Kuantum Papers: 27-32% EBITDA growth and 15% revenue growth at a PE less than 7

Growth started from FY22 after many years. Momentum has made KUANTUM attractive in terms of valuations. It has potential to get rerated but it needs growth to be delivered in FY24 too.

1. Kuantum Papers Ltd, a paper manufacturer

kuantumpapers.com | NSE : KUANTUM

Kuantum Papers Ltd, a leading wood and agro based paper manufacturer.

Largest product Portfolio in the Paper Industry

Kuantum’s product offerings include maplitho, creamwove and value added specialty products like Thermal paper, bond paper, parchment paper, Azurelaid paper, catridge paper, coloured paper, ledger paper, stiffner paper, cupstock paper, carrybag paper and straw paper with a GSM range of 42 – 200.

A cash generating business model

Order based manufacturing: The production is order based and manufacturing is undertaken after the company receives advance orders from dealers/distributors.

Inventory: Inventory of finished goods is low and rarely exceeds three days’ production.

Collection Mechanism: Collection is done strictly within 5 days of date of Invoice.

2. FY17-23: PAT CAGR of 15% & Revenue CAGR of 13%

KUANTUM broke the stagnation of Rs 700-800 cr revenue mark in FY 22 and then carried forward the momentum in FY23

3. Strong FY23: 10x FY22 PAT & Revenue up 58% YoY

We closed the financial year 2023 on a strong note with highest ever annual revenue of Rs. 1,310 crores with EBITDA of 28.96% or say 29%.

4. Strong Q1-24: Positive PAT from losses & Revenue up 14% YoY

~50% of FY23 PAT delivered in Q1-24

During the year and under review, our revenue was reported at Rs.313 crores, representing a 14% year-on-year increase. Our EBITDA is Rs.110 crores, which is an 80% increase compared to the same period last year and EBITDA margin stood at 35%.

5. Return ratios at an all time high in FY23

6. Outlook: 15% revenue & 27-32% EBITDA growth

i. 15% revenue growth and 27-32% EBITDA growth in FY24

A turnover of around Rs 1500 cr in FY24 implies a 15% revenue growth over the FY23 revenue of Rs 1309.6 cr.

An EBITDA of around Rs 480-500 cr in FY24 implies a 27-32% EBITDA growth over the FY23 EBITDA of Rs 379 cr.

You see, our turnover is going to be around Rs. 1,500 crores and going by EBITDA of 33% we expect EBITDA amount is around Rs. 480 - 500 crores.

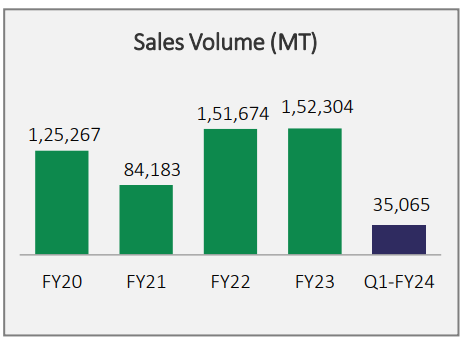

ii. 7% volume CAGR till FY25

Volume increasing to 1.62-1.64 lakh ton to 1.75 lakh ton in FY24 and FY25 implies a 7% volume CAGR for FY23-25

FY24: we will sort of close the year at about 1,62,000 or 1,64,000 tons at the year end

FY25: We will try and achieve certainly 1.75 lakh tons

7. 15% revenue & 27-32% EBITDA growth in FY24 at a PE of less than 7

8. So Wait and Watch

If I hold the stock then one may continue holding on to KUANTUM only if one is comfortable waiting patiently for the stock to be valued fairly by the market.

Between FY17 and FY20, the company experienced a period of stagnant growth, followed by a challenging FY21. However, FY22 showed signs of recovery, and FY23 proved to be a strong year. Therefore, in terms of performance, there's been only one robust year since FY17. It's crucial to keep a close eye on KUANTUM's business performance because one doesn’t want to be tied to a company with no growth prospects.

While there's potential for the stock to be revalued, it's dependent on the company's ability to deliver consistent growth and in this context it becomes important that the momentum delivered in Q1-24 continues in the remaining quarters of FY24.

9. Or, join the ride

If I am looking to enter the stock then

KUANTUM is guiding for 15% revenue growth and 27-32% EBITDA growth in FY24 at a PE of less than 7 which makes the valuations quite reasonable.

KUANTUM generated free cash flow of Rs 310 cr on a market cap of Rs 1554 cr implies that its trading a free cash flow yield of 20% which makes the valuations quite attractive.

A net worth of Rs 967 cr on a market cap of around Rs1554 cr implies that KUANTUM is available for price to book of 1.6 which makes the valuations quite reasonable.

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades