PG Electroplast: PAT growth of 77% & revenue growth of 27% in Q1-25 at a PE of 64

Guidance for PAT growth of 58% & Revenue growth of 33% with improvement in margin in FY25. Orders in place to support the growth for FY25

1. Electronic Manufacturing Services provider

pgel.in | NSE: PGEL

2. FY20-24: PAT CAGR of 169% & Revenue CAGR of 44%

3. Average FY24: PAT up 77% & Revenue up 27% YoY

4. Strong Q1-25: PAT up 151% & Revenue up 95% YoY

5. Business metrics: Strong & improving return ratios

6. Outlook: PAT growth of 58% & Revenue growth of 33%

i. Revenue growth of 33%

ii. PAT growth of 58%

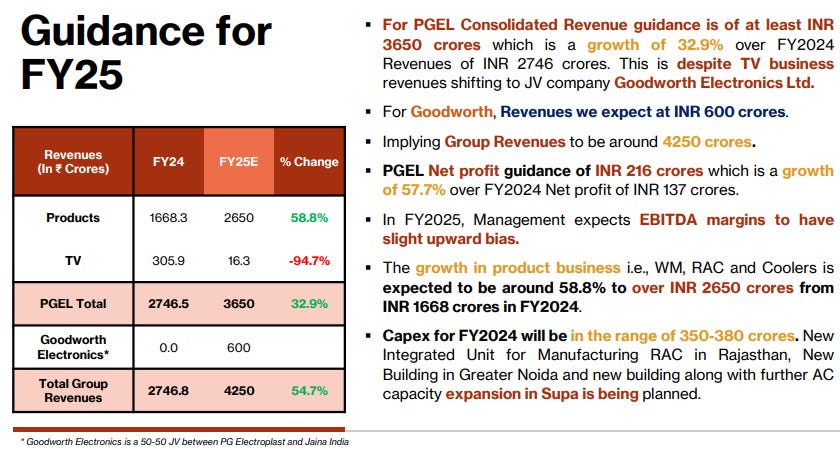

PGEL Net profit guidance of INR 216 crores which is a growth of 57.7% over FY2024 Net profit of INR 137 crores.

iii. Improvement in margins

In FY2025, Management expects EBITDA margins to have slight upward bias.

7. PAT growth of 151% & revenue growth of 95% in Q1-25 at a PE of 64

8. So Wait and Watch

If I hold the stock then one may continue holding on to PGEL

PGEL has a track record of growth, with a revenue CAGR of 30%+ for FY16-24, followed by an extremely strong quarter in Q1-25.

The management is bullish about its prospects in FY25 as it has revised its guidance upwards after a strong Q1-25.

Order book is in place to support the growth guidance for FY25

Order book for product business remains robust and the company hopes to scale product business significantly in FY2025

9. Or, join the ride

If I am looking to enter PGEL then

PGEL has delivered PAT growth of 151% & Revenue growth of 95% in Q1-25 at a PE of 64 which makes valuations acceptable in the short term.

The FY25 outlook for guiding for PAT growth of 58% & Revenue growth of 33% with improvement in margin and the support of strong order book at a PE of 64 makes the valuation reasonable from the medium term

While no quantitative numbers are given by PGEL, it is pointing towards a story which would continue beyond FY25. At a PE of 64 there would be opportunity over the longer term if the past performance is repeated.

The Management is enthused about the overall opportunity size and anticipates high growth rates in the industry segments where, company has presence.

Company is uniquely positioned in the consumer durable & plastics space in India and would derive higher revenue growth by growing its market share in the customer outsourcing wallet.

Company’s management see exciting times ahead for all its business segments.

Previous Coverage of PGEL

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer