Maharashtra Seamless: PAT growth of 50% with flat revenue in H1-24 at PE of 11

Strong outlook for the biggest PAT in FY24. Revenue visibility based on a order book. Track record of generating free cash at reasonable valuations with cushion of cash in the balance sheet

1. Manufacturing of Steel Pipes and Tubes

jindal.com/msl-seamless-pipe.html | NSE : MAHSEAMLES

Market share of 55% in seamless pipes segment.

Market share of 18% in the API certified, high frequency ERW pipes segment.

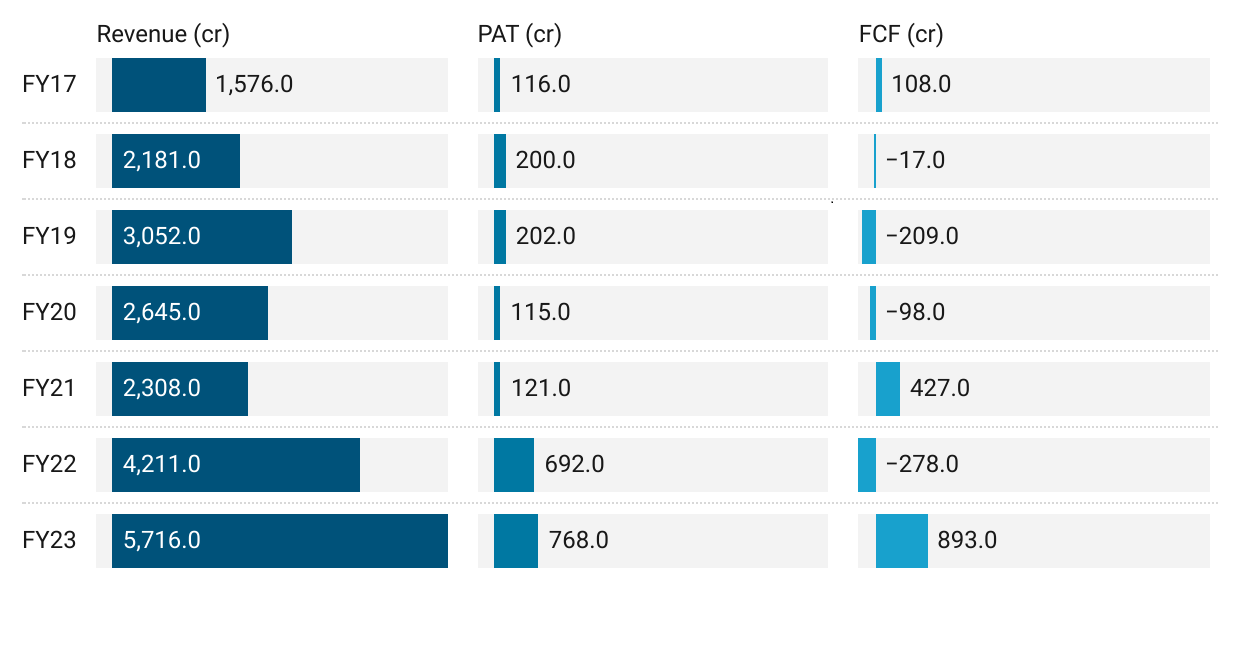

2. FY17-23: Years of low or no growth followed by a pickup in FY22

FY17-23 CAGR:

Revenue = 24%

PAT = 37%

Free cash flow (FCF) = 42% i.e. PAT converted into free cash for MAHSEAMLES

3. FY23: PAT up 11% and Revenue up 36% YoY

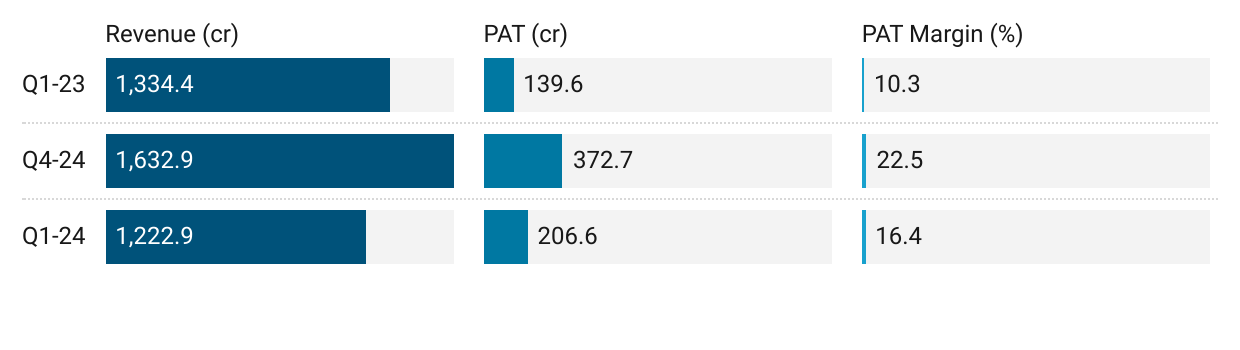

4. Q1-24: PAT up 48% & Revenue down 8% YoY

5. Q2-24: PAT up 56% & Revenue up 9% YoY

PAT up 21% & Revenue up 26% QoQ

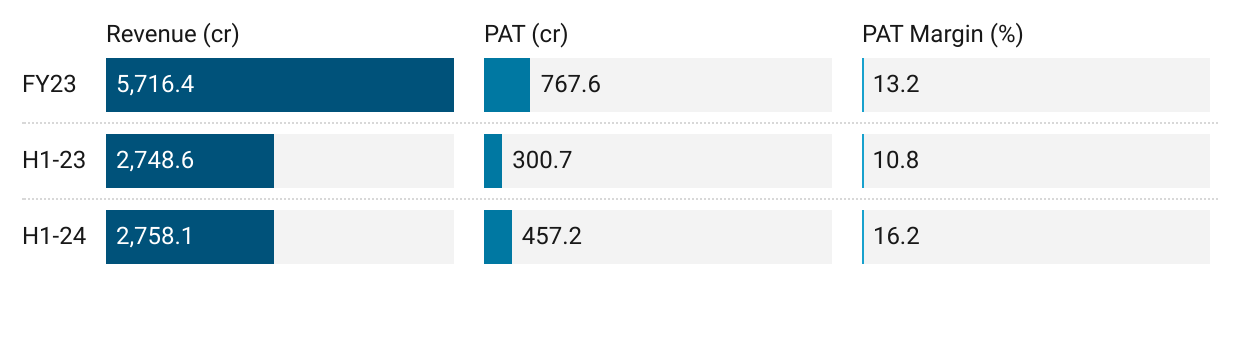

6. H1-24: PAT up 52% & Revenue is flat

7. Business metrics: Solid return ratios

8. Outlook: Revenue growth of 33% between FY24-FY26

i. FY24: 5% volume growth

ii. Revenue growth of 33% between FY24-FY26

Planned capex expected to increase revenue by Rs 1,900 cr by FY26 which around 33% higher than the revenue expected for FY24.

iii. Strong revenue visibility: Order book = 3 months of revenue

The order book stands at 1,459 crores. This appears to be a reduction from the earlier order book which was communicated in July, which was at 1,725 crores. I would like to clarify that orders of around 325 crores have been confirmed and are in pipeline. The reason why they have not been included is because the purchase order is awaited.

9. PAT growth of 52% with flat revenue in H1-24 at a PE of 11

10. So Wait and Watch

If I hold the stock then one may continue holding on to MAHSEAMLES

Based on H1-24 performance, MAHSEAMLES looks on track to deliver the strongest PAT in terms of PAT since FY17

With 5% growth in FY24, the future growth is dependent solely on timely execution of planned Capex. Time and cost overruns in the execution of the capex could be a reason to exit the stock. One needs to keep a close watch on the capex execution every quarter.

11. Or, join the ride

If I am looking to enter MAHSEAMLES then

MAHSEAMLES has delivered PAT growth of 50%+ in H1-24 at a PE of 11 which makes valuations reasonable.

MAHSEAMLES delivered Rs 543 cr of free cash flow against a market cap of Rs 12,424 cr. As of H1-24 end it is available on a free cash flow yield of 4.4% (not annualized) which makes the valuations quite attractive.

Increasing promotor holding inspiring confidence in MAHSEAMLES

The current stake is 68%. Promoter and Promoter Group have earlier committed that they will gradually increase their stake to 75%. That is still an open option.

Rs 1,224 cr of liquid investments on books as of end of Q2-24 implies that about 10% of market cap is in liquid investments which provides a margin of safety in the valuations.

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades