Jindal Saw: PAT growth of 49% & revenue growth of 7% in H1-25 at a PE of 11

Good H1-25 with muted top-line. Indicating towards a solid FY25. Strong order book provides revenue visibility into FY25. Margins to be supported by debt repayment & reduction in interest cost.

1. Manufacturer of Iron & steel pipe products, pipe-accessories and pellets

jindalsaw.com | NSE : JINDALSAW

Pipes and tubes: like Welded Pipes Above 16" Diameter, Rust-free Iron Pipes, Non-welded pipes for industrial purposes, Welded and Non-welded Pipes of different Stainless-Steel grades

Anti-corrosion and protective coating facilities along with the necessary ancillaries like fittings, bends, flanges etc. to make it a total pipe solution provider.

The company also produces and sells Pellets.

Substantial contribution to revenue is coming from drinking water supply and sanitation (WSS) which is growing rapidly in India and globally. The company’s exposure to the Oil & Gas sector accounts for only one fourth of the total revenue.

2. FY20-24: PAT CAGR of 36% and Revenue CAGR of 16%

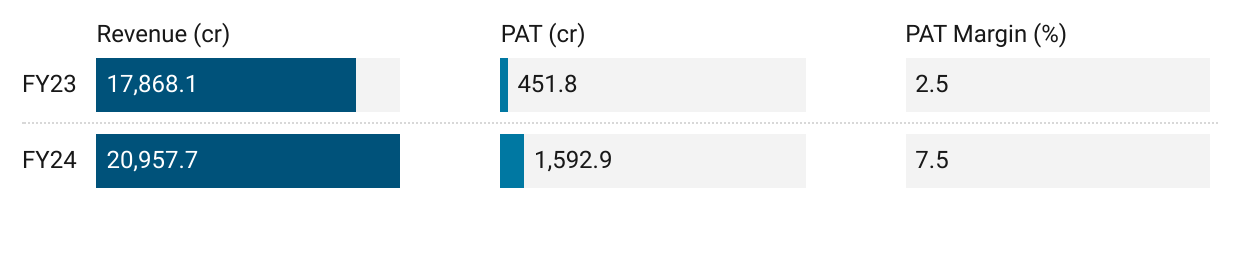

3. Strong FY24: PAT 253% & Revenue up 17% YoY

4. Q2-25: PAT 34% & Revenue up 2% YoY

PAT 14% & Revenue up 13% QoQ

5. H1-25: PAT 49% & Revenue up 7% YoY

6. Business metrics: Improving return ratios

7. Outlook: 10-15% revenue growth in FY24

i. FY25: 10-15% volume growth

FY25 guidance of 10-15 volume growth. Based on H1-25 volume growth one has to deliver a strong H2-25 to meet the FY25 guidance.

ii. Margin improvement: EBITDA Margin from 15% to 16-17% in FY25

H1-25 EBITDA margin is in line with the 16-17% guidance for FY25.

The Company continued to enhance its year-on-year performance supported by additional capacities from acquisition and merger of Sathavahana Ispat Limited operations, as well as improved execution of large export orders, leading to higher turnover and margins. Additionally, stable raw material prices and value-added product mix have contributed towards margin improvement across all products

iii. Strong revenue visibility: Order-book to be executed in 3-4 quarters

The current order book of Jindal Saw Limited (at Standalone level) for Iron & Steel pipes and pellets is ~US$ 1.62 billion, the break-up is as under:

Iron & Steel Pipes: US$ 1,573 million

Pellet: US$ 45 million

FY25: We are booked for most of the year

The order book gives a visibility of appx. 3-4 quarters.

iv. Strong free cash generation: CAPEX not required for growth in FY25

Absence of capex reflecting in the strong free cash flow of Rs 1,700 cr+ generated in FY24. The trend is continued in H1-25 where Rs 414 cr of free cash flow has been generated.

We are carrying out modernization, but there is no major projects that has been announced on the horizon. So we expect the capex -- so, if you see the way the cash flows, there would be a lot of free cash flow is what we are expecting to come out of the would be largely used to pay for capex, pay for loan, use it for shareholder distribution.

8. PAT growth of 49% & Revenue growth of 7% in H1-25 at a PE of 11

9. Hold?

If I hold the stock then one may continue holding on to JINDALSAW.

Continuing forward the momentum of FY24, a strong H1-25 has been delivered with solid PAT growth even though top-line growth was muted.

The management expects the momentum to carry on for another 12-15 months.

The present pace of execution affords visibility of performance for the coming 12-15 months with further order enquiries building up indicative of sustained momentum.

The growth outlook, EBIDTA margin expansion, order book visibility and industry tailwinds give reasons to stay in the stock.

The order book gives a visibility of appx. three quarters even though few orders may be executed in the next 9-12 months period.

The Company expect the business environment to remain positive in the upcoming quarters despite the volatile geopolitical situation in the MENA and GCC region.

Reduction in interest cost on account of debt reduction will provide strength to margins and indicating towards strong cash flow generation to support repayment of debt.

The Company has further prepaid Rs. 2,000 million term loans in October 2024 and intends to prepay an additional Rs. 2,500 million in the next few months.

10. Buy?

If I am looking to enter JINDALSAW then

JINDALSAW has delivered PAT growth of 49% & Revenue growth of 7% in H1-25 at a PE of 11 which makes valuations quite attractive.

JINDALSAW at a market cap of about Rs 21,959 cr against H1-25 networth of Rs 10,135 cr means that it is available at a price to book of 2.2 makes the valuations quite attractive.

Outlook for 10-15% volume growth with EBIDTA margin expansion to 16-17% would deliver bottom line growth closer to 20% in FY25 which at a PE of 11 makes valuations look attractive.

JINDALSAW generated free cash flow of Rs 413.75 cr in H1-25 on a current market cap Rs 21,959 cr, implies that its available at a free cash flow yield of 1.9% (not annualized) which makes the valuations quite reasonable.

Previous coverage on JINDALSAW

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer