IREDA: 30% PAT growth & 32% revenue growth in Q1-25 at a PE of 55

Guiding for 34% AUM growth for FY24-30. The runway for growth is both long and steep. However valuations are not cheap and have priced in a lot of the future growth.

1. India’s largest pure-play green financing NBFC

ireda.in | NSE: IREDA

2. FY20-24: PAT CAGR of 55% & EPS CAGR of 17%

Dilution of equity base as seen from the EPS CAGR trailing PAT CAGR

3. Strong FY-24: PAT up 45% & Revenue up 43%

4. Strong Q1-25: PAT up 30% & Revenue up 32%

5. Strong and improving return ratios

6. Outlook: AUM growth of 34% for FY24-30

Revenue from operations targets were declared in Aug-23 and hence the numbers look very conservative.

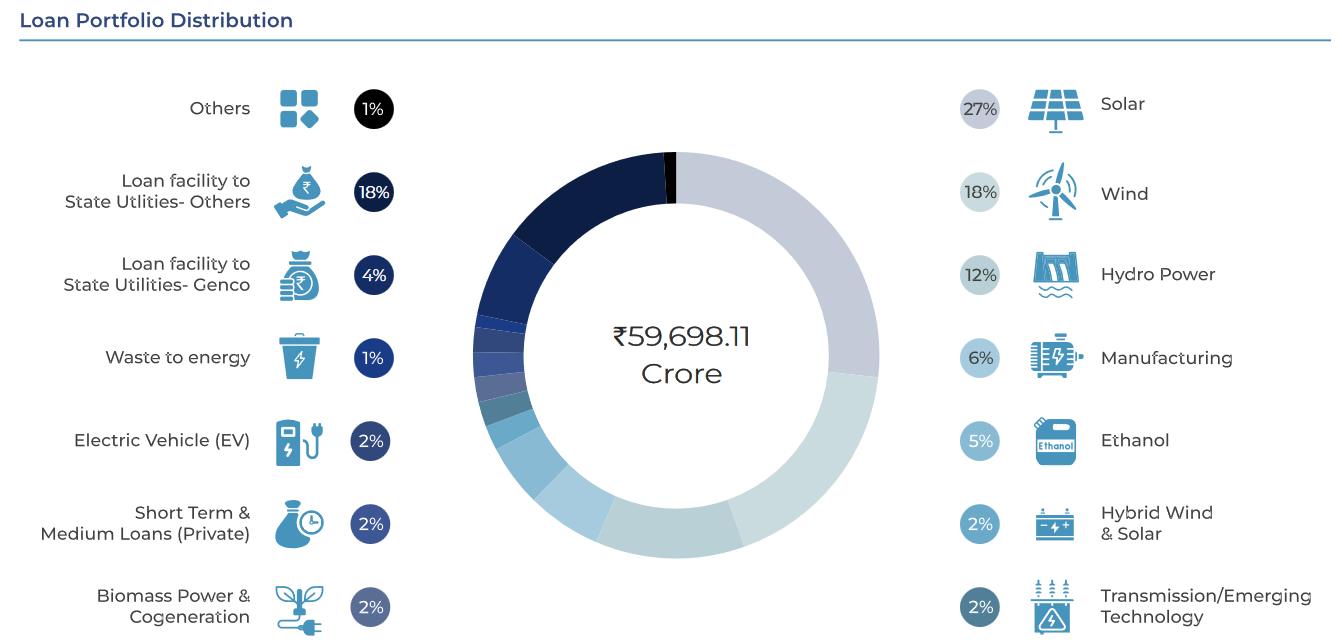

AUM growth to Rs 3,50,000 cr by FY30 from Rs 59,698 cr implies a CAGR of 34% for FY24-30

7. PAT growth of 30% & Revenue growth of 32% for Q1-25 at a PE of 55

8. So Wait and Watch

If I hold the stock then one may continue holding on to IREDA

IREDA has achieved a strong FY24 and beaten the revenue targets for FY24. It has followed it up with a strong Q1-24.

IREDA has a strong outlook with the management guiding for 30%+ AUM growth for FY24-30

IREDA will dilute the shareholders and this will impact the EPS growth. One needs to watch out for the FPO and take a call based on the pricing.

9. Or, join the ride

If I am looking to enter IREDA then

IREDA has delivered a strong Q1-25 with PAT growth of 30% & revenue growth of 32% at PE of 55 which makes the valuations quite rich in the short term.

IREDA had a networth of Rs 9,110 cr as of Q1-25 end on a current market cap of Rs 77,775 cr. It is quoting at a price to book of 8.5 which makes it quite expensive in the short term.

The outlook for AUM growth of 34%+ for FY24-30 provides a very long runway for growth and provides opportunity in the stock only from a long term perspective.

At a PE of 55 the margin of safety is limited in IREDA, one not so strong quarter and the stock may start looking quite expensive.

The proposed dilution via the FPO is a cause of concern and if there are multiple equity infusions to fund growth then the long term share holder may not benfit from the opportunity in IREDA. We have seen the EPS CAGR of 17% for FY20-24 lag the PAT CAGR of 55%.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer