Kaynes Technology: PAT up 93% & Revenue up 60% in FY24 at a PE of 141

Guidance for 60% revenue growth and 70% EBITDA growth in FY25. Order book 1.4X FY25 expected revenue to support FY25 guidance. FY24-29 outlook for 60% revenue CAGR

2. FY20-24: PAT CAGR of 166% & Revenue CAGR of 62%

3. Strong FY23: PAT up 128% & Revenue up 59% YoY

4. Strong 9M-24: PAT up 89% & Revenue up 53%

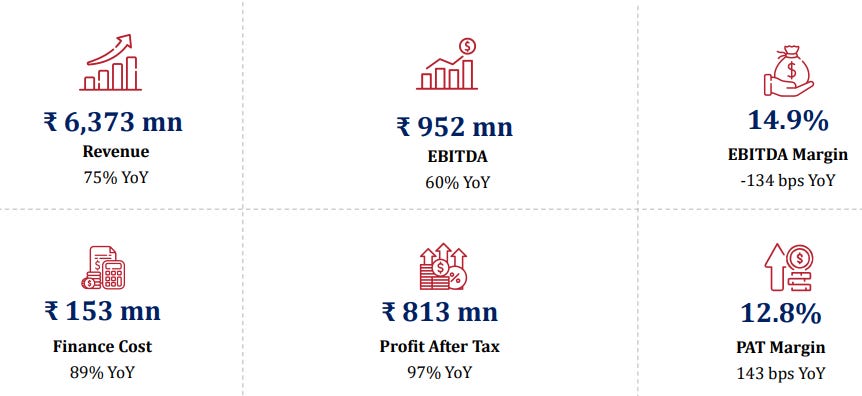

5. Strong Q4-24: PAT up 97% & Revenue up 75% YoY

PAT up 51% & Revenue up 46% QoQ

6. Strong FY24: PAT up 93% & Revenue up 60%

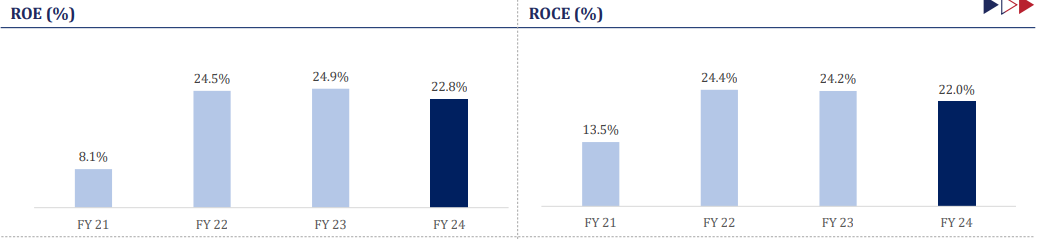

7. Business metrics: Strong return ratios

8. Outlook: 71% EBITDA & 60% revenue growth in FY25

i. FY25: Revenue growth of 60%

For the year 2025, we expect to clock a similar rate of growth in revenue greater than 60% and an improvement in operational EBITDA margin of more than 100 basis points.

ii. FY25: EBITDA growth of 71%

FY24 EBITDA margin of 14.1% expanding to 15.1% in FY25 on revenue growth of 60%, implies an EBITDA growth of 71%

improvement in operational EBITDA margin of more than 100 basis points.

iii. Strong revenue visibility: Order book 1.4X revenue expected for FY25

Revenue growth of 60% implies a expected revenue of Rs 2,888 cr in FY25. This implies that the order book of Rs 4,115 cr is 1.4X FY25 expected revenue.

Our current order book, which stands at Rs.41,152 million

iv. FY24-29: Long term revenue CAGR of 60%

KAYNES management is indicating towards for a longer term revenue CAGR of 60% for FY24-29 as a continuation of the historic momentum with the revenue CAGR of 60%

9. PAT growth of 93% & Revenue growth of 60% in FY24 at a PE of 141

10. So Wait and Watch

If I hold the stock then one may continue holding on to KAYNES

KAYNES has delivered a strong multi-year performance. On the back of this strong performance it is also guiding for a strong FY25, followed by a strong outlook for F24-29. One can continue riding the strong business uptrend which KAYNES is delivering.

11. Join the ride

If I am looking to enter KAYNES then

KAYNES has delivered PAT growth of 93% & Revenue growth of 60% in FY24 at a PE of 141 which makes the valuations quite expensive in the short term.

With a FY25 guidance of 60% revenue growth and 70% EBITDA growth at PE of 141, the valuations look fully priced from a FY25 perspective.

The opportunity will emerge over the longer term if the momentum of FY20-24 is sustained into to FY24-29. KAYNES management is quite confident on delivering on the FY24-29 outlook but 5 years is a long time and there may be volatility along the way.

Like our coverage on Kaynes Technology India Ltd? Please share it.