 X FY26 PAT

FY28 PAT =3% X average(FY26 AUM, FY27 AUM)

Despite profitability improving, PIRAMALFIN still trades at 1.2 P/B (×) on FY28 estimates.

For a company guiding to deliver ~66% PAT CAGR for FY26-28 — the P/B multiple deserves a re-rating closer to 2 P/B (×)

6.2 Opportunity at Current Valuation

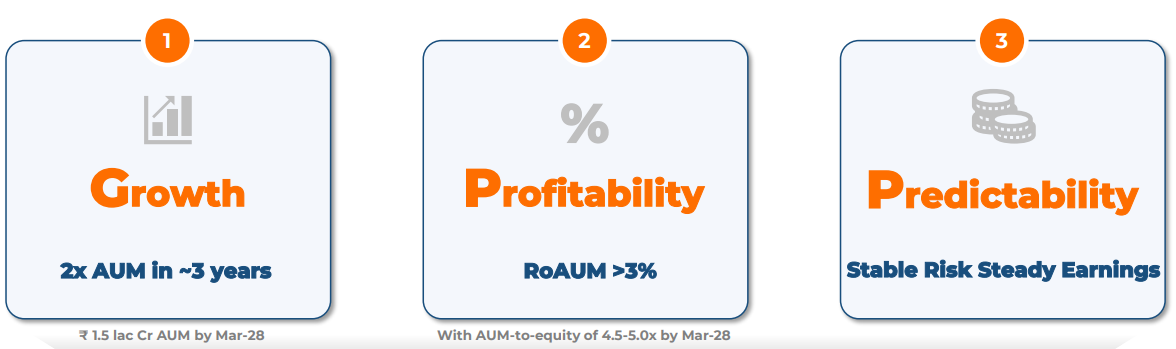

Increased Profitability: RoA improving from 2.1%(Q$ FY26 exit) to 2.5% in FY27 to 3% by FY28 creates the opportunity as bottom-line grows faster than the top-line

AUM growth: 22% AUM CAGR FY26-28 to support bottom-line growth

Margin of safety: Even at a current P/B of 1.47(×) there exists a margin of safety in the perspective of the guidance for FY27 and FY28.

Projections not discounted: Weak past record in the last 5 years — market does not fully discount the growth projection of FY28

Deferred Tax Asset on books: A deferred tax asset reduces future tax payments

When Piramal earns profits it won’t pay full tax. Instead it will use past losses to offset profits

This will lead to higher future PAT & cash flows

The impact of DTA against tax losses: ~₹2,100 Cr is not fully discounted

Optionality of total assessed tax losses is not fully discounted

Total assessed tax losses= ~₹24,600 Cr ==> @25% tax rate = DTA of ~₹6,150 Cr (of which only ~₹2,100 Cr is recognized)

Added ₹10,110 Cr in assessed tax losses taking total assessed tax losses to ~₹24,600 Cr (o/s DTA against tax losses: ~₹2,100 Cr)

Multiple Re-rating: Opportunity of being re-rated at around 2(×) P/B if FY27 guidance is delivered and PIRAMALFIN shows progress on executing FY28 guidance.

6.3 Risk at Current Valuation

Despite the visible turnaround, key risks remain:

Execution Risk: PIRAMALFIN is on-track to deliver FY26 guidance. The challenge is to consistently deliver on the FY28 guidance.

Residual legacy risk: ~₹2,807 Cr of legacy AUM still sits on the book; impairment or recovery delays could drag performance.

Asset quality while improving needs to be watched

Previous coverage on PIRAMALFIN

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer