Hotels Q3-25: Boom, High Margins, Low Supply, & Asset-Light Growth

High demand, strong pricing & record profits. Chains are expanding fast using asset-light models & premium brands. Digital upgrades, loyalty programs, and weddings drive non-room revenue

1. Emerging Trends & Challenges

1.1 Luxury & Premium Hotels Continue to Lead

Premium brands like Taj, Oberoi, JW Marriott, and Lemon Tree Premier are seeing stronger ARR and RevPAR growth than mid-market hotels.

Chalet Hotels reported ADRs reaching ₹13,000 and 17% RevPAR growth.

1.2 Capital-Light Expansion Models

All major hotel chains are pursuing asset-light growth through management/franchise contracts.

Lemon Tree: 13 new management/franchise contracts signed this quarter alone.

IHCL (Taj) and EIH (Oberoi) are adding dozens of new properties, focusing heavily on management contracts.

1.3 RevPAR-Driven Strategy Over Occupancy Gains

Occupancy rates are plateauing around 75–80% for most players, with focus shifting to ARR-driven RevPAR growth for profitability.

1.4 Tier 2/3 Cities & Mid-Market Surge Coming

While metros still lead, Lemon Tree and others forecast mid-scale demand boom as more households move into aspirational consumption brackets.

Currently, Metro cities outperform leisure hubs like Goa and Bhubaneswar in growth. Hotels in these areas saw only ~2% YoY growth.

1.5 Boom in Weddings, MICE, & F&B Revenue

F&B and events (especially weddings) are major growth drivers. Taj and Chalet are investing in high-energy venues and banquet facilities.

1.6 Loyalty & Direct Channels Driving Bookings

Taj's Tata Neu loyalty platform is now a major contributor to revenue. Ginger brand sees 40% revenue from loyalty members.

1.7 Foreign Tourist Arrivals (FTAs) Recovery Still Incomplete

FTAs remain below pre-COVID levels. Taj and Chalet expect recovery to accelerate once airport infrastructure (e.g. Navi Mumbai airport) improves.

1.8 Rising Competition & Supply in Key Markets

High-end projects like Fairmont in Mumbai and other new launches are increasing competition in metro markets.

1.9 Capex Pressure from Renovation Cycles

Many hotel chains are midway through renovation plans (e.g., Lemon Tree renovating 6,000 rooms by FY27), impacting short-term margins.

1.10 Talent Shortage & Operational Costs

While talent cost pressure is not yet severe, maintaining service quality in expansion and renovation phases is a key concern.

2. Demand Outlook: 2025 and Beyond

2.1 Short-to-Medium Term (FY25–FY26): Very Strong

Corporate & Business Travel

Surging in metro cities like Mumbai, Delhi, Hyderabad, and Bangalore.

Driven by increased domestic air travel (+12% YoY), conferences, and resumed international delegations.

MICE (Meetings, Incentives, Conferences, Exhibitions) and G20 spillover effects still visible.

“City hotels are running at near full capacity with strong pricing power” — Chalet Hotels

“Occupancy remains above 78%, and ARR continues to rise” — IHCL

Leisure & Domestic Tourism

Consistent demand in tier-1 leisure destinations (Udaipur, Jaipur, Goa), though growth is tapering vs. metros.

Weekend getaways, wellness travel, and destination weddings are key contributors.

“Weddings, F&B and leisure travel are key revenue levers, with extended wedding seasons in Q4” — IHCL

Mid-Scale & Tier 2/3 Growth

Rising middle-class spending and improved road/air connectivity fueling demand in emerging cities (e.g., Nagpur, Raipur, Coimbatore).

Lemon Tree and Ginger brands expanding rapidly in these regions.

“Demand in tier 2 and 3 cities is growing faster than metros in terms of % growth” — Lemon Tree

Foreign Tourist Arrivals (FTAs)

Still below pre-COVID levels, especially in leisure segments.

However, expected to pick up in FY26, aided by:

Weak rupee (making India cheaper)

Expansion of airports (e.g. Navi Mumbai, Jewar)

Return of global events and exhibitions

“International travel to our hotels in Bali and New York has picked up; India still undervalued” — EIH/Oberoi

2.2 Long-Term View (to 2030): Bullish

GDP growth (~6–7%), urbanization, rising disposable income, and infrastructural development will drive long-term demand.

Hotel chains are planning aggressively — over 300 hotels are in active pipelines across chains like IHCL, Lemon Tree, and Chalet.

“Hospitality is writing a new narrative for India at 2047” — IHCL CEO Puneet Chhatwal

3. Hotel Room Supply Outlook

3.1 Overall Direction: Moderate Supply Growth

Supply growth is expected to lag behind demand, creating favorable pricing power for hotels through FY26–27.

High land and construction costs are slowing new builds.

Most chains are expanding via asset-light models (management contracts), which take 18–36 months to go live.

Occupancy and ARR will stay elevated through FY26 due to demand outpacing new supply.

Tier 2/3 cities will see a bulk of new capacity—mainly by Lemon Tree and Ginger.

Ultra-premium and metro inventory will grow slower due to high development costs and regulatory approvals.

Long-term supply will gradually normalize post-FY27, but pricing power will likely remain in favor of hotels for the next 2–3 years.

3.2 Key Data Points from Hotel Chains

Indian Hotels (Taj, Ginger, etc.)

Total pipeline: 123 hotels

Signed 55 hotels & opened 20 in April–Dec 2024

Target: 25 openings in FY25, 30+ in FY26

80% of pipeline is capital-light

“More than 50% of our entire hotel base is in the pipeline” — IHCL

Lemon Tree Hotels

Pipeline: ~4,000 keys over next 3 years

Signed 13 new properties in Q3 alone

Renovating 6,000 existing rooms by FY27

Focused heavily on tier 2/3 cities

“Key growth will come from franchise & management models, especially in underserved cities” — Lemon Tree

EIH (Oberoi Group)

Expansion pipeline: 19 new properties

13 Oberoi/Trident hotels

3 luxury boats

Split: 10 domestic, 9 international

Focus on ultra-premium offerings (slow build cycle)

“We are adding across formats—owned, managed, JV—but timelines extend into FY27+” — EIH

Chalet Hotels

Plans to double room capacity from current ~3,000 keys

Actively converting land banks (Bangalore, Navi Mumbai)

Focused on luxury and business hotels in metro markets

“Expect new capacity to come online by FY26–27, especially near metro airports” — Chalet

Ventive Hospitality: Small but fast-growing player expanding via resorts and experiential stays with an asset-light model in early stages

4. Pricing & Revenue Outlook

4.1 Pricing Outlook: Sustained Upside in Average Room Rates (ARR)

High demand + limited supply = continued pricing power.

All major players indicated confidence in raising rates without losing occupancy.

“There’s considerable upside in rate—we are still underpriced for the quality we offer.” Oberoi (EIH)

“We are operating at 78–80% occupancy. Our focus is now ARR-led RevPAR growth.” IHCL (Taj)

Achieved ADR of ₹13,000+, among the highest in India. Chalet Hotels

Targeting mid-single to double-digit ARR growth across segments, with premium brands driving pricing upside. Lemon Tree

4.2 Revenue Outlook: Double-Digit Revenue Growth Expected to Continue

Industry-wide revenue is expected to grow 10–15% annually through FY26.

Growth drivers:

Higher ARRs (especially in metros & Tier 1 leisure)

Full recovery of MICE, weddings, and F&B revenue

Pipeline openings starting to contribute from FY25 onward

Digital & loyalty-led direct booking channels boosting margins

“We expect to deliver strong growth with sustained margins. Q4 to be in line with Q3.” Projecting 15%+ YoY revenue growth IHCL

Lemon Tree : Forecasts ~25% revenue CAGR over 2–3 years, driven by scale and new room additions

Chalet Hotels: Strong revenue visibility from:

High-end metro properties

New hotels near airports (Bangalore, Navi Mumbai)

Commercial assets leasing alongside hotels

4.3 Additional Revenue Levers

4.4 Risks to Monitor:

Macro slowdown (if GDP dips below 6%)

Delay in FTA (foreign tourist arrival) recovery

New supply flooding metros post-2027

5. Profitability Outlook

5.1 Drivers of Profitability Growth: High ARR + Stable Occupancy = Strong RevPAR → Flow-through to EBITDA

Hotels are operating at 70–80% occupancy, so every ARR increase directly lifts EBITDA.

Most players are okay sacrificing slight occupancy for ARR-led profit growth.

“We are happy to sacrifice occupancy if it improves ARR and flows to the bottom line.” — Oberoi

5.2 Asset-Light Expansion

Management contracts and franchises require minimal capital and offer high-margin fee income.

IHCL’s management fees in Q3 grew 32% YoY.

“80% of our pipeline is asset-light—key to sustaining margins.” — IHCL

5.3 Cost Optimization & Tech Efficiency

Lemon Tree and IHCL have adopted centralized procurement, digital systems, and AI-driven dynamic pricing.

IHCL operating margins improved 240 bps YoY despite expansion.

5.4 Diversified Revenue Streams (Weddings, F&B, Loyalty)

Weddings, MICE, and F&B are now profit centers, not just revenue fillers.

Taj’s Qmin and Chalet’s events business are high-margin.

5.5 Challenges to Profitability

High Development Costs

Land + construction costs make it hard for owned projects to generate strong ROCE.

Oberoi is focusing on mixed-use projects in cities to justify capex.

Renovation Disruptions

Many chains are mid-cycle in refurbishments (e.g., Oberoi Grand Kolkata, Lemon Tree’s 6,000 rooms).

Short-term EBITDA may be suppressed at some properties.

Talent & Wage Inflation (Emerging Risk)

While stable for now, increased hiring for new properties and quality service at scale may push HR costs up in FY26–27.

Profitability is peaking — and sustainable.

The combination of strong RevPAR growth, operating leverage, asset-light expansion, and premium positioning is expected to drive high-margin performance through FY26.

6. Investment Opportunity

6.1 The Opportunity

India’s hotel sector is entering a golden phase with:

High demand outpacing supply

Record ARR and RevPAR growth

Margin expansion via asset-light models

Surging non-room revenue (F&B, weddings, MICE)

Rising middle-class travel & infrastructure push

Well-managed hotel chains (like IHCL, Lemon Tree, Chalet, EIH) are primed to deliver double-digit revenue and PAT growth over the next 2–3 years.

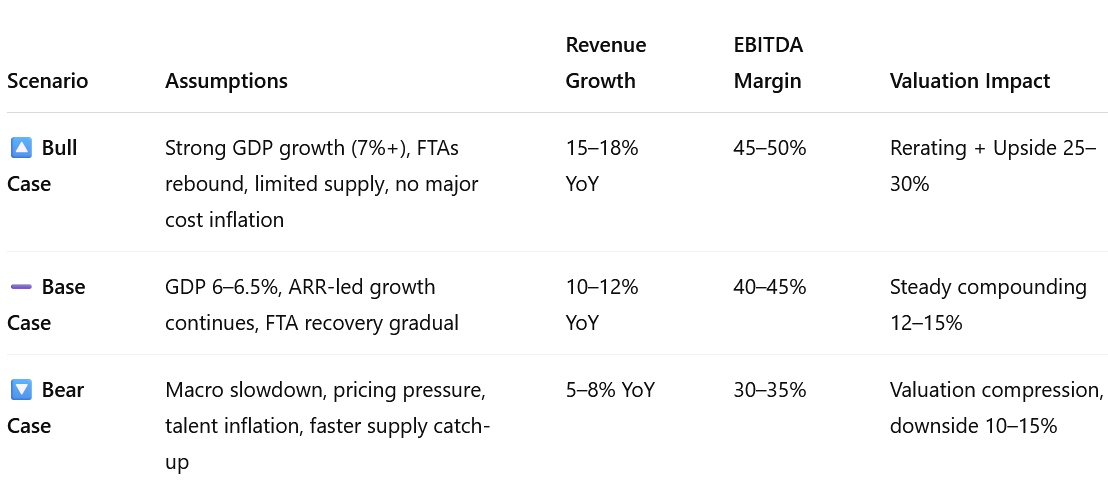

6.2 Risk-Reward Analysis

6.3 Key Upside Catalysts:

Foreign tourist arrivals return to pre-COVID levels

Tier 2/3 market expansion accelerates

Airport hotels + infra projects (e.g., Navi Mumbai) drive localized booms

Premiumization supports rate hikes without demand drop-off

Brand-led consolidation takes market share from unorganized players

6.4 Key Risks:

Macro shocks (geopolitical events, inflation)

New supply flooding metros post-FY27

Wage inflation and staffing gaps

FX volatility if operating abroad

Disclaimer

Content Accuracy and Reliability: This summary of the earnings call is generated using an artificial intelligence large language model (LLM). While every effort has been made to ensure the accuracy and completeness of the information, the summary may not fully capture all nuances or details of the original earnings call. The content provided is for informational purposes only and should not be construed as financial advice or a recommendation to buy or sell any securities. Verification: Readers are encouraged to refer to the official earnings call transcript, company filings, and other authoritative sources for comprehensive and accurate information. The creators of this summary do not guarantee the accuracy, completeness, or timeliness of the information and accept no responsibility for any errors or omissions. No Liability: The use of this summary is at your own risk. The creators and distributors of this content disclaim any liability for any loss or damage arising from the use of or reliance on this summary. Consult Professional Advice: For investment decisions or financial advice, please consult a qualified financial advisor or other professional