NCC: PAT growth of 21% & Revenue growth of 26% in Q1-25 at a PE of 27

30%+ EBITDA growth with 15% revenue growth in FY25. Possibility of upward revision of FY25 revenue guidance. Order book 2.2X+ revenue expected in FY25. At a free cash flow yield of 5.4%

1. Why is NCC interesting?

ncclimited.com | NSE : NCC

NCC's order book exceeding Rs 52,000 cr, more than double the expected revenue for FY25, combined with an expected FY25 order inflow of Rs 20,000-22,000 cr, lays a strong foundation for growth through to FY27. Additionally, the potential for an upward revision in FY25 revenue guidance alongside an EBITDA growth exceeding 30% presents a compelling short-term opportunity for FY25.2. Second largest listed construction company by revenue

EPC company with in-house design and engineering capabilities

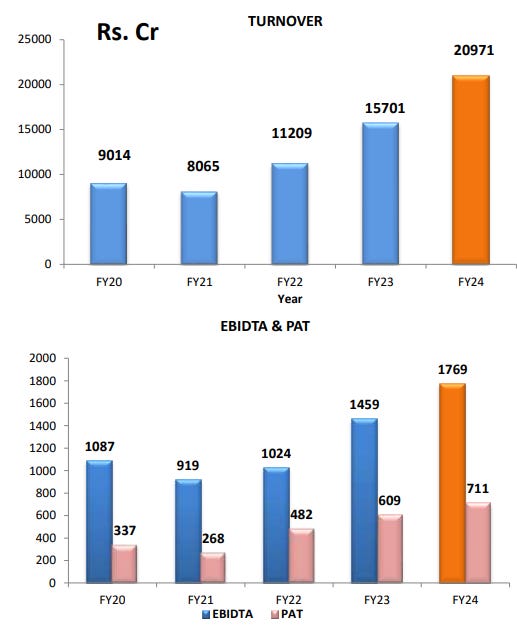

2. FY20-24: PAT CAGR of 21% & Revenue CAGR of 24%

3. Strong FY23: PAT up 26% & Revenue up 40%

4. FY24: PAT up 17% & Revenue up 34%

5. Q1-25: PAT up 21% & Revenue up 26%

6. Business metrics: Improving return ratios

FY24: On a consolidated basis, the RoCE reported is 15.77% as against 14.41%.

7. FY25 Outlook: 15%+ revenue growth & 30%+ EBITDA growth

i. Guidance for FY25

Order Inflow Guidance: Rs 20,000 to Rs 22,000 crore

Revenue Guidance: Growth upwards of 15%

Margin Guidance: EBIDTA margins between 9.5% to 10%

ii. Strong order book: Order book 2.2X+ expected revenue of FY25

So, for the year 24-25 we give a guidance on order booking about 20,000 to 22,000 considering the present market environment particularly the general elections, followed by some state assembly elections.

ii. FY25: Conservative guidance for 15%+ revenue growth

Top line growth guidance about 15% plus as against 20% guidance given in the last year.

Possibility of guidance revision: In the second-half year, at that time, we can comment on that one about how the third and fourth quarter progress. At that time again, we will confirm you on that one

iii. FY25: 30-36% surge in EBITDA as margin expands to 9.5-10%

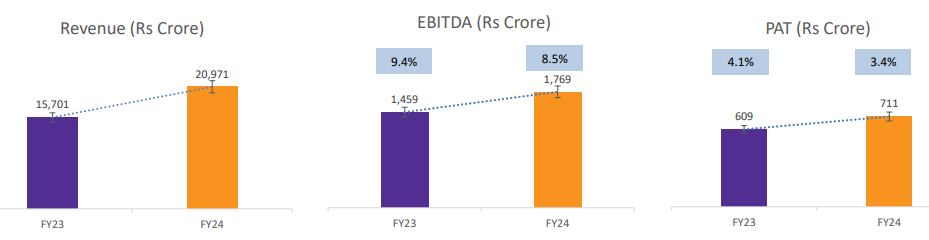

In FY25, EBITDA is projected to surge by 30-36%, reaching Rs 2291-2411 cr, up from Rs 1769 cr in FY24, driven by a revenue growth of 15% and an EBITDA margin expansion from 8.5% to 9.5-10%.

We expect the EBITDA margin 9.5% to 10%. Going forward, next couple of years, our intention is always to keep the needle moving.

8. PAT growth of 21% & Revenue growth of 26% in FY24 at a PE of 29

9. Do I stay?

If I hold the stock then one may continue holding on to NCC

NCC has outperformed its FY24 guidance and is on track with its Q1-25 performance to meet the FY25 guidance.

We have given guidance for order booking for FY23-24 as INR26,000 crores whereas we have achieved INR27,283 crores and top line we have given a growth of 20%, but we achieved 37%.

NCC's order book exceeding Rs 52,000 cr and an anticipated order inflow of Rs 20,000-22,000 cr in FY25 ensure strong revenue visibility through at least FY27, presenting a case for long-term investment in the company.

NCC hints at potential upward revisions of FY25 guidance in revenue and orders by H2-25.

So if there is no impact -- good impact on the front of the elections, so we may get more orders. But a minimum of 20,000 to 22,000 is the benchmark the company has kept.

Despite NCC management's guidance for an EBITDA margin expansion to 9.5-10% in FY25, the company's PAT growth has not kept pace with revenue growth in FY24 and Q1-25. Without significant margin improvement, NCC risks becoming less attractive as its earnings growth lags behind the targeted 15% revenue growth.

10. Do I enter?

If I am looking to enter NCC then

NCC delivered PAT growth of 21% & revenue growth of 26% in Q1-25 at a PE of 27 which makes the valuations fully valued in the short term

NCC on a current market cap of Rs 20,354 cr generated free cash flow of Rs 1,108 cr in FY24 which implies that its available at a FY24 free cash flow yield of 5.4% which makes the valuations quite reasonable.

NCC has grown its free cash flow from Rs 877 cr in FY23 to Rs 1,108 cr in FY24 a growth of 26% (vs PAT growth of 17%) at PE of 27 which makes the valuations reasonable. One can expect strong fee cash flow generation in FY25 to continue as capex in FY25 is expected to be lower.

Capex Spend: In FY '24, we spent about INR285 crores. Full year, we were budgeting around Rs. 250 crores and we have done around Rs. 51 crores at the end of the 1st Quarter.

Top-line growth of 15%+ in FY25 with EBITDA growth of 30%+ at a PE of 27 which makes the valuations fairly valued in the medium term

Previous coverage on NCC

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer