Indo Tech Transformers: PAT up 102% & Revenue up 24% in 9M-25 at a PE of 36

Outlook of 20%+ revenue growth in FY25. with strong margin expansion. Demand outlook & order book providing strong revenue visibility. Growth constrained by capacity. Margins to be sustained

1. Transformer manufacturer

indo-tech.com | NSE: INDOTECH

ITL, incorporated in 1992, manufactures power and distribution transformers and various special application transformers and mobile sub-station transformers. The company’s manufacturing plants are in Chennai and Kancheepuram in Tamil Nadu. ITL is a subsidiary of Shirdi Sai Electricals Limited, and SSEL currently holds a 70.01% stake in ITL.

Products

2. FY20-24: PAT CAGR of 122% & Revenue CAGR of 25%

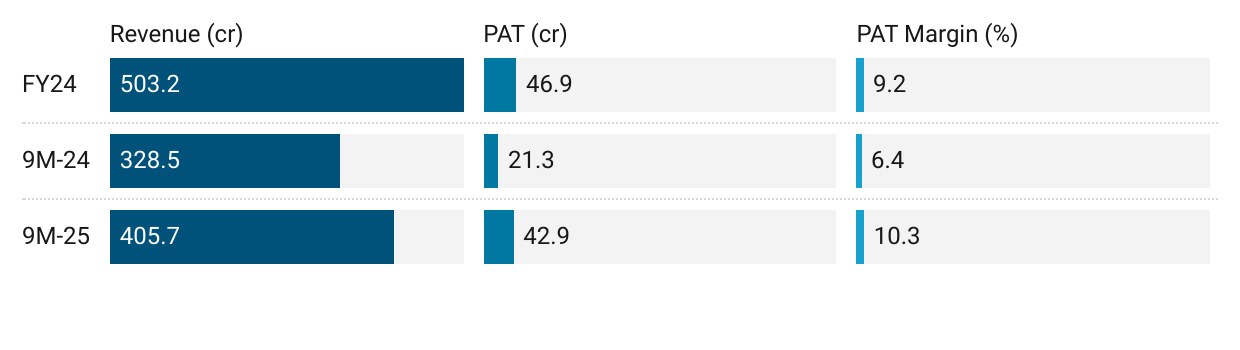

3. Strong FY24: PAT up 82% & Revenue up 36%

4. Strong Q3-25: PAT up 80% & Revenue up 27% YoY

PAT up 9% & Revenue up 21% QoQ

5. 9M-25: PAT up 102% & Revenue up 24% YoY

6. Business metrics: Strong & Improving return ratios

7. Strong outlook: 20% revenue growth in FY25

i. FY25: Strong order book indicating 50% revenue growth

While Rs 700 cr order book is in place, Rs 406 cr revenue in 9M-25 and Rs 177 cr in Q3-25 implies that INDOTECH may just about cross Rs 600 cr revenue in FY25 i.e. 20% kind of growth in FY25.

The orders declared on 31-Dec-24 add up to Rs 149 cr which provides visibility into FY26

Orders declared on 31-Dec-24

ii. FY25: Margins are sustainable

Given that orders have price escalation clauses one can assume the margins to be sustainable.

iii. Capacity to be a growth constraint

With INDOTECH operating at 80-90% capacity, MVA growth i.e. top-line growth would be constrained till FY27.

iv. Industry tailwinds creating strong demand

Management outlook in FY23-24 Annual report is very optimistic based on industry tailwinds

Transformer industry is flushed with orders and the demand outlook is positive vis-a-vis end use in various industries such as railways and renewables. The pent-up demand from industrial expansions backed by a rise in capex is leading to higher consumption of power in India, in turn leading to improved order books for transformer manufacturers.

We remain confident of sustaining the market share and maintaining margins at healthy levels.

8. PAT growth of 102% & Revenue up 24% in 9M-25 at a PE of 36

9. Hold?

If I hold the stock then one may continue holding on to INDOTECH

The outlook for FY25 is strong

Even though there is no management commentary available on INDOTECH, one can hold on as long as one sees the momentum of FY22-24 continues. 9M-25 momentum provides confidence that INDOTECH is on track to deliver a strong FY25. The news orders create positive outlook for FY26

The proposed capacity expansion by INDOTECH management indicates that they confident of the demand outlook into FY28. However one needs to watch out for the impact of capacity constraint on the top-line growth as the full impact of new capacity will come up in FY28.

10. Buy?

If I am looking to enter INDOTECH then

INDOTECH has delivered PAT growth of 102% & with Revenue up by 24% in 9M-25 at a PE of 36 which makes the valuations fully priced in the short term.

Growth outlook for INDOTECH constrained by capacity in FY26 and FY27. Performance in FY26 & FY27 needs to be driven via bottom-line growth. Top-line growth will come in from FY28 which at a PE of 36 makes the valuations expensive. Opportunity in INDOTECH will emerge from a FY28 perspective, which is quite far away.

The lack of any management commentary or public information is the biggest problem one faces in taking a call on INDOTECH. Additionally at a PE of 36, the margin of safety is small in INDOTECH

Previous coverage of INDOTECH

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer