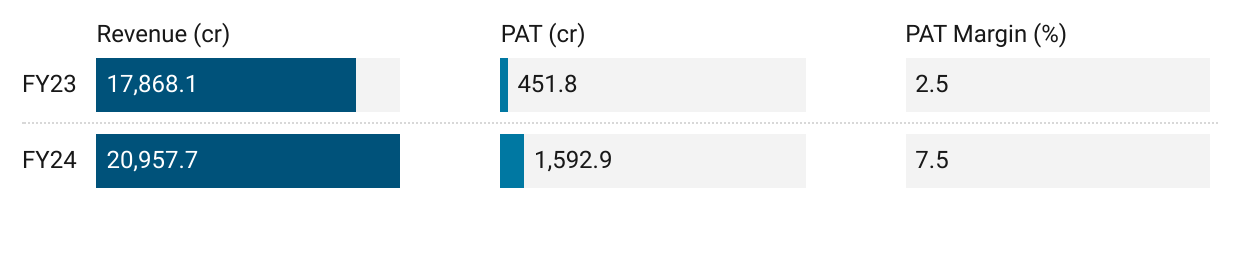

Jindal Saw: PAT growth of 253% & revenue growth of 17% in FY24 at a PE of 11

At P/B of 1.7 & free cash flow yield of 10%+ JINDALSAW looks attractive in terms of valuations. JINDALSAW is riding industry tailwinds and its order book provides revenue visibility into FY25.

1. Manufacturer of Iron & Steel pipe products

jindalsaw.com | NSE : JINDALSAW

Business Segments

Saw Pipe: Manufacturing LSAW & HSAW pipes in 6 pipe mills in India

DI Pipes & Pig Iron: 3rd largest producer of DI Pipes globally with plants in India & Abu Dhabi (UAE).

Seamless Pipes

Carbon & alloy steel pipes & stainless steel (including stainless seamless pipes & Tubes and stainless welded pipes & tubes)

Entered in a JV with Hunting Energy Pte. Ltd (49%) to set up precision machine shop for premium connections. JV to start production in next financial year i.e. 2024.

Iron Ore Mines and Pellet: Low grade iron ore mine with iron ore beneficiation & pellet plant at the mine head

2. FY20-24: PAT CAGR of 36% and Revenue CAGR of 16%

3. FY23: PAT up 20% and Revenue up 34% YoY

4. Strong 9M-24: PAT 648% Revenue up 22% YoY

5. Q4-24: PAT 61% & Revenue up 5% YoY

6. Strong FY24: PAT 253% & Revenue up 17% YoY

7. Business metrics: Improving return ratios

8. Outlook: 10-15% revenue growth in FY24

i. FY25: 10-15% volume growth

FY24 growth of 34% was on account M&A activity related to Sathavahana Ispat Limited. However FY25 volume growth would be around 10-15%

ii. Margin improvement: EBITDA Margin from 15% to 16-17% in FY25

Margin improvement on a top-line growth of 10-15% could drive bottom-line growth closer to 20%

iii. Strong revenue visibility: Order-book to be executed in 3 quarters

The current order book of the Company (for Iron & Steel pipes and pellets) is ~US$ 1.53 billion (Previous quarter ~ USD 1.49 billion) the break-up is as under:

Iron & Steel Pipes: US$ 1,509 million

Pellet: US$ 16 million

FY25: We are booked for most of the year

iv. Strong free cash generation: CAPEX not required for growth in FY25

Absence of capex reflecting in the strong free cash flow of Rs 1,700 cr+ generated in FY24.

We are carrying out modernization, but there is no major projects that has been announced on the horizon. So we expect the capex -- so, if you see the way the cash flows, there would be a lot of free cash flow is what we are expecting to come out of the would be largely used to pay for capex, pay for loan, use it for shareholder distribution.

9. PAT growth of 253% & Revenue growth of 17% in FY24 at a PE of 11

10. So Wait and Watch

If I hold the stock then one may continue holding on to JINDALSAW.

Coverage of JINDALSAW was initiated after Q1-24 results. The investment thesis has not changed after a strong FY24. It has increased the confidence in the management to deliver a stronger FY25

The management expects the momentum to carry on for another 12-15 months.

The present pace of execution affords visibility of performance for the coming 12-15 months with further order enquiries building up indicative of sustained momentum.

The growth outlook, EBIDTA margin expansion, order book visibility and industry tailwinds give reasons to stay in the stock.

The order book gives a visibility of appx. three quarters even though few orders may be executed in the next 9-12 months period.

We expect the business scenario to remain positive in the coming quarters despite the volatile geopolitical situation in the MENA and GCC region.

11. Or, join the ride

If I am looking to enter JINDALSAW then

JINDALSAW has delivered PAT growth of 647% & Revenue growth of 22% in 9M-24 at a PE of 11 which makes valuations quite attractive.

Outlook for 10-15% volume growth with EBIDTA margin of 16-17% would deliver bottom line growth closer to 20% in FY25 which at a PE of 11 makes valuations look reasonable.

JINDALSAW at a market cap of about Rs 16,714 cr against FY24 sales of Rs 20,000 cr+ means that it is available at a market cap to sales of less than 1

A net-worth of Rs 10,000 cr+ on a market cap of about Rs 16,714 cr, implies that its available at a price to book of 1.7 which makes the valuations quite attractive.

JINDALSAW generated free cash flow of Rs 1,729.92 cr on a market cap Rs 16,714 cr, implies that its available at a free cash flow yield of 10.3% which makes the valuations quite attractive.

Previous coverage on JINDALSAW

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer