JD Cables FY26 Result: PAT up 44%, Strong Guidance till FY28

Guiding 50-60% revenue growth with stable margins. JD Cables looks cheap on forward valuations. Risk if ambitious growth FY27 not delivered as per guidance

1. Cables & Conductors + Power EPC Projects

jdcables.in | BSE - SME: 544524

Core business: cables, wires and conductors

In FY26, the business is dominated by cables and wires.

Cables & Wires~76%

Aluminium Conductors~24%

JD Cables sells mainly into the power infrastructure ecosystem. Its customer universe includes:

State electricity boards / DISCOMs

EPC contractors

Infrastructure companies

Utilities

Industrial customers

Power transmission and distribution projects

Management said they are majorly supplying to EPC contractors and are also participating directly in government tenders for cable supply.

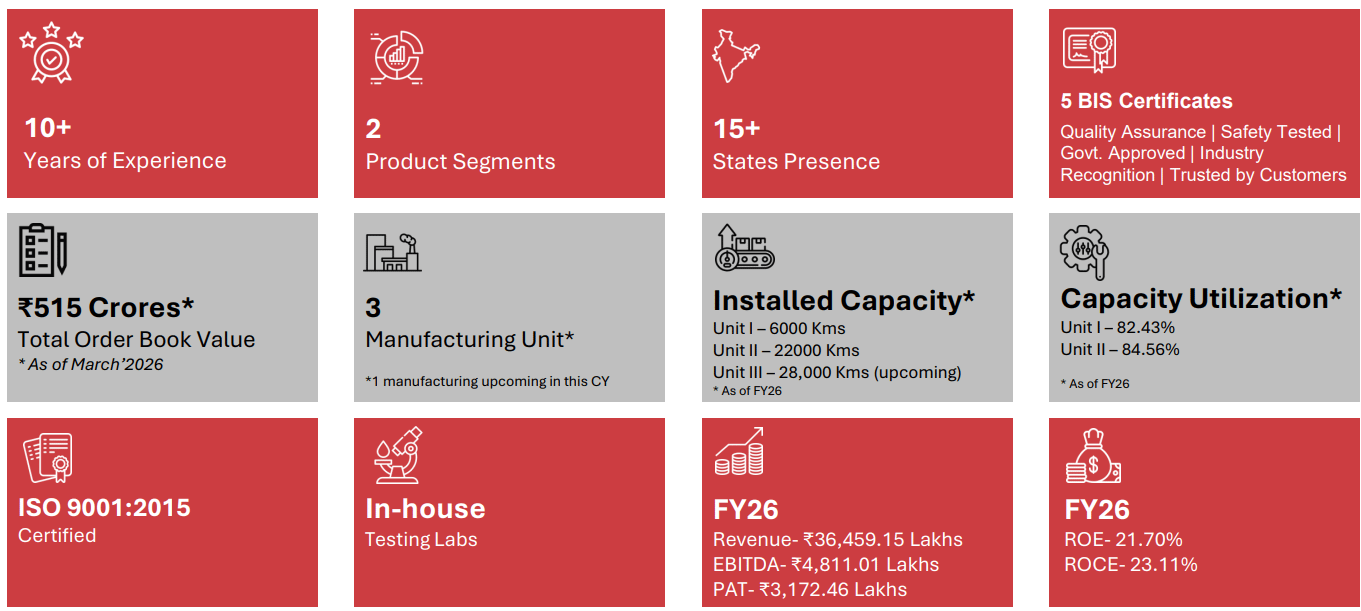

JD Cables has two operating production facilities with combined installed capacity of around 28,000 km per annum — 6,000 km at Unit I and 22,000 km at Unit II.

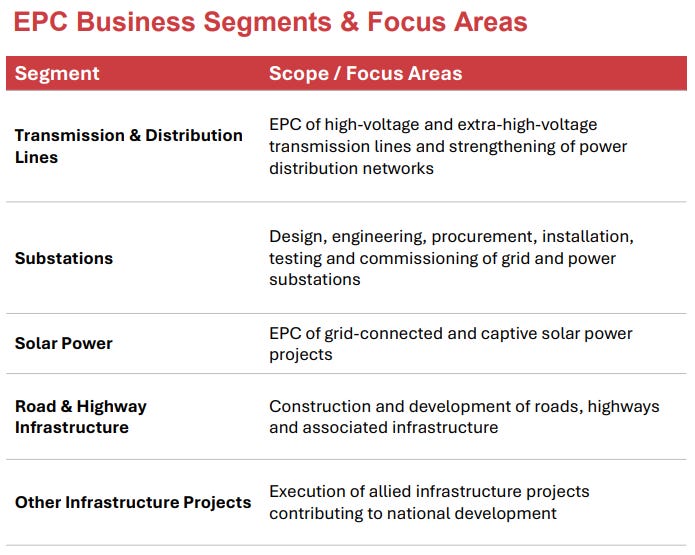

New business: EPC / infrastructure projects

JD Cables is expanding beyond manufacturing into EPC.

So JD Cables is becoming:

Earlier: cable/conductor manufacturer

Now: cable/conductor manufacturer + EPC/infrastructure contractor

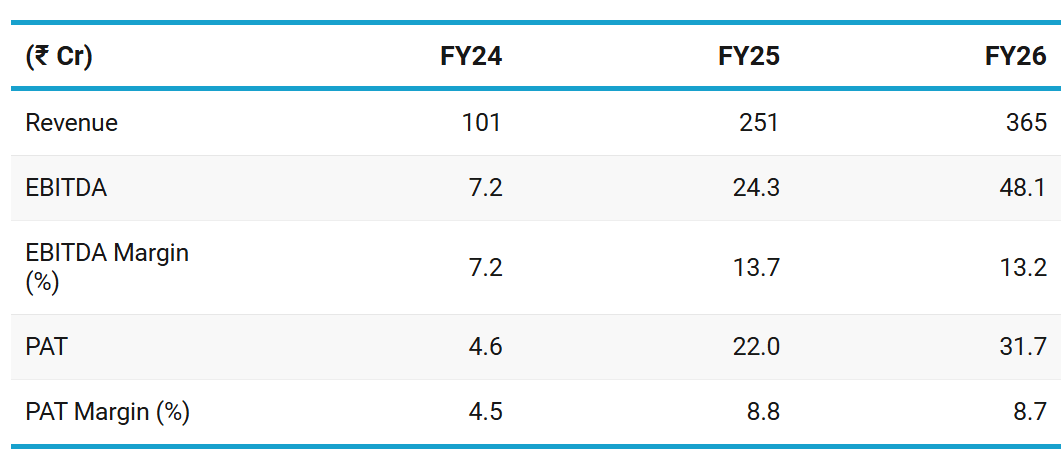

2. FY24-26: PAT up 163% & Revenue up 90% CAGR

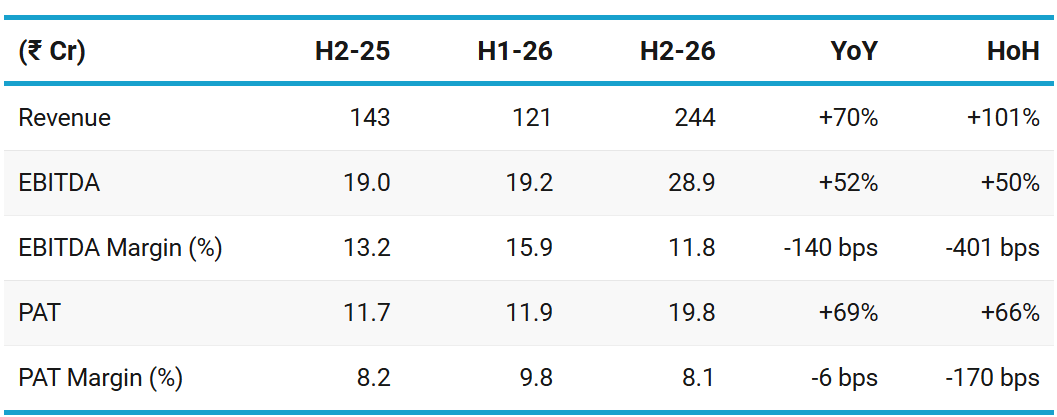

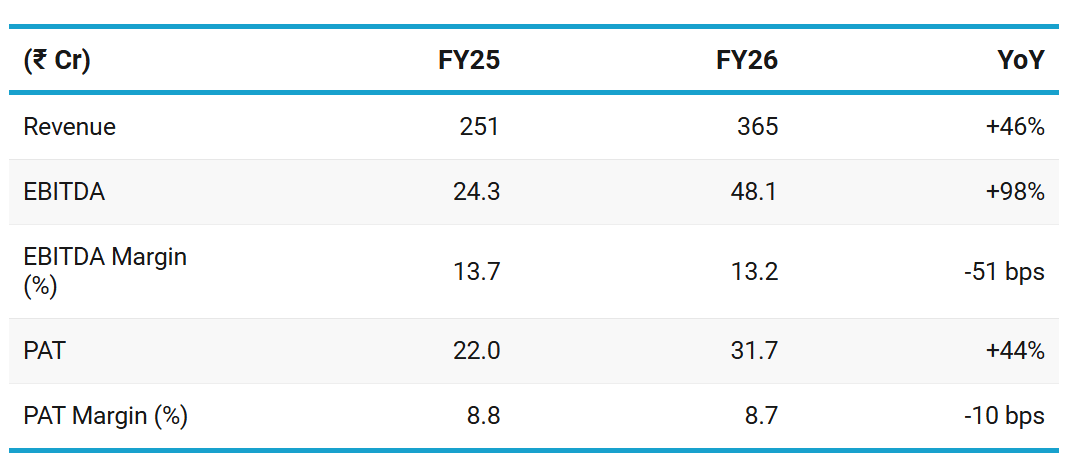

3. H2 FY26: PAT up 69% & Revenue up 70% YoY

PAT up 66% & Revenue up 101% HoH

EBITDA margin fell from H1 FY26 level because of higher other expenses, EPC-related costs, and bulk-supply execution.

Other expenses increased because the company started the EPC business and incurred expenditure where bills/invoices were pending.

Raw material ratio actually improved, so margin pressure was not from raw material

4. FY26: PAT up 44% & Revenue up 46% YoY

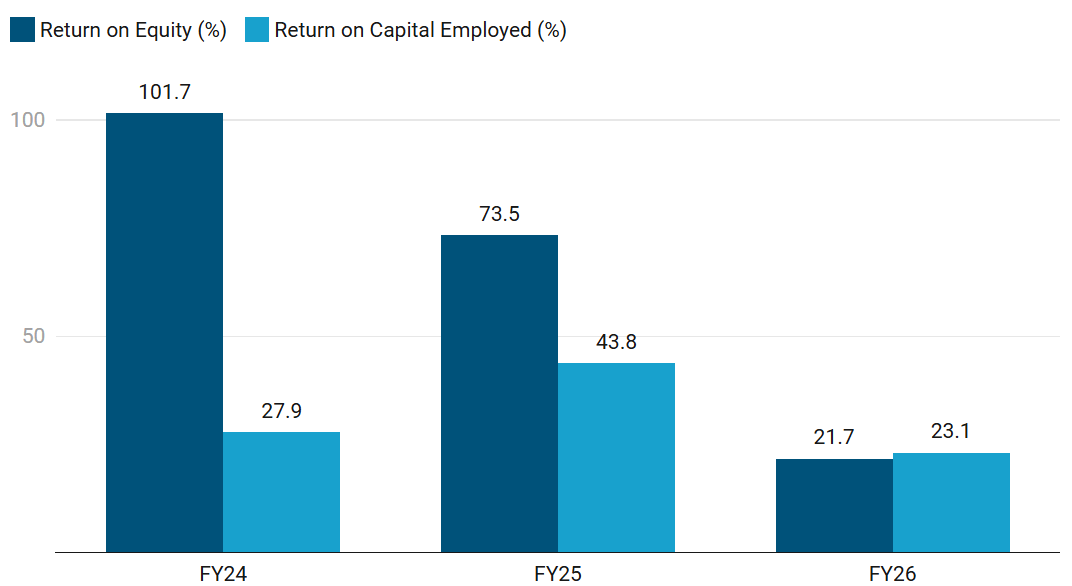

5. Business Metrics: Stable Return Ratios

ROE: still healthy, but no longer extraordinary.

Fall is mostly because of IPO-led net-worth expansion.

ROCE: more important to watch.

FY26 ROCE of 23.11% is good, but the decline from 43.84% shows capital efficiency has reduced after expansion.

IPO money increased capital employed before full earnings came in.

New facility/capex has not yet fully ramped up.

Working capital increased due to fast growth and EPC entry.

H2 margins declined versus H1, which reduced operating return on capital.

EPC business can be more capital-intensive, so ROCE may stay under pressure if execution is not cash-efficient.

6. Outlook: Growing at 50-60%+ CAGR

6.1 FY27 Guidance

FY27 revenue growth

50–60% revenue growth in FY27.

Expect similar 50–60% growth even in FY28

Core cables & conductors growth

Expected to grow 30–40% in FY27.

EPC is the accelerator on top.

EPC revenue

Expects minimum ₹200 Cr from EPC in FY27 — can go higher (₹30 Cr in FY26)

Order book

₹515 Cr / ₹500 Cr+ as of March 2026.

Order-book execution timeline is usually around 1.5 years.

FY27-end order book target — at least ₹700–800 Cr by FY27 end, calling this a conservative expectation.

Tender pipeline — ₹1,000 Cr+ tenders, across EPC and cables, with outcomes pending.

Margins — 12–13% EBITDA margin

EPC margin — Expectation is around 8%, but management said exact margin can be confirmed once project completion advances.

New products margin:

Newer products such as HTLS, AL-59, MVCC and HT cables are expected to have better margins than existing products and management expects these margins to be double digit.

Capacity ramp-up:

Conductor division is ready and awaiting electricity connection; cable division expected to start in the next two months.

New unit to operate at a good pace by September and reach 70–80% utilization next year.

Longer-term capacity ambition

Capacity can be expanded 3x–4x within the next two years, depending on order book and demand.

Capex

FY27 capex guidance is around ₹20–30 Cr, depending on order inflow and new-unit ramp-up.

Company is also procuring adjacent land near the new factory.

JD cables is growing into a ~₹1,000 Cr revenue company by FY29, driven by three levers:

Core cables/conductors growing 30–40%

EPC scaling from ₹30 Cr to ₹200 Cr+

New Dankuni capacity and new products supporting higher volumes

This is no longer a simple cable/conductor capacity expansion story. FY27 growth now depends heavily on EPC execution, working-capital funding, and tender conversion.

Order book, capacity expansion, and tender pipeline support the growth narrative.

Margins are guided closer to 12–13% EBITDA, not the H1 FY26 level of ~16%; EPC can absorb cash; and management openly accepts that high growth can keep cash flows under pressure.

6.2 FY26 Performance vs FY26 Guidance

FY26 vs guidance: mostly positive, but not perfect.

Growth and order book: delivered / ahead

Margins: lower than H1 run-rate

Capacity expansion: delayed

EPC entry: stronger than expected

Cash flow / working capital: watch closely

7. Valuation Analysis — JD Cables

7.1 Valuation Snapshot

Current Market Price — ₹244.05

Market cap — ₹ 550.36 Cr

Assumptions — lower end of the 50-60% growth till FY28

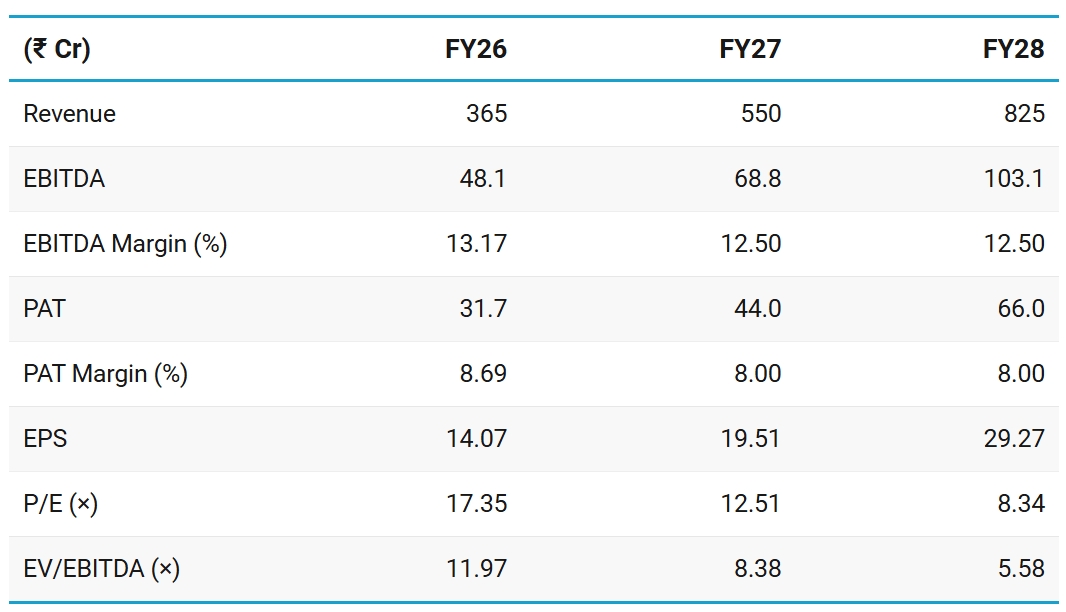

On FY26 actuals, the stock trades at: 17.4× P/E, 12× EV/EBITDA, 1.5× sales

That is a fair-to-slightly-rich trailing valuation for a small SME-listed company with rising EPC exposure.

On FY27 guidance, the valuation falls sharply which makes it attractive.

On FY28 guidance, it becomes optically cheap at 8.3× P/E, 5.6× EV/EBITDA, 0.7× sales

It is cheap only if three things happen:

Revenue growth actually lands at 50–60%.

EBITDA margin stays around 12–13%.

EPC growth does not destroy cash flow.

The biggest risk is working capital + debt + EPC execution.

Management has already acknowledged that growth can pressure cash flows, especially because debtor and inventory days rise during rapid expansion.

7.2 Opportunities at Current Valuation

Valuation looks ordinary on FY26, but attractive if FY27/FY28 growth comes through.

Strong earnings growth can make current valuation look cheap

If guidance is delivered the valuations are not demanding for a company growing at 50-60% with revenue scaling to ₹1,000 Cr by FY29.

Order book gives revenue visibility

If execution is smooth, FY27 revenue visibility is stronger than what a normal small manufacturing company would have.

EPC can create a step-change in scale

The biggest upside lever is EPC.

The core cables and conductors business can grow 30–40%, while overall revenue growth is expected at 50–60%.

Capacity expansion supports growth

Existing two units were already operating at high utilization: 82.43% at Unit I and 84.56% at Unit II in FY26.

Upcoming Unit III with 28,000 km capacity, effectively creating a major capacity expansion runway.

New unit to run at a good pace by September and reach 70–80% utilization next year.

New capacity comes onstream just as order book and EPC revenue are scaling.

New products can improve the quality of growth

Newer products should have better margins than existing products

If growth comes only from lower-margin EPC, valuation may not rerate much.

But if new products contribute meaningfully and margins stay healthy, the market can value JD Cables more like a growing cables/conductors platform rather than just a contractor.

8.3 Risks at Current Valuation

If execution slips, the valuation is no longer cheap.

Growth guidance is aggressive

Guiding for 50–60% revenue growth till FY28

That is a big ask for a company with a limited track record in public markets

If growth comes in at 25–30% instead of 50–60%, the stock can quickly move from “cheap forward valuation” to “fairly valued small-cap.”

Margin has already softened

In the latest call, management accepted that the sustainable margin expectation is now around 12–13% EBITDA, not the earlier H1 FY26 level of ~15–16%.

If the market is valuing JD Cables as a high-growth manufacturing company, then margins matter.

If EPC becomes a larger part of the mix, the business may grow faster while margins stay lower.

EPC can grow revenue but hurt cash flow

EPC can scale revenue quickly, but it usually brings:

execution delays,

billing milestones,

retention money,

receivable build-up,

inventory build-up,

higher working-capital requirement,

lower margin visibility.

Management itself acknowledged that growth and EPC can keep cash flow negative, because debtor and inventory days rise in a 50–60% growth phase.

So the risk is: PAT grows, but cash does not.

Debt risk can rise in FY27

Management said they may take bank debt to fund working capital and EPC execution if they win more tenders.

JD Cables becomes a business where:

revenue grows → receivables grow → debt grows → interest cost grows → PAT quality weakens

New capacity execution risk — new facility important for FY27 growth.

The conductor division ready but awaiting electricity connection

The cable division expected to start byJul/Aug 26

Any delay in can push revenue into later quarters.

At this valuation, the market may not tolerate delayed capacity ramp-up.

Tender conversion is not yet proven at larger scale

Management has participated in ₹1,000 Cr+ tenders, but also said conversion ratio is difficult to state because this is a relatively newer area of participation for them.

This creates uncertainty while valuation assumes JD Cables winning and executing large orders.

If tender wins are delayed or conversion is lower, the forward valuation case weakens.

Help your group stay ahead. Share now!

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer