IndusInd Bank: 18-23% loan growth CAGR for FY23-26 at a PE of 14 and price to book of 2

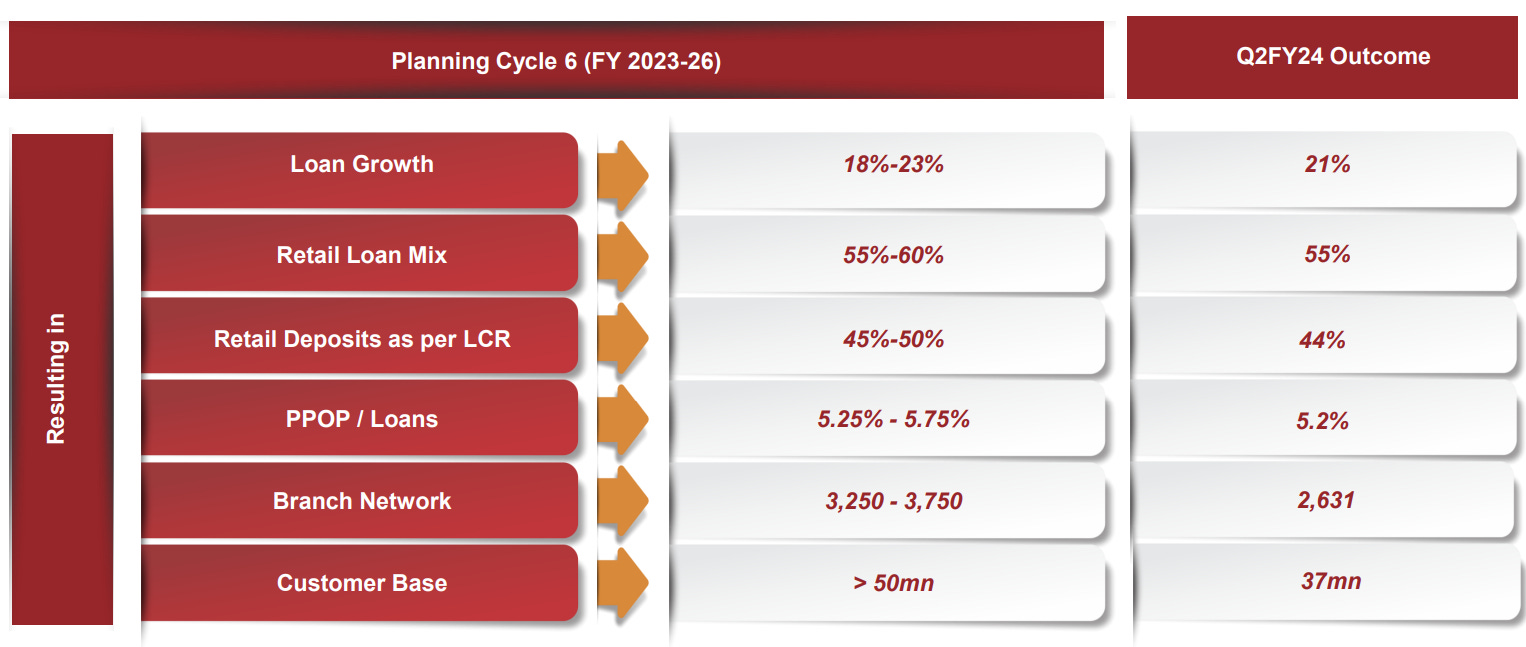

Planning Cycle 6(PC-6) of INDUSINDBK is a roadmap with targets till FY26. Outcome against PC-6 targets as of H1-24 provides confidence in the banks ability to execute & create an upside in the stock

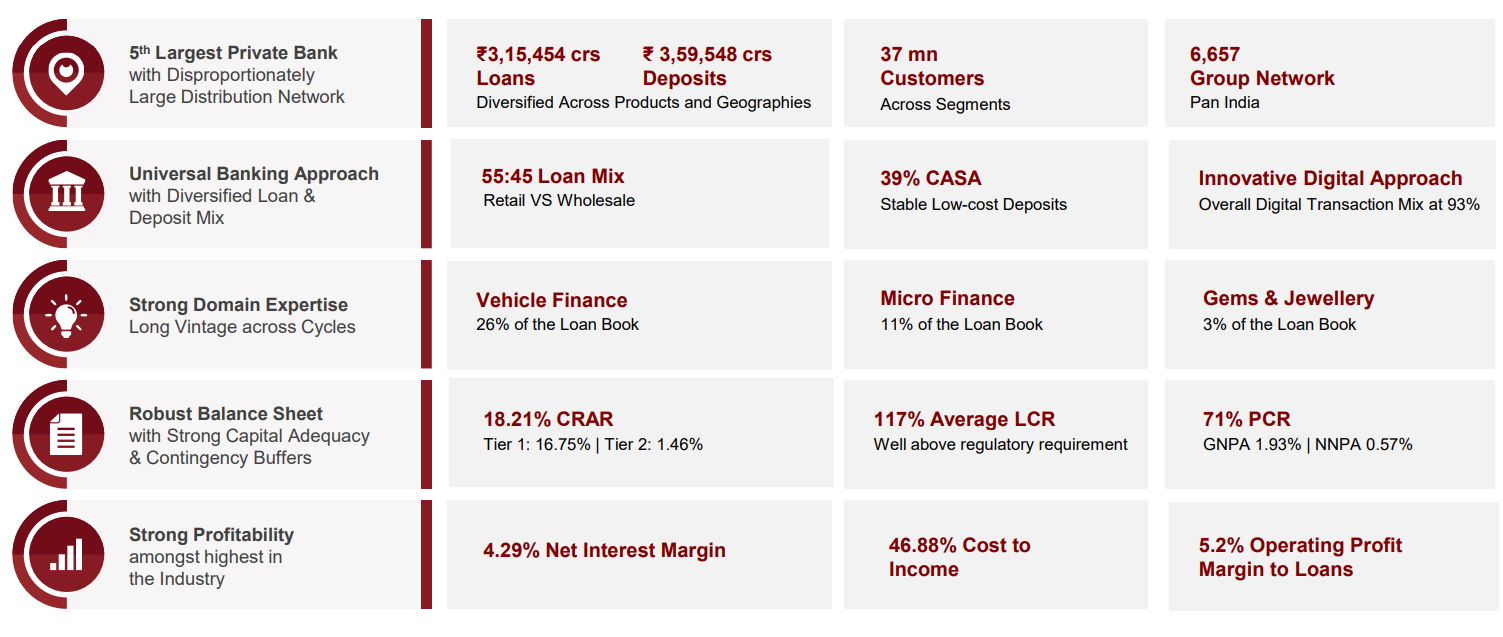

1. 5th Largest Private Bank

indusind.com | NSE: INDUSINDBK

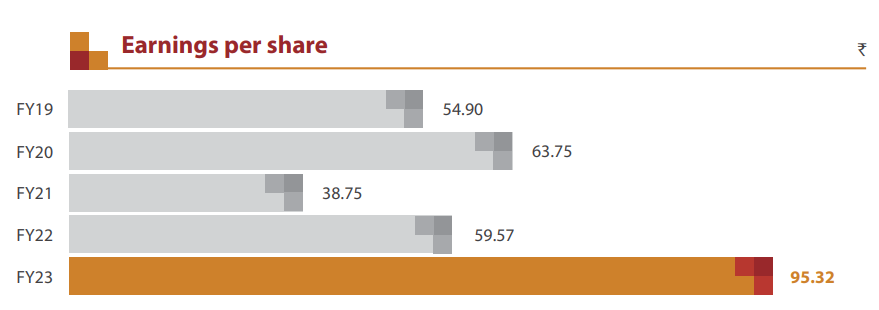

2. FY19-23: 14% CAGR for Earnings per share

Growth delivered in FY23 only

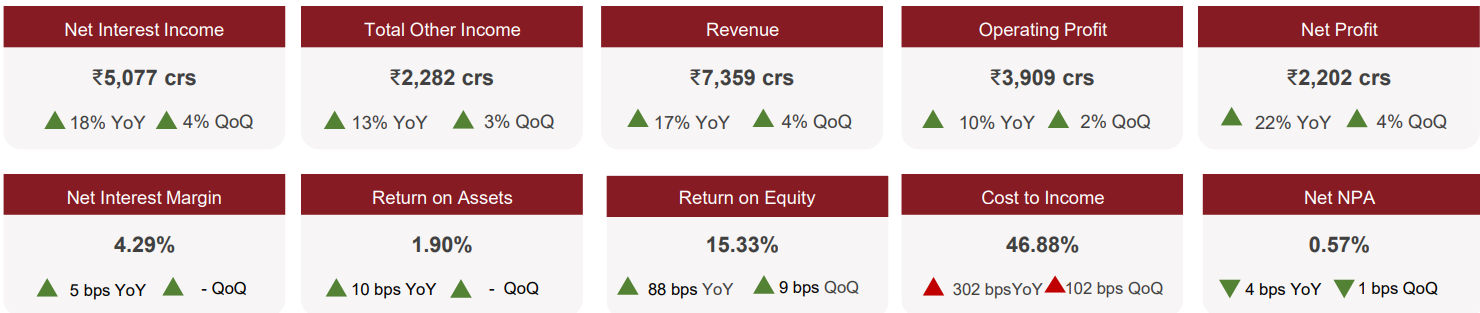

3. Strong Q1-24: PAT up 30% & Revenue up 17% YoY

PAT up 4% & Revenue up 4% QoQ

4. Strong Q2-24: PAT up 22% & Revenue up 17% YoY

PAT up 4% & Revenue up 4% QoQ

5. Overall H1-24 looking strong: PAT up 26% & Revenue up 17% YoY

Total Income of ₹14,436 crores as compared to ₹12,370 crores for the corresponding previous half year

Net Profit was ₹4,326 crores as compared to ₹3,436 crores during corresponding previous half year increased by 26% YoY.

6. Strong & consistent return ratios

INDUSINDBK has grown its book sequentially year on year

7. Outlook: 18-23% loan growth CAGR for FY23-26

22% loan growth in Q1-24 followed by 21% loan growth in Q2-24 indicates that the bank is executing as per its planning cycle. The planning cycle provides a clear and strong roadmap for growth

8. Outlook 18-23% loan growth CAGR for FY23-26 at a PE of less than 14

9. So Wait and Watch

If I hold the stock then one may continue holding on to INDUSINDBK

INDUSINDBK has delivered a very strong FY23 (~100% EPS growth) and followed it up with a strong H1-24 (~26% EPS growth)

Additionally there is an outlook for strong loan growth till FY26 where INDUSINDBK is targeting 18-23% loan growth

We need to keep a very close watch on the EPS growth. We don’t want to be stuck in scenario like FY19-22 where earnings were stuck in a range

11. Or, join the ride

If I am looking to enter the stock then

We are entering INDUSINDBK where a lot of the short term performance starting from FY23 is already in the price. However the loan growth of 18-23% till FY26 is still to be discounted and provides an opportunity in the stock.

From the perspective of PE, loan growth of 18-23% till FY26 at PE of less than 14 is reasonable.

From a price to book perspective, INDUSINDBK has a net-worth of Rs 56,198 cr on a market cap of Rs 112,798.41 cr implying its available at P/B of 2 with growth till FY26 yet to be discounted.

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades