Kaynes Technology: PAT at 117% CAGR for FY20-23, 60-90% PAT growth in FY24 at 88 PE

Strong order flow. Executing orders that are higher value and leading to increased margin and higher profitability. To meet the growth, expanding to new facilities along with upgrading existing ones

1. A leading electronics manufacturing services provider

kaynestechnology.co.in | NSE : KAYNES

Founded in 1988 Kaynes Technology is a leading end-to-end IoT solution enabled integrated electronics manufacturing in India. KAYNES has capabilities across the entire spectrum of ESDM (Electronic System Design Manufacturing) services. KAYNES has experience in providing conceptual design, process engineering, integrated manufacturing and life cycle support for major players in automotive, industrial, aerospace and defense. KAYNES has a diversified portfolio of around 300+ customers in 26 countries across multiple industry verticals.

2. Growing at a blistering pace

PAT grew at 117% CAGR on a revenue growth of 45% for FY20-23

3. FY23: PAT up 128% on revenue growth of 59%

Our growth was largely led by strong demand in automotive, railway, IoT and consumer verticals.

4. Q1-24: PAT up 145% YoY on revenue growth of 49%

Our growth was largely led by strong demand in industrial, railway, IoT and IT, aerospace verticals and to some extent, automobile and EV.

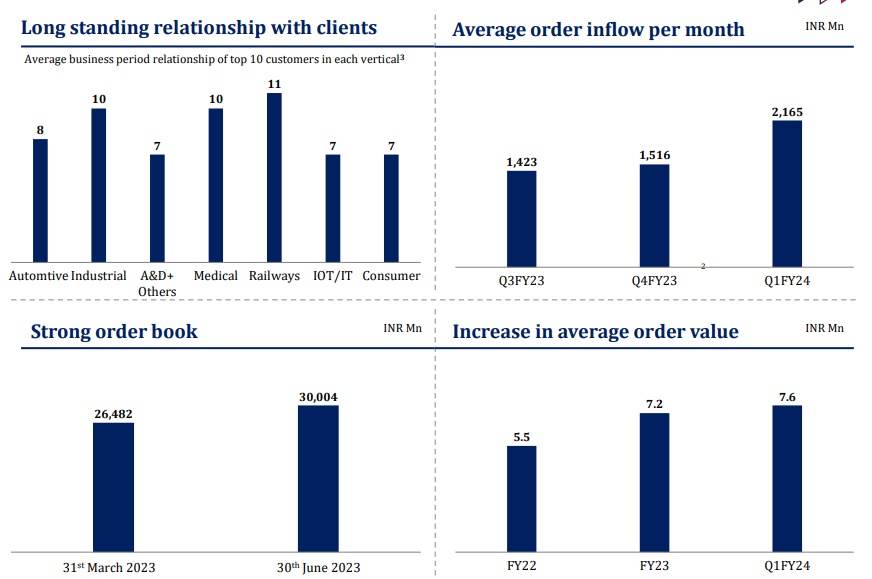

5. Revenue visibility: Order book 2.7X FY23 revenue

Quality of Rs 3,000 cr order book as on 30-Jun-23 improving

Order inflow per month increasing

Average order value increasing

6. Outlook:

i. Revenue to grow by 50-60% in FY24 vs Rs 1126 cr in FY23

For the year we are already saying that Rs. 1,700 to Rs. 1,800 crores is what we think we can do.

ii. PAT to grow by 60-90% in FY24

Average, you can expect 15% EBITDA and PAT around 9% to 10%.

A PAT margin of 9-10% on a revenue of Rs 1700-1800 cr in FY24 implies that PAT will be Rs 153-180 cr in FY24. This implies 60-90% growth in PAT over the Rs 95.2 cr PAT in FY23

7. 60-90%+ PAT growth in FY24 at a PE of 88

8. So Wait and Watch

If I hold the stock then one can definitely hold on to KAYNES as long as the blistering pace of growth continues. One should have the flexibility to patient if one weak quarter slip in between as PAT growth close to 100% can be quite challenging as the base increases.

9. Or, join the ride

If I am looking to enter the stock then

KAYNES has delivered a PAT CAGR of 117% for FY21-23 and has a guidance of 60-90% PAT growth for FY24 which makes the PE of 88 look reasonable.

In the medium term, the revenue visibility and the increasing run rate of order inflow ensures that the story based on current order book will continue at least till FY25

There is a long term story also in play given the capex plan of KAYNES

We have allocated INR 989 million towards CAPEX expansion and upgrade our facilities in Mysore, Manesar and Bengaluru and Chennai and acquired 1,20,000 square feet built up space in Manesar which is expected to be operationalized in the Q1 of this year. Additionally, we have year marked INR 1,493 million for investments into Kaynes Electronics Manufacturing Private Limited for setting up a new facility in Chamarajanagar Karnataka whose first phase to be operationalized by Q2 of this year.

Industry tailwinds will ensure that this is a long term story unfolding

India is now positioned as a global hub for electronic system design and manufacturing and we believe that we are rightly placed to capitalize this opportunity.

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades