India Pesticides Ltd - Hit by a speed breaker

An efficiently run company with a growth history of 25%+ slowing down

Company Overview

Set up in 1984, India Pesticides Limited (IPL) is a chemical manufacturer headquartered in Lucknow, UP. IPL is engaged in the manufacturing of various types of pesticides (technical & formulations) and pharmaceutical intermediates.

IPL is the sole Indian manufacturer and among top five manufacturers globally for several technicals both in fungicides and herbicides.

Share Details

NSE:IPL ( indiapesticideslimited.com)

Quality: Returns on capital employed in cash

Return ratios are quite good and have been consistent with the exception of FY23. IPL is expecting the return ratios to go back to old levels once the next capex and product launches stabilizes which is expected by FY25. One can expect FY24 return ratios to be weak like FY23

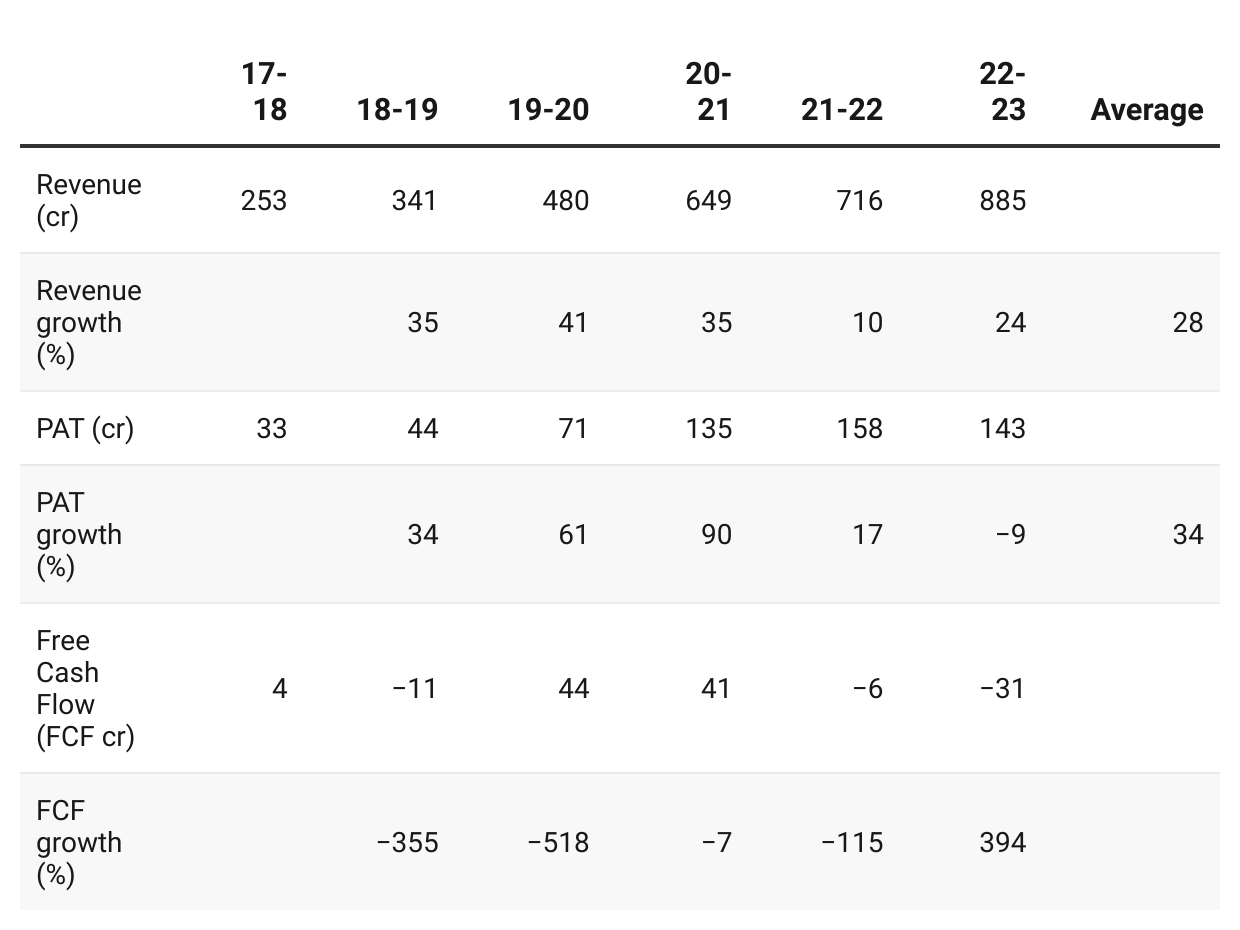

Growth

IPL has grown its top-line and bottom-line quite strongly over the last 6 years. But growth completely slowed down in FY23.

During FY23, we have launched 14 products, which include 10 formulations, 3 technicals and 1 very important intermediate.

New product contribution was around INR 120 crores in this FY23, and we are expecting turnover of INR 175 crores in FY24. It will go up to more than INR 200 crores in FY25.

New product contributed Rs 120 cr implies old products contributed Rs 765 cr in FY23. This implies that old products grew from Rs 716 in FY22 to Rs 765 cr in FY23. The old business growth was around 7% in FY23 down from the 10% growth in FY22.

It puts a big question mark on the growth outlook for IPL going forward.

Growth Momentum

The revenue growth momentum was salvaged by new products in FY24.

Outlook

The weak performance of FY23 would continue in the short term till H1-24

Major headwinds still remain because of the continual downward trend of the technical offering from China, which we feel should stabilize in another 1 or 2 quarters.

Product portfolio and capacity expansion will be driving factors for growth

On the back of product portfolio and capacity expansion the top-line guidance of achieving Rs 1,200 cr by FY from the current Rs 885 cr in FY23 implies a 16% growth CAGR

The margin guidance is that the margins of FY23 will be maintained till FY25.

At least we will be able to maintain the present margins. That much we can tell you.

So What????

If I currently hold the stock, there is a limited chance that I am in the money with IPL given that its trading quite close to its life time low around Rs 197. So I have to look at alternate options.

If I don't currently own the stock, I may not want to enter it. It is an efficiently run company with solid return ratios. However, it’s expensive at a PE of 18, promising growth of 16%. Other than the routine additions to product portfolio and capacity there is nothing exciting in the future story.

IPL is an efficiently run company one should put this company under watch and enter at the right time once the growth momentum picks up.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades