Macrotech Developers Q4 FY25 Results: Predictable Growth, Premium Valuations, Stronger Future Cashflows

Macrotech combines strong FY25 execution, clear FY26 growth visibility, premium valuations backed by high RoE, & optional upside from rentals & new cities.

Table of Content

Macrotech Developers (Lodha) Financial Performance Overview

Macrotech Developers Management Commentary and FY26 Outlook

Macrotech Developers Valuation Analysis

Implications for Investors: What to Watch

1. Macrotech Developers (Lodha) Financial Performance Overview

Macrotech Developers ended FY25 not just bigger, but stronger and structurally de-risked, setting a powerful foundation for FY26 and beyond.

1.1 Q4 FY25 Results: Key Drivers Behind Macrotech's Growth

Macrotech Developers closed FY25 on a high note, delivering another record-breaking quarter that solidified its reputation as India's leading residential real estate platform.

Q4 wasn’t just about solid numbers — it was about showcasing the predictability and strength of Macrotech's business model heading into FY26.

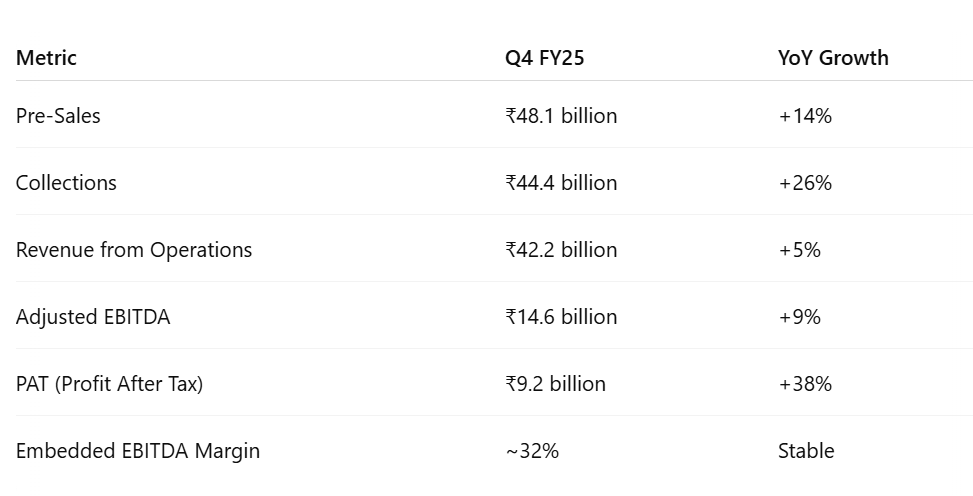

Key Q4 FY25 Financial Metrics:

Performance Drivers:

Sales Consistency: Fifth consecutive quarter with pre-sales exceeding ₹40 billion, reflecting a highly predictable and scalable sales model.

Robust Collections: Conversion of sales into cash remained strong, with ₹44.4 billion in collections, providing ample fuel for both growth and debt reduction.

Margin Resilience: Despite inflationary pressures, embedded EBITDA margins stayed stable at ~32%, underscoring disciplined execution.

Debt Reduction: Net debt shrank by ₹3.1 billion sequentially, further improving the company’s already conservative balance sheet (Net Debt/Equity of 0.20x).

Noteworthy Micro-Market Performance:

Western Suburbs, Mumbai: Pre-sales more than doubled (+140% YoY), driven by Lodha’s “supermarket strategy” of hyperlocal project presence every 2–4 km.

1.2 FY25 Full-Year Financial Highlights: Revenue, Margins, and Profit Growth

Macrotech Developers scaled new financial peaks in FY25, achieving high-quality growth across all major metrics.

Annual Performance Drivers:

Margin Expansion: EBITDA margin improved from 33.3% to 36.0%, thanks to price growth, operating leverage, and cost discipline.

Profitability Boost: PAT margin jumped from 15.4% to 19.6%, highlighting a sharp uplift in return on capital employed.

Business Development: Lodha added 10 new projects with a GDV of ₹237 billion, surpassing its full-year guidance and securing future growth pipelines.

Credit Upgrade: India Ratings upgraded Lodha’s credit rating to AA (Stable), validating its financial resilience.

Strategic Progress:

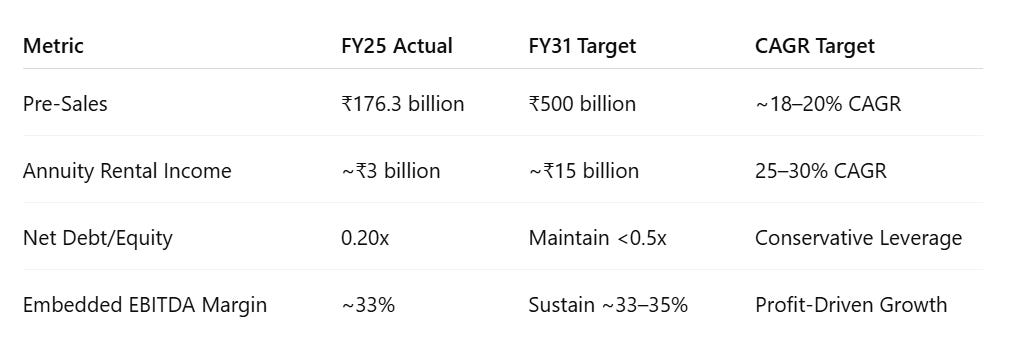

Expanded rental annuity income platform significantly, laying the groundwork for ₹15 billion in recurring income by FY31.

Continued diversification across MMR, Pune, and Bengaluru markets to mitigate city-specific risks.

1.3 Segment-Wise Performance Analysis: Residential, Commercial, and Regional Trends

Macrotech’s "micro-market + supermarket strategy" — building presence every few kilometers — is creating highly resilient, diversified cashflows across India’s top property hubs.

Residential Business:

Remained the core growth driver, contributing over 90% of pre-sales.

Premium and mid-income housing saw the highest absorption, particularly in the Western Suburbs of Mumbai and Pune.

Commercial/Annuity Business:

Rapid scale-up in digital infrastructure (warehousing and industrial leasing) with 5 active locations.

Office and retail portfolio expected to contribute over ₹5.6 billion in annual rental income by FY31.

Regional Mix FY25:

MMR (Mumbai Metropolitan Region): ~60% of total pre-sales, anchored by strong launches in Western and Eastern suburbs.

Pune: Delivered ₹25 billion+ in pre-sales, with multiple new project additions deepening its local footprint.

Bengaluru: Early-stage but promising growth, with 5 locations operational by end-FY25.

2. Macrotech Developers Management Commentary and FY26 Outlook

Macrotech’s management is walking a clear path — profitable 20%+ growth, predictable cashflows, financial conservatism, and building a future-ready portfolio for India's $5 trillion economy vision.

2.1 FY26 Guidance: Targets for Growth and Profitability

Macrotech Developers enters FY26 with strong momentum and ambitious, yet achievable, targets

Management is targeting another year of predictable ~20% growth in pre-sales, while maintaining best-in-class margins and strict financial discipline.

2.2 Strategic Priorities for FY26: Growth Plans and Execution Focus

Macrotech’s gameplan for FY26 is centered around profitable growth with de-risking:

Expand Micro-Market Presence:

Strengthen leadership in MMR (Mumbai), accelerate share gains in Pune, and deepen presence in Bengaluru.New City Pilot Entry:

Launch pilot projects in a new metro city (details yet undisclosed) — a strategic move to diversify beyond the existing strongholds.Scale Annuity Business:

Target visible growth in warehousing, high-street retail, and commercial offices — adding steady recurring revenue streams toward the ₹15 billion rental income goal by FY31.Debt Management Discipline:

Despite aggressive business development plans, net debt ceiling maintained below 0.5x Equity — prioritizing financial resilience.Sustain Pricing Power:

Focus on premiumization, strong branding, and product differentiation to avoid unnecessary price wars and protect margins.

2.3 CEO and Management Commentary: Key Themes and Market Insights

Abhishek Lodha, MD & CEO, summed up the company’s outlook with clarity:

"Our consistent 20% growth since IPO is not an accident — it's a result of a predictable and disciplined business model. We are confident that Macrotech is at the epicenter of India’s massive housing upcycle, and we are investing wisely to capture this opportunity, without losing sight of profitability or balance sheet strength."

Additional Management Themes:

Demand for premium and mid-income housing remains robust, fueled by rising urban incomes and infrastructure upgrades.

Collections strength is expected to remain high, supporting cash generation and de-leveraging.

Infrastructure tailwinds in Mumbai (metro expansions, bullet train, freeway projects) will enhance real estate demand corridors, especially for Lodha's developments.

Cost of capital trending lower will further support profitability expansion over FY26–FY27.

2.4 Longer-Term Growth Outlook: Vision for FY31 and Beyond

Macrotech Developers isn’t just planning for the next quarter — it has a well-articulated long-term roadmap:

Key Longer-Term Growth Catalysts:

Urbanization boom: 75–100 million new homeownership-capable households expected this decade.

Infrastructure mega-projects in MMR to compress travel times and boost residential demand.

Pricing tailwinds: Premium real estate pricing in Mumbai, Pune, and Bengaluru still significantly trails global urban benchmarks.

Low mortgage penetration in India (only ~11% of GDP) leaves headroom for housing credit growth.

Strategic Vision:

Lodha aims to transition from being "the leader in sales" to "the leader in long-term compounding cash flows" — blending premium branding, operational excellence, and recurring income streams.

3. Macrotech Developers Valuation Analysis

Macrotech Developers' stock is fully priced for execution — but hidden upside from annuity income scale-up, margin expansions, and new city successes could surprise to the upside over the medium term.

3.1 Current Valuation Snapshot: Metrics and Multiples

Macrotech Developers’ valuation reflects both its strong operating momentum and its market leadership position in Indian residential real estate.

Growth Premium:

Investors are paying a premium multiple (~47.5x) because Lodha offers predictable 20%+ annualized growth in pre-sales, margins >30%, and strong operating cash flows.Annuitized Earnings Not Fully Visible Yet:

The annuity (rental) income from commercial, retail, and warehousing projects will materially increase earnings over the next 5–6 years. Current reported PAT does not yet fully capture this future earnings visibility — making the "effective" forward P/E lower over time.Deleveraging and Cost of Capital Tailwind:

As Lodha continues to pay down debt and borrowing costs fall (current cost of debt already at 8.7%), net profits should grow faster than operating profits — compressing P/E naturally without needing aggressive top-line growth.

The stock trades rich at 47.5x trailing earnings.

However, the 20% RoE, low net debt, scalable rental streams, and India’s housing cycle tailwinds offer strong earnings compounding visibility.

Investors are effectively paying up for a high-quality, fast-compounding real estate platform — not just a static balance sheet.

When compared to major Indian real estate developers, Lodha’s valuation sits at a moderate premium — but is supported by higher returns and stronger growth visibility.

While Lodha trades at a similar or lower P/E than DLF and Godrej Properties, it offers materially higher RoE and a cleaner, de-leveraged balance sheet.

Among large listed realty players, Lodha offers the best combination of:

High earnings quality

Strong balance sheet

Predictable sales growth

even though it trades at only a moderate valuation premium compared to sector heavyweights like DLF and Godrej Properties.

3.2 What’s Priced Into Macrotech Developers Stock Today

At current levels, the market appears to have already priced in:

Continuation of 20%+ pre-sales CAGR through FY26–FY28.

Sustained 33–35% embedded EBITDA margins.

Further net debt reduction with strong operating cash flows.

Ongoing success in MMR, Pune, and Bengaluru with current projects.

👉 Essentially, the stock is priced for execution on the base-case growth plan — not for margin expansion or annuity upside.

3.3 Optional Upsides: Hidden Growth Drivers and Underappreciated Catalysts

Despite the stock trading at premium multiples, optional upsides exist that are not fully priced in yet:

Annuity Income Scale-up:

Rental streams could hit ₹15 billion/year by FY31 — adding valuation support through stable cashflows akin to REITs.New City Expansion:

Success in the pilot city (planned in FY26) could unlock an entirely new growth runway beyond MMR-Pune-Bengaluru.Cost of Debt Reduction:

Further 50–75 bps decline in borrowing costs over FY26–FY28 would lift margins and free cash flows.Brand Premiumization:

Lodha's premium projects (World Towers, Park, etc.) gaining stronger ASPs (average selling prices) can drive higher profitability than modeled.

4. Implications for Investors: What to Watch

Macrotech Developers offers asymmetric reward-to-risk for investors aligned with India’s housing boom — with strong compounding potential if management executes on both housing and annuity ambitions over the next 3–5 years.

4.1 Bull, Bear, and Base Case Forecasts for Macrotech Developers Stock

To help frame risk and reward, here’s a structured look at different scenarios over the next 12–18 months:

The base case still offers attractive returns given Lodha’s balance sheet strength and high predictability, while the bull case unlocks even larger upside through optional growth levers.

4.2 Investment Thesis: Why Consider Macrotech Developers

Reasons to Stay Invested or Add to Position:

Predictable Growth Engine: 20% pre-sales CAGR now proven over four consecutive years post-IPO.

Superior Profitability: 36% EBITDA margin and 20% RoE are best-in-class among Indian real estate majors.

Balance Sheet Resilience: 0.20x Net Debt/Equity provides a margin of safety against cyclical downturns.

Macro Tailwinds: Rising urban incomes, infrastructure upgrades (metro, airports, freeways), and housing supply consolidation strongly favor top-tier developers like Lodha.

Optional Upsides: Annuity business growth and new city expansions are not fully captured in current valuations.

4.3 Key Risks to Watch and Risk Mitigation Strategies

While the long-term story remains robust, investors should stay alert to certain risks:

Lodha’s relatively premium target audience (upper mid-income, premium buyers) is typically less rate-sensitive compared to affordable housing buyers — reducing downside volatility.

4.4 Investor Profile Outlook: Who Should Own Macrotech Developers Stock?

Best Suited For:

Long-Term Compounders: Investors looking for 3–5 years of compounding from housing and annuity growth themes.

Growth-Oriented Portfolios: Those seeking exposure to India’s housing demand upcycle and urban expansion.

Moderate Risk Investors: Those willing to accept cyclical ups and downs for a fundamentally strong, cash-generative company.

Less Suited For:

Short-Term Traders: Lodha's stock may not show daily/weekly momentum unless backed by macro news flow.

Deep Value Investors: The stock is not “cheap” in a classical value sense; it’s priced for predictable quality and growth.

Disclaimer

Content Accuracy and Reliability: This summary of the earnings call is generated using an artificial intelligence large language model (LLM). While every effort has been made to ensure the accuracy and completeness of the information, the summary may not fully capture all nuances or details of the original earnings call. The content provided is for informational purposes only and should not be construed as financial advice or a recommendation to buy or sell any securities. Verification: Readers are encouraged to refer to the official earnings call transcript, company filings, and other authoritative sources for comprehensive and accurate information. The creators of this summary do not guarantee the accuracy, completeness, or timeliness of the information and accept no responsibility for any errors or omissions. No Liability: The use of this summary is at your own risk. The creators and distributors of this content disclaim any liability for any loss or damage arising from the use of or reliance on this summary. Consult Professional Advice: For investment decisions or financial advice, please consult a qualified financial advisor or other professional

Like