M&B Engineering FY26 Results: PAT up 20%, Steady FY27 Guidance

Guiding 25% revenue growth in FY27. Uncertainty over margins is a risk. Trading at reasonable forward valuation for business promising 25% growth.

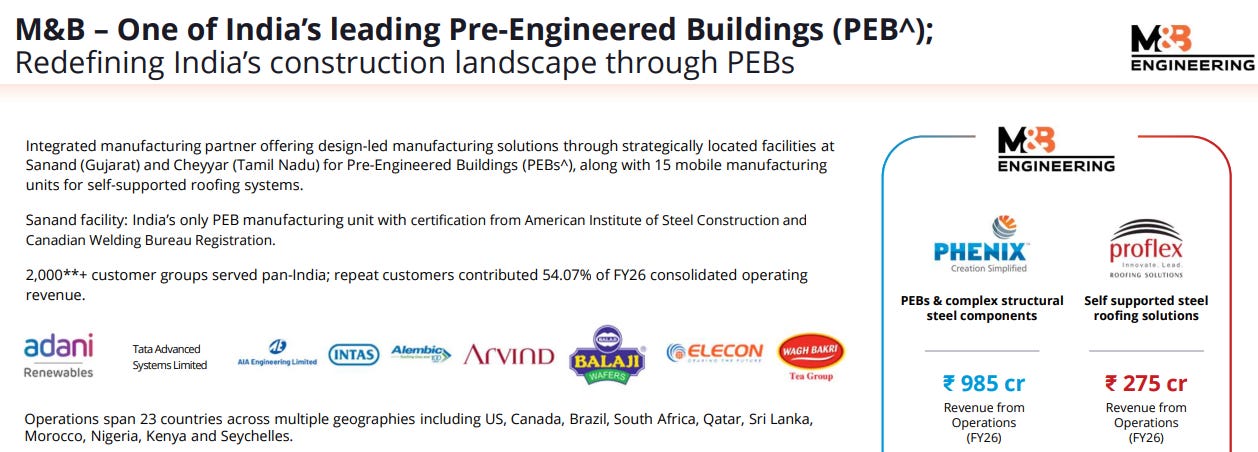

1. Leading Pre-Engineered Buildings Player

mbel.in | NSE: MBEL

Business Segments

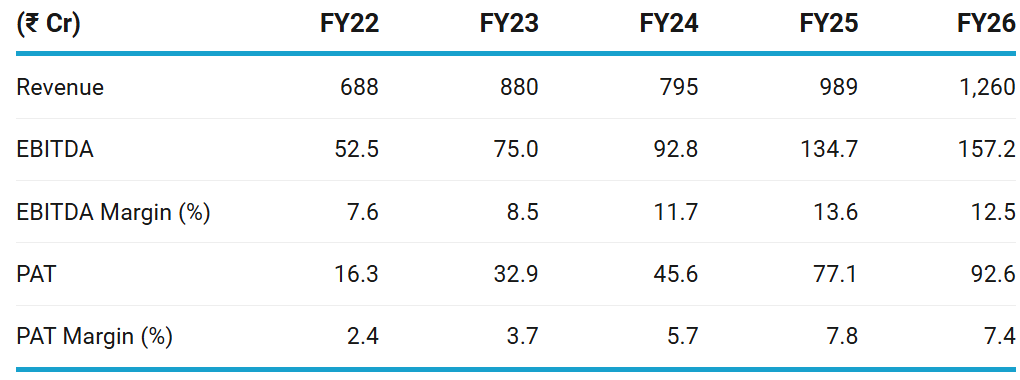

2. FY22-26: PAT up 54% & Revenue up 16% CAGR

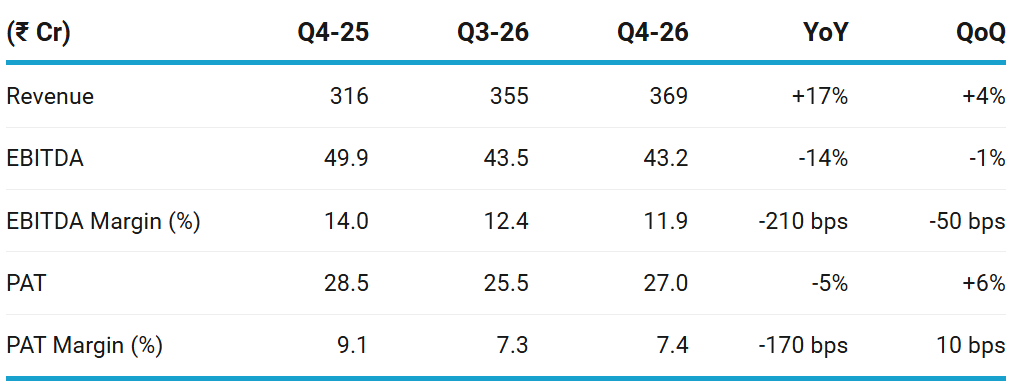

3. Q4 FY26: PAT down 5% & Revenue up 17% YoY

PAT up 6% & Revenue up 4% QoQ

Q4 was an execution quarter, not a margin quarter.

MBEL delivered the revenue number and exited FY26 with a strong order book. Q4 exposed the key risk in MBEL: growth is visible, but margins are vulnerable to FX, steel, freight and export-mix changes.

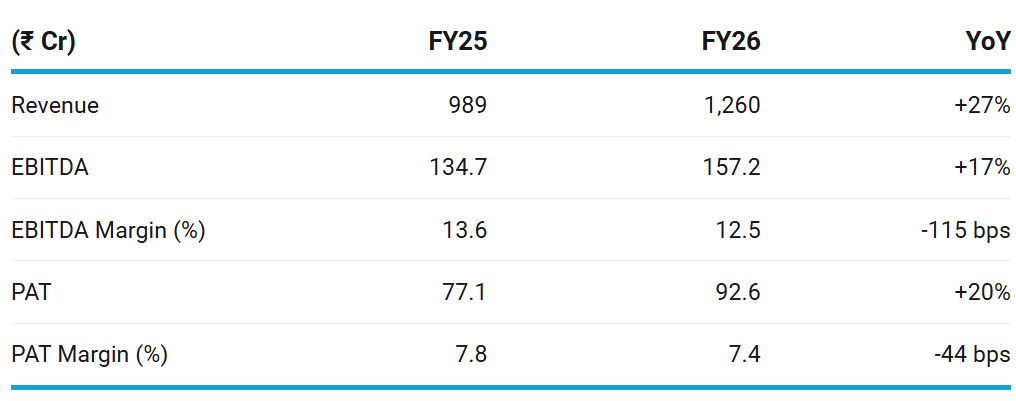

4. FY26: PAT up 20% & Revenue up 27% YoY

FY26 was a strong growth year. Revenue grew 27%, PAT grew 20%, and order inflow/order book improved. But EBITDA growth lagged revenue growth, so operating leverage did not fully show up.

Segment performance

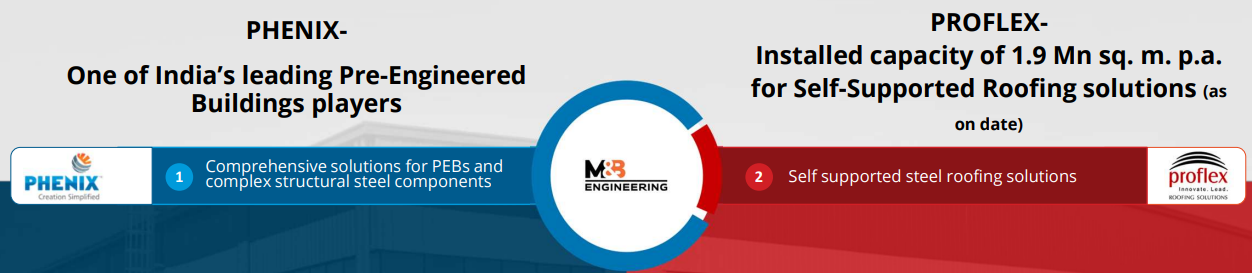

Phenix / PEB — ₹985 Cr Main growth engine; ~78% of revenue

Proflex / self-supported roofing — ₹275 Cr. Smaller but strong niche business

M&B is not only an export story. Domestic industry/infra remains the base.

Export is the upside lever, especially for Phenix.

Exports are scaling fast, mainly North America.

MEB’s reiterates that Sanand is India’s only PEB facility with AISC and CWB certifications, which supports the US and Canada opportunity.

Exports also bring volatility — FX, freight, tariffs and delivery/revenue recognition timing.

Balance sheet and capital allocation

FY26 balance sheet improved after IPO.

Net debt/equity fell from 0.61x in FY25 to 0.12x in FY26. — leverage is now comfortable.

FY27 planned capex is ~₹100 Cr, so capital efficiency needs to hold.

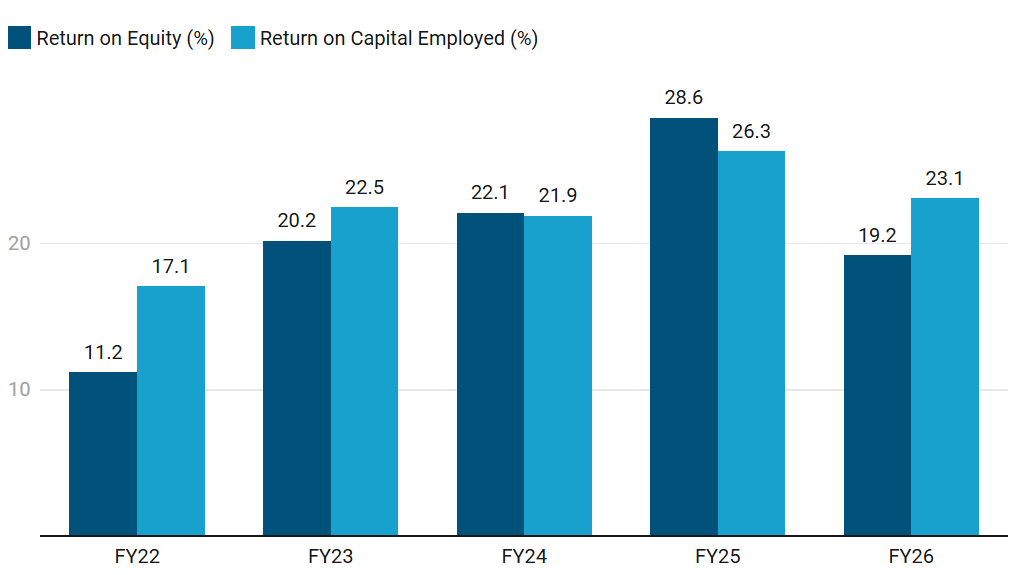

5. Business Metrics: Stable Return Ratios

ROE fell from 28.6% to 19.2% in FY26, but this is not necessarily due to business deterioration alone. FY26 included the IPO, which increased equity/net worth sharply.

RoCE fell from 26.3% to 23.1%, but remains strong. This is more important operationally because it captures return on capital employed, not just shareholder equity. A 23% RoCE is still healthy for an engineering/manufacturing business.

The concern is the direction: FY25 was peak return efficiency, FY26 normalized lower. Revenue and PAT grew, but margin pressure, higher working capital, and expanded capital base pulled return ratios down.

With FY27 capex planned, return ratios may remain under pressure unless revenue growth and margins improve.

Can MBEL grow while keeping RoCE above 20%?

If yes, valuation comfort improves. If RoCE drops below 18–20%, the market may treat it as a lower-quality growth business.

6. Outlook: 25% Growth in FY27

6.1 FY27 Guidance

FY27 guidance is positive on growth but cautious on margin

For FY '27, we remain confident of delivering top-line growth of around 25% year-on-year, supported by the strong order book already in hand and the continued rise in demand for preengineered buildings and self-supported roofing systems across different sectors. At the same time, we expect some near-term challenges. The impact of the Iran conflict is likely to be reflected in the short term, particularly through margin pressure and execution delays. Labor availability constraints, which are typical in the first quarter, along with monsoon-related challenges in Q2, may also result in softer performance in the first half of the year.

We feel that this is a bit premature for us to give any margin guidance for FY26- 27 for three very clear reasons.

One, the whole costing currently, as you know, steel prices have gone up by 20% just in the last quarter.

Then the freights are very uncertain. On the export freight availability of containers and freight, it keeps on fluctuating very widely.

FX, we are not able to control exactly. While of course, we have a good export order book of about INR280 crores, we are hopeful of a continued stronger margin profile, but we want to wait and watch for at least one more quarter before which we will give any specific margin guidance.

Implied FY27 revenue & margin:

At 23–25% growth, FY27 revenue could be roughly ₹1,550–1,575 Cr.

Similar margins as FY26

Order book visibility — strongest part of the outlook.

As on 31 Mar 2026, unexecuted order book stood at ₹ 1,083 crore, representing a 35 % YoY growth

Proflex division accounted for 20% (₹212 crore)

Phenix division accounted for 80% (₹871 crore)

Within the Phenix, export orders were ₹279crore

Management said the existing order book and visible pipeline provide strong future execution visibility.

Export outlook

Exports remain the key margin and growth lever.

Focus on North America, supported by Sanand’s AISC certification for the US and CWB certification for Canada.

25% reduction in US sectoral import tariff should improve competitiveness and traction.

The earnings call was not all rosy. Management said US order closures have become slower due to inflationary pressures, so they want to balance margin improvement with building a good order book.

H1 vs H2 outlook

FY27 is likely to be H2-heavy. MBEL warned:

Q1 may be softer due to labor availability constraints.

Q2 may be impacted by monsoon.

Iran conflict may cause short-term execution delays and margin pressure.

They specifically asked investors to judge the business on a full-year basis, not quarter by quarter.

For FY27, the key question is not whether revenue can grow. MBEL has order book support. The key question is whether MBEL can deliver 25% growth while holding ~12.5–13% EBITDA margin and keeping CFO positive.

7. Valuation Analysis — M&B Engineering

7.1 Valuation Snapshot

Current Market Price — ₹286.6

Market cap — ₹ 1,637.9 Cr

MBEL looks reasonably valued, not expensive — but not a screaming bargain unless FY27 guidance is delivered .

EV/EBITDA still looks reasonable even conservatively.

For a company guiding ~25% revenue growth, with export scale-up, order book visibility and a net-cash balance sheet, 14x FY27E P/E is not expensive.

Sensitivity — margin matters more than revenue

Stock is not very sensitive to revenue guidance, because 25% growth is already assumed. The real upside comes if PAT margin improves from 7.35%. The real downside comes if margin slips below 7%.

7.2 Opportunities at Current Valuation

Reasonable valuation with execution upside

Not deep value because FY26 cash flow was weak and management has not given FY27 margin guidance.

The rerating trigger is simple: deliver 25% growth + hold 12.5–13% EBITDA margin + turn CFO positive.

Valuation is not demanding for 20–25% growth

Export scale-up can change the margin profile

Exports are still only ~13% of revenue, so there is room to scale.

Sanand is a key advantage because it is India’s only PEB manufacturing unit with both AISC and CWB certifications, supporting US and Canada access.

If North America scales from ~13% revenue share toward 18–20%, MBEL can get both revenue growth and better realization. That can support EBITDA margin recovery, provided freight / FX / tariffs don’t offset the benefit.

8.3 Risks at Current Valuation

The market is probably discounting three risks:

Margins are not guided for FY27.

Management refused margin guidance because of steel-price inflation, freight volatility, FX and geopolitical uncertainty.FY26 cash conversion was weak.

PAT was healthy, but operating cash flow was negative due to working-capital absorption. So valuation should not be judged only on P/E.FY27 capex is high.

Management guided for around ₹100 Cr capex in FY27, including Sanand expansion, part Cheyyar expansion and regular capex.

US order closures have slowed

US order closures have become “longish” due to inflationary pressure. They are trying to balance margin improvement and order-book creation.

If US orders take longer to convert, FY27 export revenue may disappoint. That would reduce the margin-upside narrative.

Return ratios may normalize lower

With ₹100 Cr capex in FY27, ROCE may remain under pressure unless revenue ramps quickly and margins stabilize.

The stock is cheap only if FY27 earnings scale. If PAT stays near ₹90–100 Cr, current valuation becomes ordinary, not cheap.

Risk is moderate, not high — but very margin-sensitive.

Help your group stay ahead. Share now!

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer