Jai Balaji Industries: PAT growth of 1422% & revenue growth of 5% in FY24 at a PE of 18

Revenue growth of 25-30% in FY25. EBITDA margin expansion to 17-18% provides strong outlook for FY25. JAIBALAJI undergoing capex till FY26 providing a roadmap for longer term growth

1. Manufacturers of DI Pipes & Specialized Ferro Alloys

jaibalajigroup.com | NSE: JAIBALAJI

Jai Balaji Industries is an integrated steel products company specialising in value-added products like ductile iron pipes and specialised ferroalloys.

Currently we have around 9% to 10% of the DI pipe market share of India and our aim is to reach 18% to 20% of the market share post our capacity expansion plans.

One of the largest producers of Specialized Ferro Alloys in India

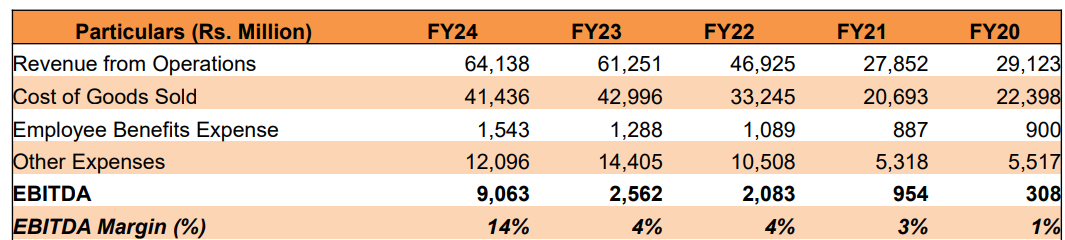

2. FY20-24: EBIDTA CAGR of 133% & Revenue CAGR of 22%

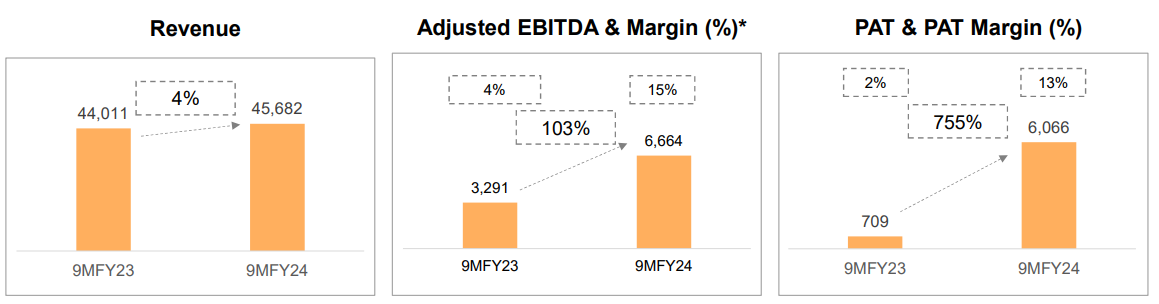

3. Strong 9M-24: PAT 755% Revenue up 4% YoY

4. Q4-24: Back to Profitability & Revenue up 7% YoY

5. Strong FY24: PAT 1422% & Revenue up 5% YoY

6. Business metrics: Strong & Improving return ratios

Becoming net debt free company in next 12-15 Months and strengthening the Balance Sheet

7. Outlook: 25-30% revenue growth in FY25

For FY '25, we anticipate revenue growth in the region of 25% to 30%, EBITDA margins of around 17% to 18% and the net debt to be reduced to a range of around INR225 to INR250 crores.

The capital expenditure is also expected to be in the range of INR300 to INR250 crores and we expect the ductile iron pipe production to exceed INR4 lakh tons.

With a focus on increasing the contribution of value-added products for margin expansion, we expect DI to contribute 45% to 50% and Ferroalloys to contribute around 35% of our total volumes by FY '25 '26.

8. PAT growth of 1422% & Revenue growth of 5% in FY24 at a PE of 18

9. So Wait and Watch

If I hold the stock then one may continue holding on to JAIBALAJI.

JAIBALAJI has delivered a strong turnaround in FY24 after a lackluster FY21-23. It has increased the confidence in the management to deliver a stronger FY25 based on the strong guidance for FY25.

FY '24 has been a very eventful year for us. We have achieved record high financial performance, marking the highest ever in the history of our company.

The bottom line is expected to grow faster than top-line given that EBITDA margin is expected to expand from 14% in FY24 to 17-18% in FY25

Capacity Expansion Plans are in place to support growth till FY26. Volume CAGR of 48% for DI pipes for FY24-26. Volume growth of 14% for Ferro Alloys for FY24-25.

10. Or, join the ride

If I am looking to enter JAIBALAJI then

JAIBALAJI has delivered PAT growth of 1422% & Revenue growth of 5% in FY24 at a PE of 18 which makes valuations quite reasonable.

FY25 guidance for 25-30% volume growth with EBITDA margin expansion to 17-18% implies EBITDA growth of 40-54% at a PE of 18 makes valuations look attractive from medium term.

Outlook for FY24-26 volume CAGR of 48% for DI pipes for FY24-26 provides a roadmap for growth over the longer term.

JAIBALAJI generated free cash flow of Rs 459 cr on a market cap Rs 16013 cr, implies that its available at a free cash flow yield of 2.9% which is positive that its generating free cash flow at the time of an ongoing capacity expansion.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer