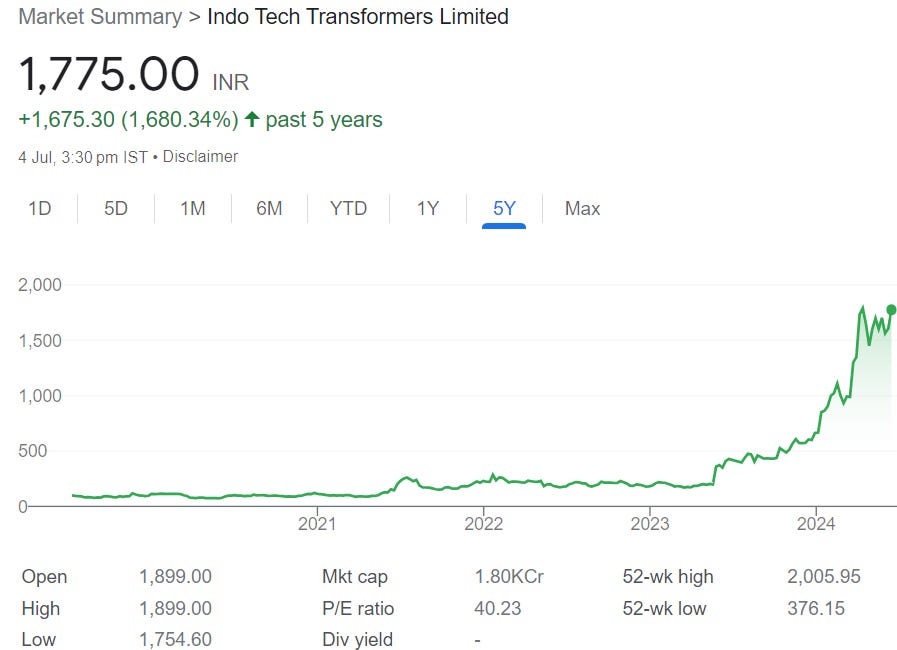

Indo Tech Transformers: PAT up 82% & Revenue up 36% in FY24 at a PE of 40

Doubling of capacity to sustain revenue growth over the longer term. FY25 margins to be sustained given price escalation clauses in majority of the orders.

1. Transformer manufacturer

indo-tech.com | NSE: INDOTECH

ITL, incorporated in 1992, manufactures power and distribution transformers and various special application transformers and mobile sub-station transformers. The company’s manufacturing plants are in Chennai and Kancheepuram in Tamil Nadu. ITL is a subsidiary of Shirdi Sai Electricals Limited, and SSEL currently holds a 70.01% stake in ITL.

Products

2. FY20-24: PAT CAGR of 122% & Revenue CAGR of 25%

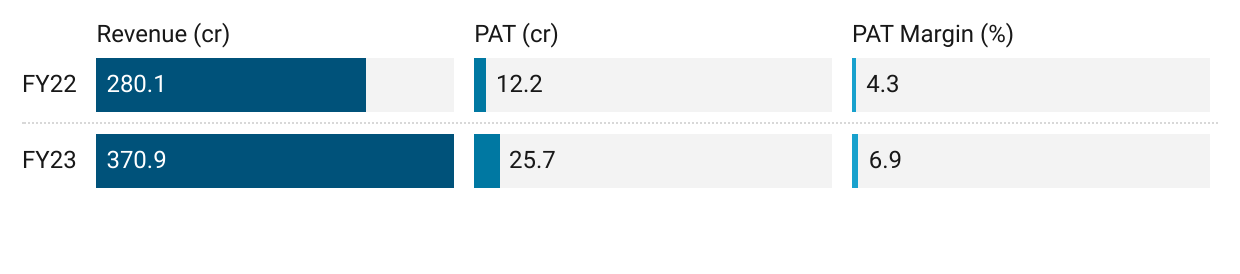

3. Strong FY23: PAT up 111% & Revenue up 32% YoY

4. Strong 9M-24: PAT up 233% & Revenue up 45%

5. Strong Q4-24: PAT up 178% & Revenue up 67% YoY

PAT up 51% & Revenue up 46% QoQ

6. Strong FY24: PAT up 82% & Revenue up 36%

7. Business metrics: Strong & Improving return ratios

8. Strong outlook: Capacity expansion to support growth

i. Capacity to more than double in FY26

ii. FY25: Revenue visibility based on order book

Information on current order book is not available. However, if we assume a similar order book it provides revenue visibility for at least the first three quarters of FY25.

ii. FY25: Margins of FY24 are sustainable

Given that orders have price escalation clauses one can assume the margins to be sustained.

9. PAT growth of 82% & Revenue growth of 36% in FY24 at a PE of 40

10. So Wait and Watch

If I hold the stock then one may continue holding on to INDOTECH

Even though there is no management commentary available on INDOTECH, one can hold on as long as one sees the momentum of FY22-24 continues.

The proposed capacity expansion by INDOTECH management indicates that they confident of the growth momentum to continue into FY26 and beyond.

11. Join the ride

If I am looking to enter INDOTECH then

INDOTECH has delivered PAT growth of 82% & Revenue growth of 36% in FY24 at a PE of 40 which makes the valuations fully priced in the short term.

Outlook for INDOTECH looks positive given the planned doubling of capacity coming online in FY26. Opportunity in INDOTECH will emerge if the momentum of FY22-24 is continued in to FY26 and FY27.

The lack of any management commentary or public information is the biggest problem one faces in taking a call on INDOTECH.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

With Lack of Management Commentary, Concalls etc. it's difficult to judge when to enter, though sector is booming.