IFGL Refractories: 25%+ growth in FY24, 19-26% growth outlook till FY27, at a 18 PE

Strong performance expected in FY24 after a weak FY23. IFGL expected to deliver on plans to reach Rs 2000 cr in FY25 a year ahead of FY26 target. Working to 2X on FY23 base again by FY27-28

1. Refractory solutions for iron & steel manufacturing

ifglgroup.com | NSE : IFGLEXPOR

IFGL Refractories Ltd offers a wide range of specialised refractory products & operating systems. Expertise in the Iron Making, Steelmaking and Continuous Casting areas with particular emphasis in Slide Gate Systems, Purging Systems, Ladle Lining & Ladle Refractories, Tundish Furnitures & Tundish Refractories, and others.

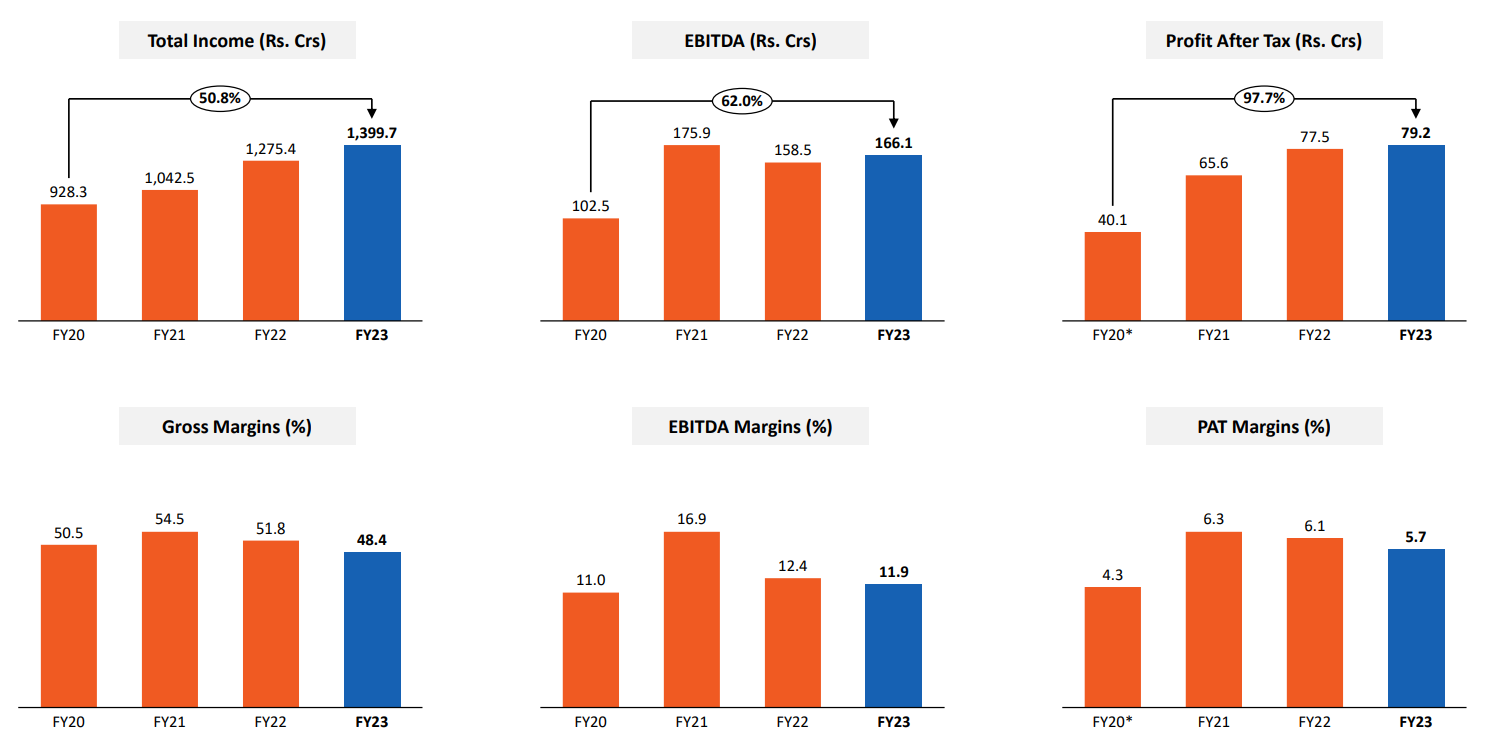

2. FY20-23: PAT CAGR of 26% & Revenue CAGR of 15%

3. A weak FY23: PAT up 2% and Revenue up 10% YoY

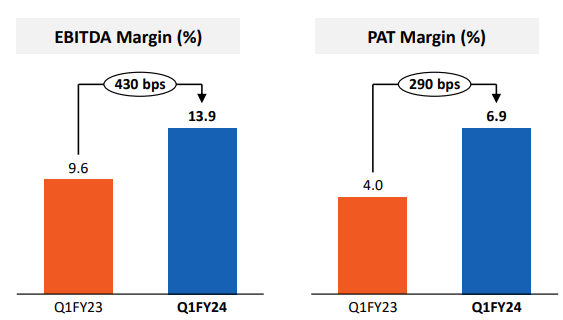

4. Q1-24 stronger than FY23: PAT up 104% and Revenue up 19% YoY

Q1-24 improvement in margin YoY. Q1-24 margin higher than FY23 margin

5. Business metrics are average not exceptional

We are a net cash company from FY19 with our cash & equivalents improving from 134.2 Crs in FY19 to 194.3 Crs in FY23 while our net debt position as on 31st Mar-23 stood at 45.9 Crs

6. Outlook: 25% revenue growth and 12%+ EBITDA in FY24

i. 25% revenue growth and 12%+ EBITDA in FY24

We are talking of a consolidated turnover of 1,750 plus.

Consolidated, my guidance is about 12% plus EBITDA margins.

ii. To 2X revenue in FY27 or FY28, 19-26% CAGR growth outlook

IFGL Refractories Aims To Double Revenue In 4-5 Years | CNBC TV18

iii. Will 2X revenue on FY21 base in FY25 ahead of plan of FY26

Target of Rs 2085 cr revenue by FY26, double of FY21 revenue. Guidance to reach Rs 1750 cr by FY24. One could expect the Rs 2000+ cr turnover target to be achieved in FY25 itself.

I will maintain the same, that we are talking of doubling our turnover in five years' time from 2021 to 2026.

iv. Growth in FY25 to supported by capex in existing facilities

In both Odisha and Vizag, we have spent approximately 50% of the planned CAPEX so far, and in Kandla we have completed almost, we have spent about 90% of that. The remaining CAPEX is expected to be completed by March 24.

Research Center at Kalunga is almost ready and likely to be operationalized in Q3FY24.

With these enhanced capacities and new production capabilities, we expect to improve the scale of business which will lead to scaled benefits and operating leverage playing out of the long-term offer for the benefits for the company.

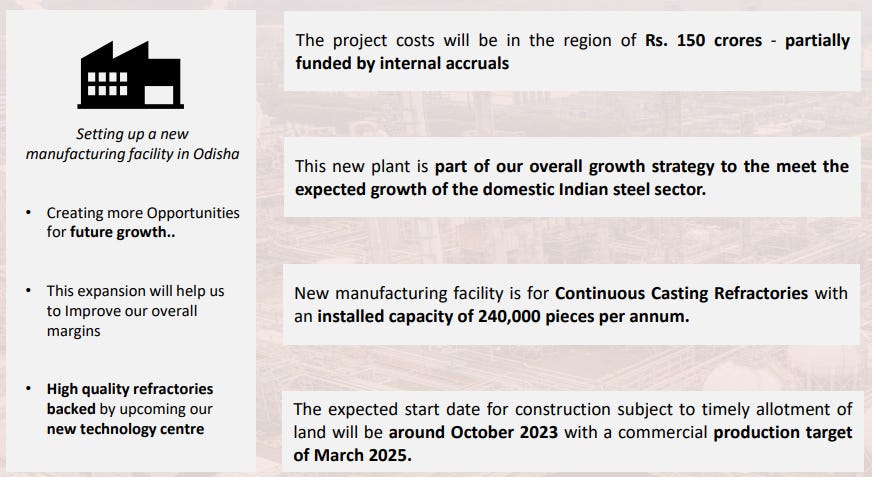

v. Growth in FY26 to supported by new manufacturing facility

7. 25% growth in FY24 and 19-26% growth till FY27 at a PE of 18

8. So Wait and Watch

If I hold the stock then one may continue holding on to IFGL even though FY23 was weak. Q1-24 results provide confidence to stay the course with IFGL.

25% revenue growth guidance for FY24 and a capex driven roadmap for growth delivering 19-26% growth till FY27 provide opportunities to stay invested and keep watching its execution.

IFGL seems close to delivering on its target to double the company on FY21 base a year ahead of the target provides confidence that it will be able to deliver on its capex led growth roadmap by FY27

9. Or, join the ride

If I am looking to enter the stock then

25%+ revenue growth in FY24 and 19-26% growth till FY27 at a PE of 18 looks reasonable.

All growth is based on organic growth projections and does not factor in inorganic growth. IFGL is open to inorganic growth in future after completing the acquisition of Sheffield Refractories Limited in Feb-23

IFGL Refractories Aims To Double Revenue In 4-5 Years | CNBC TV18

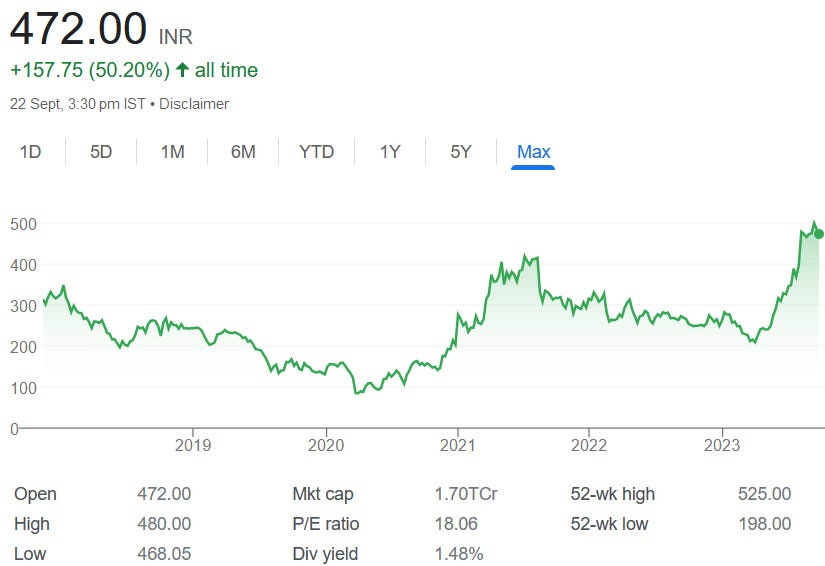

On a price to book of 1.79 based on FY23 book, the stock is reasonable valued.

The management feels that IFGL is undervalued

We have also grown in the share prices from about 200-plus levels to about 300-plus levels in the last, say, I think, what, a month's time. So it is not that we have not grown. We are undervalued. We feel that the market should give us more valuations.

As on 2-Jun-23. Closing Price =Rs 316.35

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades