Northern ARC Capital: Q1-25 Earnings Call Highlights

Strong performance, highlighting resilient business model, risk management, & technological capabilities. Despite challenges in microfinance, remains optimistic about growth & profitability

northernarc.com | NSE: NORTHARC

1. Key Takeaways

1.1 TLDR

Successful IPO and Listing: Northern Arc celebrated its successful listing on both NSE and BSE on September 24th, 2024.

Northern Arc Capital Limited reported a strong Q1FY25 performance, highlighting its resilient business model, robust risk management, and technological capabilities.

Despite ongoing challenges in the microfinance sector, the company remains optimistic about its future growth and profitability prospects.

1.2 Strong Q1FY25 Performance:

AUM reached INR 11,869 crores, representing a 32% year-on-year growth.

Net revenue reached INR 297 crores, reflecting a 40% year-on-year growth.

Stable cost of borrowing at 9.3%.

Robust growth in pre-provisioning operating profit (PPoP) at 43% year-on-year.

Strong asset quality with a GNPA of 0.47% and a net NPA of 0.12%.

Achieved the most profitable quarter to date with a PAT of INR 93 crores, representing a 43% year-on-year increase.

1.3 Outlook

Continued focus on growth in line with the company's historical 30%+ CAGR.

Northern Arc expects their balance sheet to grow faster than the industry growth rate.

Credit costs are anticipated to remain consistent.

The company is cautious about potential macroeconomic impacts on borrower repayment.

The infusion of INR 500 crores in primary capital through the IPO will provide further momentum for growth and profitability.

2. Key Themes & Discussion Points

2.1 Microfinance Sector Challenges:

The microfinance sector is experiencing stress due to over-leveraging at the borrower level following regulatory changes in October 2022, including the removal of the interest rate cap and restrictions on the number of microfinance loans an individual could hold. Northern Arc is mitigating risk through:

Deep domain expertise and robust risk models.

Ground-level insights through physical branch visits.

Proactive portfolio management and credit selection.

"We actually touch 35% of the network where our portfolio is spread by physically going and meeting in the deep rural areas which we select on a pretty scientific basis to cover 35% of our portfolio." - Ashish Mehrotra, MD & CEO

2.2 Diversification as a Strength:

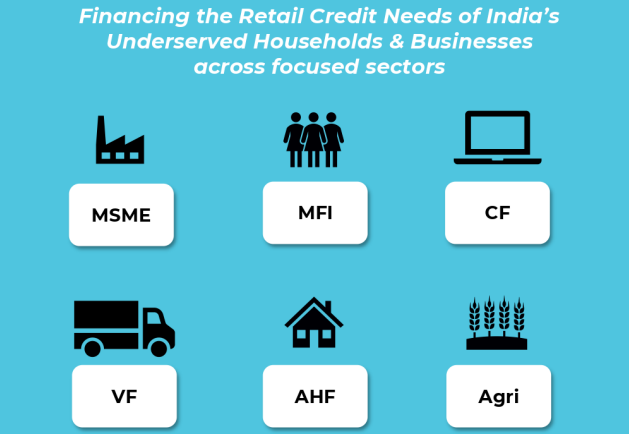

Focus Sectors: Northern Arc focuses on six key sectors: MSME, Microfinance, Consumer Finance, Vehicle Finance, Affordable Housing, and Agricultural Supply Chain.

Northern Arc emphasized the importance of their diversified portfolio across six sectors, enabling them to adjust exposure based on market dynamics and maintain a consistent performance.

"The power of diversification allows you to dial up and dial down looking at the headwinds and tailwinds." - Ashish Mehrotra

2.3 Strong Liability Franchise:

Northern Arc boasts a diversified funding profile with strong relationships with lenders and investors, proactive liquidity management, and strong credit ratings (upgraded to AA- by ICRA & India Ratings).

Northern Arc has established a diversified and robust liability franchise, with a significant portion of borrowings coming from DFIs, both domestic and global multilateral. This strong franchise, coupled with proactive treasury management, has allowed them to maintain a stable cost of borrowing.

"We have been able to grow the share of the offshore route to 28%." - Atul Tibrewal, CFO

2.4 Positive Outlook for Growth and Profitability:

Northern Arc expressed confidence in its ability to sustain its growth trajectory and profitability, supported by its diversified portfolio, strong risk management, technology capabilities, and the recent infusion of capital through the IPO.

Northern Arc Capital Limited Q1FY25 Earnings Call FAQ

1. How has Northern Arc Capital Limited (Northern Arc) managed to maintain such strong asset quality in the microfinance sector despite recent challenges?

Northern Arc attributes its strong asset quality to a combination of factors:

Deep domain knowledge and tested risk models: Northern Arc possesses extensive experience in the microfinance sector. They leverage this knowledge to create proprietary risk models, ensuring a thorough understanding of borrower behaviour and potential risks.

Ground-level engagement: The company actively visits a significant portion of its portfolio network, physically meeting borrowers and assessing loan origination and servicing processes. This hands-on approach provides valuable insights and early warnings of potential delinquencies.

Collaboration and knowledge sharing: Northern Arc collaborates with both NBFC MFIs and operates its own direct microfinance business, enabling the sharing of knowledge and best practices across the portfolio.

2. How does Northern Arc mitigate risks associated with its intermediate retail business model, specifically in the context of microfinance?

Northern Arc manages risk in its intermediate retail microfinance business through:

Loan-to-originate facilities: Northern Arc provides loans to partner lenders with pre-agreed risk criteria and target client profiles, ensuring lending aligns with Northern Arc's risk appetite.

Security and collateral: The company secures loans by taking specific charges on identified assets, providing a secondary source of recovery in case of default.

Portfolio coverage: Northern Arc typically requires a coverage ratio of 1.2 to 1.25x, meaning for every INR 100 lent, they have INR 120-125 of the underlying loan pool as security.

Cash flow analysis: Beyond collateral, Northern Arc assesses the overall cash flows of the partner lender to ensure sufficient repayment capacity even in stressed scenarios.

3. What factors contributed to the recent over-leveraging observed in the microfinance sector?

Two key regulatory changes contributed to over-leveraging:

Removal of interest rate caps: The Reserve Bank of India (RBI) lifted the interest rate cap on microfinance loans, leading to increased competition and potentially less prudent lending practices.

Relaxation of loan limits per borrower: The RBI removed the restriction on the number of microfinance loans an individual borrower could hold, previously limited to two NBFC MFI loans. This change, coupled with increased competition, resulted in some borrowers taking on multiple loans.

4. How does Northern Arc leverage its First Loss Default Guarantee (FLDG) arrangements in its partnership-based lending model?

FLDG arrangements are primarily used in digital lending partnerships, as per RBI guidelines. Northern Arc ensures the portfolio originated through these partnerships adheres to the guidelines, allowing them to utilise the FLDG as a risk mitigation tool.

5. What are Northern Arc's key competitive advantages in the Indian retail credit ecosystem?

Northern Arc's key competitive advantages include:

Domain expertise: Deep understanding of underserved sectors, including MSMEs, microfinance, consumer finance, and others.

Network effect: Extensive distribution network encompassing branches, lending partners, originator partners, and investors, providing access to a vast pool of borrowers and capital.

Data and technology: Proprietary scorecards, risk models, and technology platforms like Nimbus and Altifi enable efficient loan origination, servicing, and risk management.

Strong liability franchise: Diversified funding sources, including domestic and international DFIs, ensure access to capital at competitive rates.

6. How is Northern Arc positioned to benefit from the anticipated interest rate cuts in India?

Northern Arc is well-positioned to benefit from rate cuts due to:

Predominantly floating-rate liabilities: Around 65-70% of borrowings are linked to floating rates, enabling a reduction in interest expenses as rates decline.

Flexible asset repricing: A significant portion of the loan portfolio has shorter tenors or is linked to floating rates, facilitating asset repricing as interest rates fall.

7. What is Northern Arc's strategy for growth following its recent IPO?

Northern Arc aims to continue its growth trajectory by:

Leveraging IPO proceeds: The infusion of INR 500 crores will fuel expansion and support new initiatives.

Maintaining sectoral diversification: Prudently adjusting exposure across sectors based on risk-return dynamics and economic conditions.

Expanding technology capabilities: Continued investment in technology to enhance efficiency, reach, and customer experience.

Strengthening partnerships: Deepening relationships with existing partners and forging new alliances to expand reach and product offerings.

8. What are Northern Arc's expectations for credit costs in the coming quarters?

While specific guidance on credit costs was not provided, Northern Arc emphasized its proactive risk management approach, which includes:

Proactive provisioning: Building adequate provisions, including for Stage 1 and 2 assets, to absorb potential future losses.

Portfolio monitoring and adjustment: Continuously monitoring portfolio performance and making necessary adjustments, such as reducing exposure to higher-risk segments.

Robust collections infrastructure: Investing in technology and manpower to strengthen collection efforts and minimize losses.

Source: Link to Earning Call Transcripts

Disclaimer

Content Accuracy and Reliability: This summary of the earnings call is generated using an artificial intelligence large language model (LLM). While every effort has been made to ensure the accuracy and completeness of the information, the summary may not fully capture all nuances or details of the original earnings call. The content provided is for informational purposes only and should not be construed as financial advice or a recommendation to buy or sell any securities.

Verification: Readers are encouraged to refer to the official earnings call transcript, company filings, and other authoritative sources for comprehensive and accurate information. The creators of this summary do not guarantee the accuracy, completeness, or timeliness of the information and accept no responsibility for any errors or omissions.

No Liability: The use of this summary is at your own risk. The creators and distributors of this content disclaim any liability for any loss or damage arising from the use of or reliance on this summary.

Consult Professional Advice: For investment decisions or financial advice, please consult a qualified financial advisor or other professional.