Oriental Rail Q3 FY26 Results: PAT Up 84%, Strong Growth Guidance

Guidance of 25% revenue CAGR with margin expansion for FY25-28. After a strong 9M FY26 the forward guidance is not discounted - trading at attractive valuation

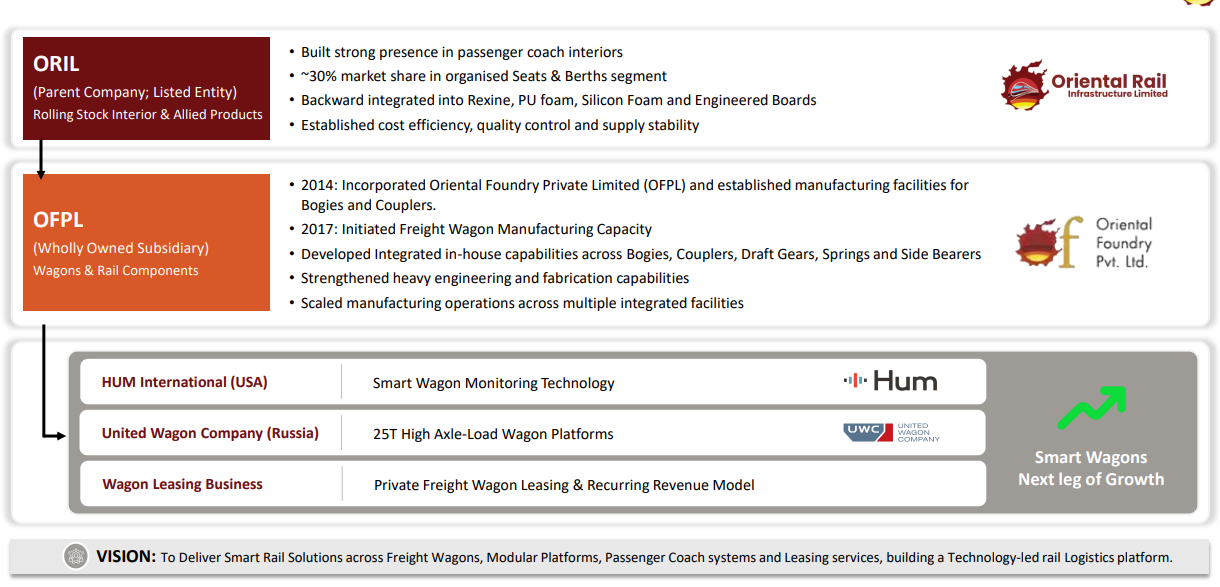

1. Coach Interiors + Wagon & Rail Components

orientalrail.com | BSE: 531859

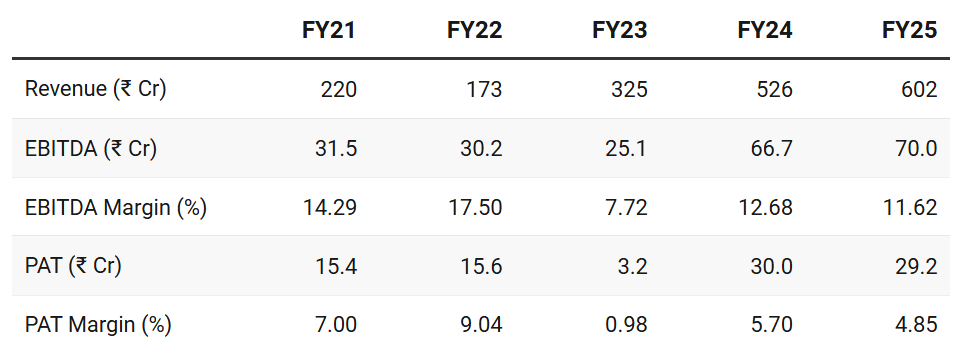

2. FY21–25: PAT CAGR of 17% & Revenue CAGR of 29%

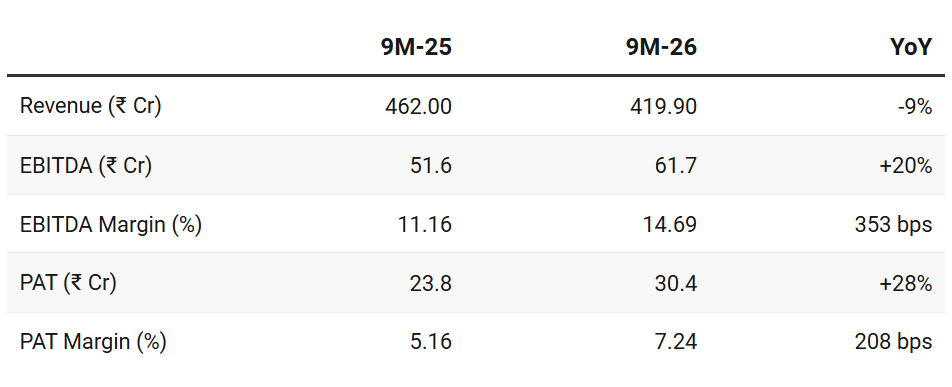

Average performance - nothing spectacular in the past

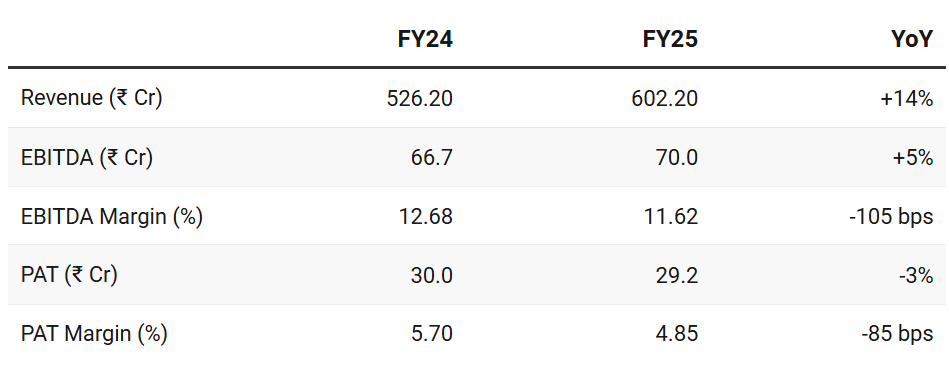

3. Weak FY25: PAT down 3% & Revenue up 14%

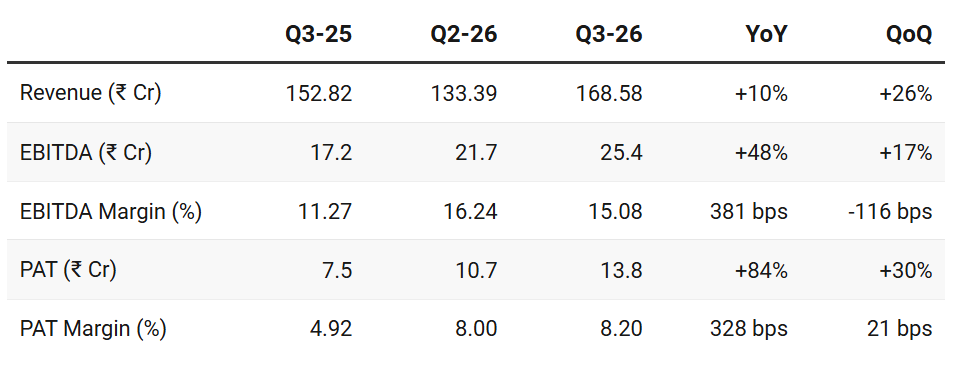

4. Strong Q3-26: PAT up 84% & Revenue up 10% YoY

PAT up 30% & Revenue up 26% QoQ

Q3FY26 revenue grew by 10.3% YoY on improved execution

EBITDA margins expanded by 381 bps in Q3 supported by better product mix and operating leverage.

5. 9M-26: PAT up 28% & Revenue down 9% YoY

9MFY26 revenue declined by 9% YoY due to order driven revenue recognition, dispatch timing and temporary wheel supply constraints.

EBITDA margins expanded in 9M, supported by better product mix and operating leverage.

PAT margins improved by 328 bps in Q3 and 207 bps in 9M, driven by stronger operating performance and improved cost absorption.

Order book stands at Rs 1,960 Cr comprising Rs 1,779 Cr for OFPL and Rs 181 Cr for ORIL, providing strong revenue visibility

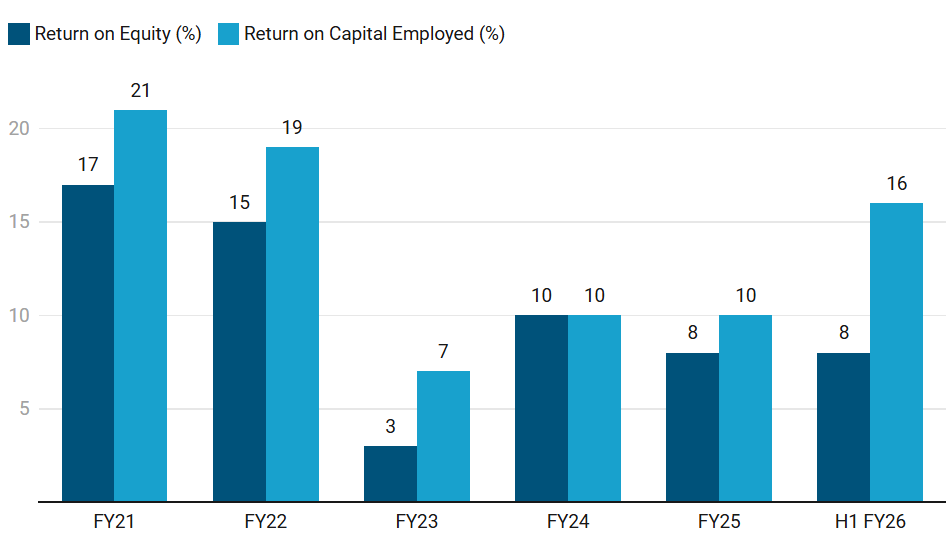

6. Return Metrics: Average Return Ratios

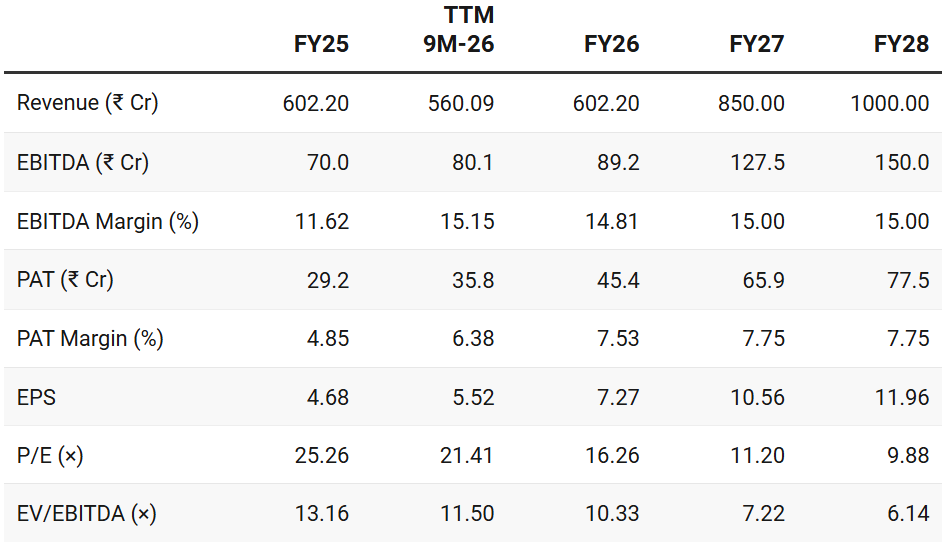

7. Outlook: 25% Revenue CAGR for FY25-28

7.1 Management Guidance

Guidance for strong growth in FY27 and FY28 — strong turnaround from a flattish FY26

Revenue Growth

FY27: Revenue of ₹850 Cr.

FY28: Revenue of ₹1,000 Cr.

Revenue guidance for FY27 is conservative as it only includes the legacy seat interior and wagon manufacturing businesses; it does not yet account for potential revenue from the new ”smart wagon” technology

While past-performance has not been spectacular — the strong order book provides revenue visibility and confidence that the FY27 and FY28 guidance is realistic

7. Valuation Analysis — Oriental Rail Infrastructure

7.1 Valuation Snapshot

Current Market Price: ₹118.2; Market Cap: ₹793 Cr

Very attractive from the perspective of forward valuations — given the strong tailwinds supporting governmental spend in railway infrastructure

Orient Rail Infrastructure generated ₹28.5 Cr in H1 FY26. At current market cap of ₹793 Cr, its trading a free cash flow yield of 3.6% (not annualized) which makes it quite attractive from a current valuation perspective

Suggests limited room for further multiple expansion in the near term

The opportunity emerges over the longer term beyond FY27

7.2 Opportunity at Current Valuation

The guidance is not in the price

A company growing to ₹1,000 cr with 25% CAGR and 15% EBITDA margin is available at a FY28 P/E of 10x and EV/EBITDA of 6x

Opportunity of re-rating in multiples a realistic re-rating to a PE of 15x for FY28 creates significant opportunity in the stock.

Management has re-iterated that the guidance of ₹850 cr is conservative

Freight Wagons & Wagon Components

50% Capacity Utilisation: Significant headroom to scale wagon production and capture rising procurement demand.

Smart & Modular Wagon Platforms: Leveraging technology partnerships to develop advanced wagon solutions and unlock new revenue streams.

Wagon Leasing Platform: Entering wagon leasing to capitalise on growing private freight demand and build recurring logistics revenues.

Rolling Stock Interior & Allied Products

Interior Systems and Seats & Berths: Growing new train additions and passenger coach modernisation to drive sustained demand.

ORVIN® (Artificial Leather): Strong revenue growth supported by expanding industrial applications.

Backward Integration: Continued focus to enhance cost efficiencies, margin resilience and supply chain control

Strategic Technology Partnerships

Smart Wagon Systems (Hum International, USA): The company has a tie-up to introduce sensors and algorithms that predict bearing and wheel failures up to 50,000 kilometers in advance.

Market Opportunity: Management estimates the total market scope for this safety technology in India to be approximately INR 100,000 million.

Tender Status: A pilot tender for 400 wagons is opening on March 26 to prove the concept.

High-Capacity Wagons (United Wagon, Russia): A collaboration to develop next-generation 25-ton high-axle load wagons. This technology is expected to increase carrying capacity from the current 80 tons to approximately 82–83 tons per wagon.

7.3 Risk at Current Valuation

Risk associated with tender based business: Oriental Rail receives majority orders from Indian railways based on tender.

Revenue depends on the company’s ability to win tenders.

Profitability margins come under pressure because of this competitive and tender-based industry.

This risk is seen in the past performance of Oriental Rail given that revenue wins are lumpy

The primary customer of Oriental Rail is the Indian Railways

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer