Just Dial FY26: Value Play or Value Trap?

Cheap or value trap?. Balance sheet more valuable than market capitalization. Deep dive into Just Dial to understand and why the market isn’t assigning value

Just Dial’s services connect sellers of products & services with potential buyers/ users

justdial.com | NSE: Just Dial

1. Just Dial Trading at Attractive Valuations

Just Dial today presents a rare setup in the Indian market — a company where the balance sheet alone appears more valuable than the entire market capitalization.

1.1 Cash-Rich Balance Sheet

As of FY26, Just Dial holds ₹5,852 Cr in cash and investments on its balance sheet.

Against this, Just Dial’s market cap is ~₹4,865 Cr.

The market is valuing the core operating business at close to zero (or even negative) after adjusting for cash.

1.2 Valuation Snapshot

P/E ~10x → low for a profitable, debt-free business

Free Cash Flow Yield ~5.4% → reasonable, with room to improve

Debt: Zero → no balance sheet risk

Enterprise Value: Negative → cash exceeds market cap

This is deep value for a profitable business, trading at low multiples, with excess cash.

1.3 A Profitable Business — Not a Broken One

Despite the valuations, the operating business is not distressed:

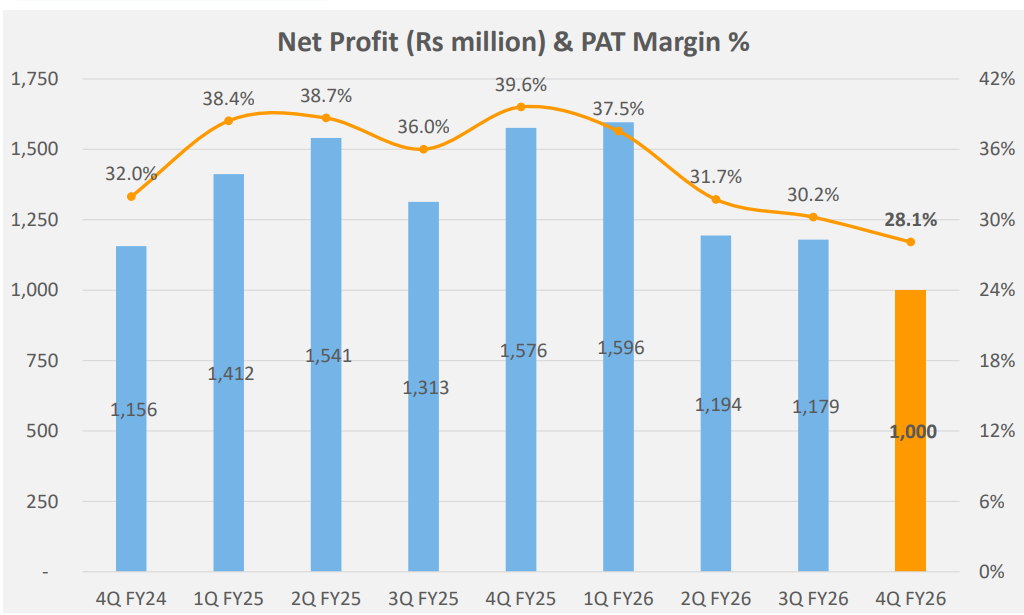

FY26 Operating EBITDA: ₹357 crore

EBITDA Margin: ~29.5%

It is a profitable, cash-generating platform that continues to add to its treasury.

1.4 What the Market Is Really Saying

When a business trades below its cash value, the market is effectively saying:

“We are not confident about the future of the operating business.”

So the real question is not — “Is Just Dial cheap?”

But: — “Why is the market unwilling to assign value to the business?”

2. Just Dial valuations: Value Trap or Deep Value?

2.1 Value Trap: Signs of Demand-Side Erosion

The thesis that the business is in structural decline and the “cheap” valuation is justified.

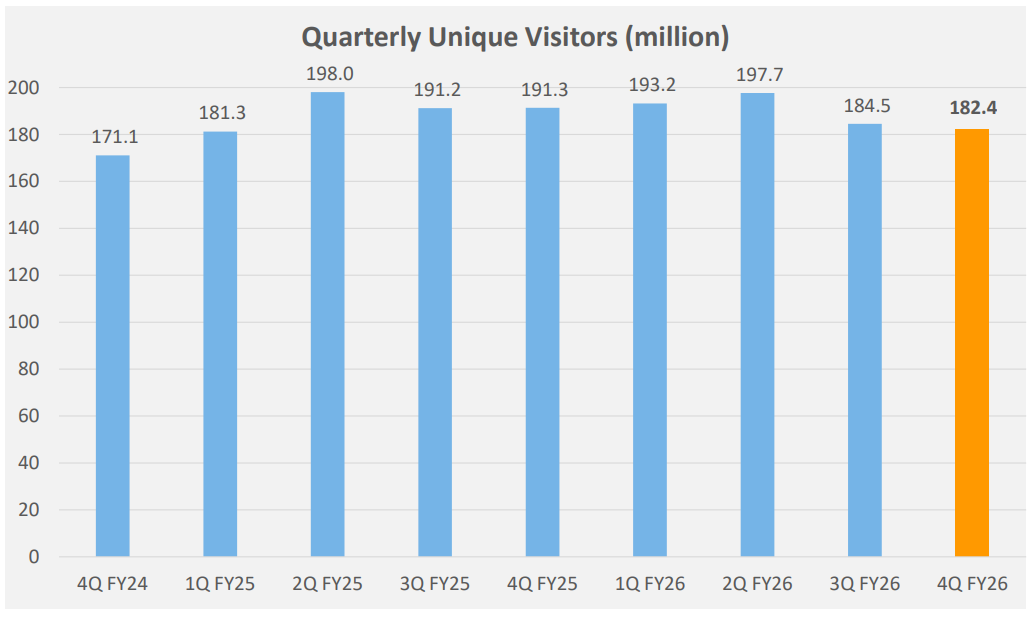

Traffic Is Declining — and Trending Down

The most alarming metric is the persistent decline in Unique Visitors.

Total visitors fell to 182.4 million in Q4 FY26, a 4.7% YoY decline from 191.3 million in Q4 FY25.

More importantly, this is not a one-off dip. Traffic has declined sequentially for multiple quarters, forming a clear downtrend.

In a marketplace business, traffic is the raw material. If it shrinks, everything else eventually follows.

The company has lost roughly 15.6 million quarterly visitors in just six months. This suggests that the post-pandemic digital surge has not only cooled off but is actually reversing for Just Dial.

This is the lowest traffic level in seven quarters, effectively erasing two years of growth. More concerning is the sequential “staircase” decline over the last three quarters, indicating that the drop is a trend, not a one-off seasonal dip.

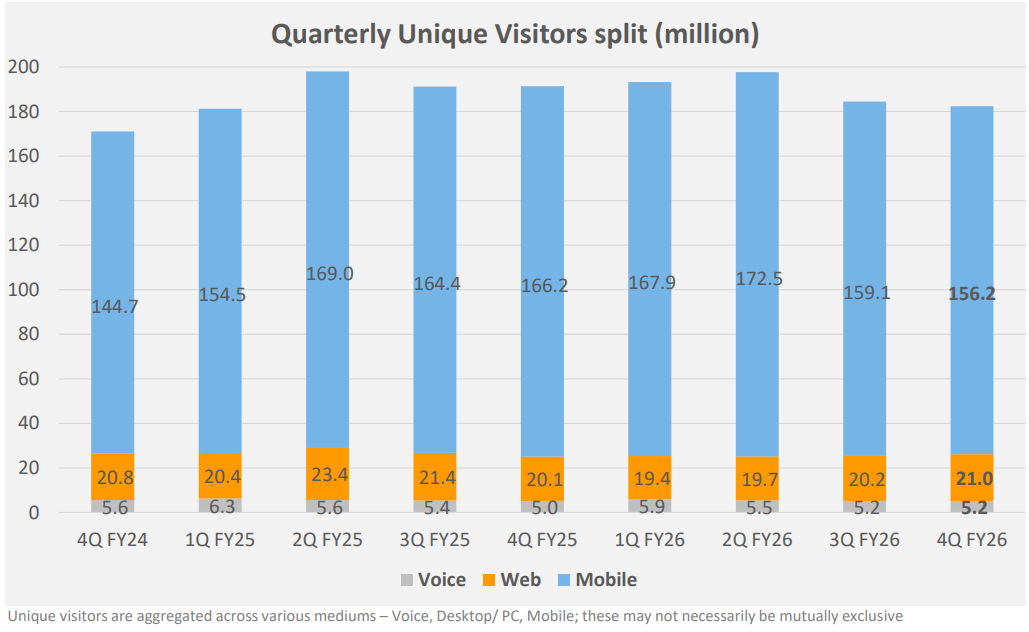

The Real Red Flag: Weakness in Mobile

The decline is concentrated where it matters most:

Mobile visitors dropped 6.0% YoY from 166.2 million (4Q FY25) to 156.2 million (4Q FY26).

Mobile accounts for ~86% of total traffic

That is a loss of 10 million mobile users in a single year. In an “App-First” economy like India, mobile traffic is the only traffic that truly matters for long-term survival.

A decline here suggests users are shifting to alternative platforms, not just slowing down.

Monetization Is Losing Momentum:

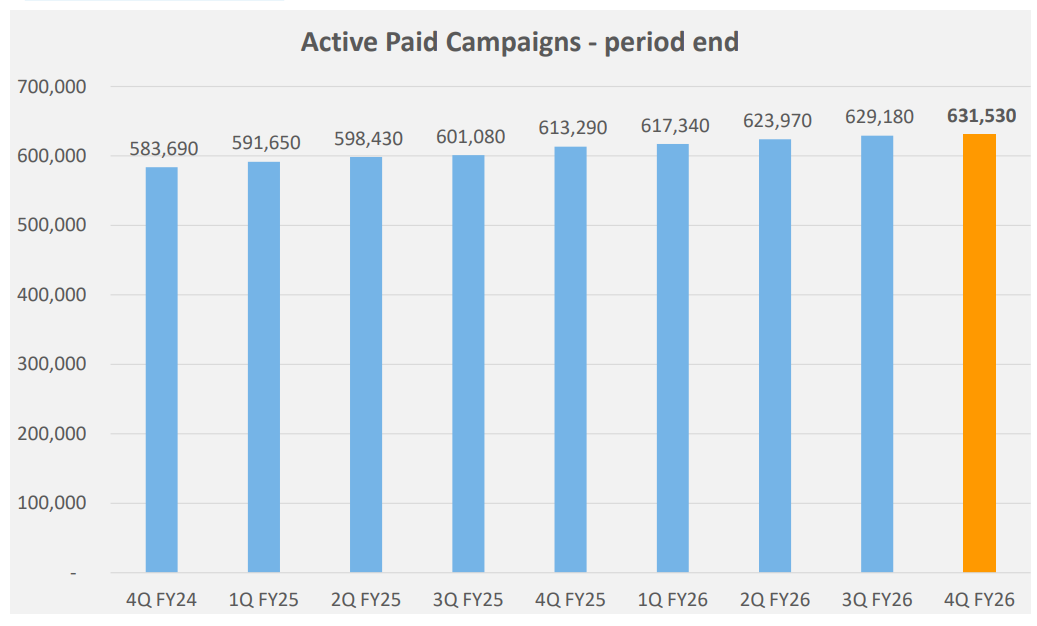

Active Paid Campaigns growth is Stalling

YoY Growth: 3.0% (631,530 vs 613,290).

QoQ Growth: 0.37% (631,530 vs 629,180).

While the number is technically at an “all-time high,” the velocity of growth has collapsed.

In 4Q FY25, the company added ~12,200 net new paid campaigns.

In 4Q FY26, they added only ~2,350 net new paid campaigns.

Quarterly addition has dropped by nearly 80% compared to the same period last year.

This matters because:

Merchants pay for leads & Leads depend on traffic

If traffic weakens, merchant ROI weakens — and that eventually shows up as higher churn or slower additions

What This Implies

Put together:

Overall Traffic is down

Mobile Traffic is down

Campaign growth slowing

The demand side of the business is weakening — even as the company remains profitable.

2.2 Value Play: A Business with Hidden Strength

Despite these concerns, dismissing Just Dial as a value trap may be premature.

Extreme Valuation Discrepancy (Negative EV):

Cash & Investments reached ₹5,852.2 Cr, while the Market Cap is only ~₹4,865 Cr.

The market is valuing the core business at minus ₹1,000 Cr.

Even if the business eventually dies, the cash alone provides a theoretical “floor” that is significantly higher than the current stock price.

High Profitability Provides Time

While margins are weakening on a relative basis — they are strong on an absolute basis

Just Dial is not in a crisis mode. It has the cushion to adapt, reposition, or integrate within a larger ecosystem.

Strong and Improving Supply-Side Assets

Total Listings grew 12.1% YoY to 54.7 million.

Listings with Geocodes (essential for map-based search) grew 25.4%.

While traffic is down, the “inventory” of data is growing rapidly. This deep database of Indian SMEs is a unique asset that is difficult for a newcomer to replicate.

Reliance Backing Creates Optionality

Promoter Reliance Retail Ventures Ltd (RRVL) holds 63.84% of the company.

The long-term value may not come from Just Dial as a standalone app, but as

the backend infrastructure for SME commerce.

the “discovery layer” for the Jio/Reliance Retail ecosystem.

3. Conclusion: Cheap for a Reason or Mispriced?

Just Dial is not an easy stock to classify.

On one hand, it is undeniably cheap:

Cash exceeds market cap

The business is profitable

Valuations are low across metrics

On the other hand, the core engine is weakening:

Traffic is declining

Mobile engagement is slipping

Monetization growth is slowing

The Tie-breaker:

Two factors will determine whether this becomes a value trap or a value opportunity:

Demand Stabilization

Capital Allocation — If the board announces an acquisition to drive growth or return the ₹5,852 Cr via dividend or buyback to to shareholders.

If they keep the cash idle, it remains a “Value Trap” indefinitely.

Management Commentary on Capital Allocation in Q4 FY25 Earnings Call: So, at this point of time, this particular agenda on returning cash via, say, dividend has not been taken up. We expect the same to be taken up sooner, most likely by next quarter, hopefully, we should be freezing on a proper capital allocation policy via most likely by dividend because that is a more tax-efficient way rather than buyback at this point of time.

The "Watch-out" for Q4 FY26 Call:

The most important question for the Q4 FY26 earnings call not only about "Traffic"—it is "What is the specific date for the implementation of the Capital Allocation Policy?" If management remains vague again (as they were in FY25), the "Value Trap" label will likely stick for another year.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer